Africa Oil: Like I never left

It's worth more(paywall removed)

Africa Oil has not been a strong performer this year but based on multiple catalysts all happening during the first half of 2025 and the stock price being depressed by the weak oil price and tax loss selling currently. I see a high chance of a rerating of the stock from the current price during the first half of 2025.

Mongolian AD: THE LINK

Use my Affiliate link to sign up for Seeking Alpha premium. Now with a black Friday sale until December 5th.

7-day free trial+90$ discount!

Africa Oil: The cheapest oil stock I know

Africa Oil has been cheap for a while, but it has also been confusing, and directionless, but in recent months there has been a shift within the company, because of management changes. A new direction that I like. Maybe some of you have looked into this company in the past and you have seen this monstrosity.

Last January I wrote this. “The Cheapest Oil Stock I Know” There have been some developments since then and it’s time to provide my updated thoughts.

Maybe some of you who don’t follow me on Twitter didn’t know that I sold out of Africa Oil in September and then recently at a bit higher price bought back in.

So what happened there why did I abandon Africa Oil and then unabandon it?

The primary reason was that I wanted to buy more Valeura Energy. Both stocks were falling because the oil price was going down and I thought why not just get more Valeura? Because Valeura is cheaper than Africa Oil, it has better management, better catalysts, and better everything. And it was a good move as Valeura is up 25% from that buy.

The second reason for my decision to sell Africa Oil was that Africa Oil announced a deal that would double its production. In my opinion, this deal is good for shareholders, but originally it was supposed to close in Q3 2025 and they said they won’t be doing buybacks until this happens. This was my take and the details of the deal.

source: AlmostMongolian, X

I think it’s a good deal, but having to wait until Q3, or maybe before, and the way these situations tend to go when there are regulatory things that need to get done there would be a high chance of further delays. It might not actually close until Q4. Then they said in the Q2 earnings call that they won’t be buying back shares until the deal closes.

Source: SA Premium, Africa Q2 conference call transcript

The buybacks were supporting the Africa Oil stock for the whole year and we saw a drop in the share price after they stopped. However, that was also because of the falling oil price.

So I’m looking at this situation thinking:

“There won’t be a buyback or increased dividend likely until Q3 maybe Q4 next year. The stock will also suffer from tax loss selling before the end of the year. I think this will be dead money for a bit. I’m going to buy something else like Valeura that is also very cheap but has short-term catalysts.”

I was planning to re-enter Africa Oil closer to when the deal closes if it’s still very cheap.

Why did I return to Africa Oil?

First, they announced they now expect the deal to be closed at the end of the first quarter of 2025 and then they re-initiated the buyback.

Source: https://ceo.ca/@newswire/nigerian-regulator-clears-prime-consolidation

Then in the Q3 earnings call, they said they restarted the buyback.

Source: SA premium, Africa Oil Q3 earnings call transcript

This is counter to what they said in the Q2 call. They said they won’t buy back shares until the consolidation is done, but here they say they waited for the Impact farm down to complete until buying back shares, but whatever I like buybacks.

Source: https://ceo.ca/@newswire/africa-oil-announces-results-of-share-buyback-program-7baef

So basically both of the reasons why I sold got rectified. The deal will close sooner and the buybacks re-started. This means I have to be long again. This is why I follow my ex-investments and this situation inspired my article “Follow your ex-investments(link)” I did not mention Africa Oil in that article, because I knew I would make a stand-alone article about Africa Oil.

The stock is already recovering a bit, but I see an easy path back to the 2.5-3.5 CAD price level.

Source: Google

CURRENT SET-UP

Market cap=624m USD

“When we complete the transaction with BTG amalgamation, we are going to issue a fixed number of shares, which have been pretty fine and it's roughly 240 million shares.”

Market cap after the amalgamation=443+240=683m shares at 1,35$ USD is 963m market cap

EV After the consolidation= Prime net debt is 329,4m and Africa oil net cash is 136.1m so EV pro-forma is 922+329,4-136.1=1 156,3m USD

Should I use amalgamation or consolidation? I hate both so much I can’t decide. Send me a YouTube comment about what word I should use.

Source: https://africaoilcorp.com/wp-content/uploads/2024/08/Q224-Presentation__August-2024_FINAL.pdf

It’s already pretty cheap based on this Pro-Forma outlook that uses a 2-year forward curve + $70LT Brent with 2% annual inflation. It’s a pretty conservative price outlook. The current Brent price is 71$ after a big drop recently. So using those price assumptions Africa Oil will be making these FCF amounts. And I’m just eyeballing these numbers from this chart so they are roughly accurate and in USD.

2025=275m FCF

2026=200m FCF

2027=170m FCF

2028=330m FCF Preowei Project production lift.

Post 2029 Venus is expected to start producing, but there is a lot of uncertainty around its size and timing so they don’t make clear predictions anymore.

Their producing fields are declining, but they will be looking to offset this with new developments in Nigeria and Orange Basin.

These fields even though declining are low-cost and will be highly profitable for the foreseeable future.

Using next year’s FCF assuming around 70$ oil price(Brent) Market cap/FCF would be 3,5 and EV/FCF would be 4,2. This is a cheap valuation, but nothing crazy in this sector. It does get much cheaper when you include their exploration assets.

What I like about this deal is that it commits to a 100m base dividend which would be a 10,3% dividend yield at the current valuation.

In addition: “an annual commitment to distribute at least 50 percent. of excess free cash flow after Base Dividend distribution in the form of supplemental dividends and/or share repurchases”

If we add this we would have 275m of FCF 100m base dividend and at least 50% of what is left after it=87,5m would also go towards dividends or buybacks meaning a minimum of 187,5m of shareholder returns compared to 922m market cap meaning a 19,4% shareholders yield.

Shareholders’ yield is like dividend yield but also includes stock buybacks and debt repayments.

These commitments to a base dividend and at least 50% of FCF after the base dividend to shareholder returns are really good. These policies can drive a rerating in the valuation because people can expect reliable income from the stock. I’m not very interested in the dividend itself. I’m more interested in the rerating it could deliver because the stock will be more attractive to dividend investors and institutional investors.

Africa Oil did not have a predictable shareholder returns policy before. They would have a small dividend and do buybacks here and there, but it was not consistent or predictable. This hurt the stock because the stock seemed directionless in the past. The valuation was cheap, but it kind of did everything. It was an exploration and M&A-focused company with random shareholder distributions and many minority shareholdings in other companies.

Now they are taking a clear direction. They are a high dividend payer and consolidating their portfolio to their core assets.

BTG who is the other party in this consolidation will own 35% of the company and will also have board seats and are in a two-year lock-up which is good as we won’t be seeing increased selling pressure from this dilution for a while. They are clearly focused on being paid and were likely the driving force behind the shareholder return commitments.

The shareholder return commitments are also a shield from bad moves by the management because they won’t even have a lot of money to work with to make any new major acquisitions.

This is good because I think they have all they need in their portfolio already for an easy 50-150% rerating of the stock. There does not need to be any additional M&A.

What is going on with their other assets?

What is there in addition to the 10,3% dividend yield and 19,4% shareholders yield?

3B/4B drilling, Large potential expansion of Venus, Eg-18 exploration results

Developments and catalysts with other assets

Recently the Venus fam-down was completed. This deal provides Impact 99m USD and 9,5% of carried interest in the Venus discovery. Africa Oil’s current position in Impact is 32,4% (3,08% carried interest in Venus for Africa oil), but they have an agreement in place to increase their position in Impact to 39.5%(3,75% carried)

Source: https://ceo.ca/@newswire/africa-oil-announces-agreement-to-acquire-a-material

What is interesting about this deal is that we can see how the participants are valuing Impact.

This agreement values impact at:

80 160 198*0,57 GBP=45 691 312,86/0,071=634 539 744,5 GBP enhance rate in Aug 27th was 1,33 to USD so 634 539 744,5*1,33=843 937 860 USD

So current Africa Oil’s position at 32,4% is valued at 273 435 866 USD and 39,5% would be 333 355 454 USD.

They also have a deal in place with Eco Atlantic that increases their position in block 3B/4B to 18%. The deal favors Eco Atlantic but is not very material for Africa Oil. More about that in my Eco Atlantic article and in general I would refer you to my Eco Atlantic article LINK for information about 3B/4B as it is my most in-depth and recent deep dive on it. Although it’s in the paid part of the article. I also talk about it in my original Africa oil write-up LINK which is a 100% free article.

I don’t want to regurgitate everything about 3B/4B here, but Africa Oil will have 18% and likely 2 exploration wells fully carried and drilling expected in the first half of 2025 and it’s a very promising block.

In my Eco article, I made a valuation of 3B/4B looking at how different deals valued the block for ECO

Source: My Eco article

If we just adjust that to Africa Oil’s position of 18% post-Eco deal is worth according to these valuations

28,8m USD

77,04m USD

207m USD

I would use the number 2 valuation because It’s the most recent valuation with multiple parties involved like Total and Qatar Energy.

If we take 3B/4B and Venus out of the market cap we would be paying 552,6m USD for the cash-flowing portion of the business if we include net debt then it would be 745,9m USD.

I’m done with the valuations now. Their Equatorial Guinea assets don’t have a valuation I can find.

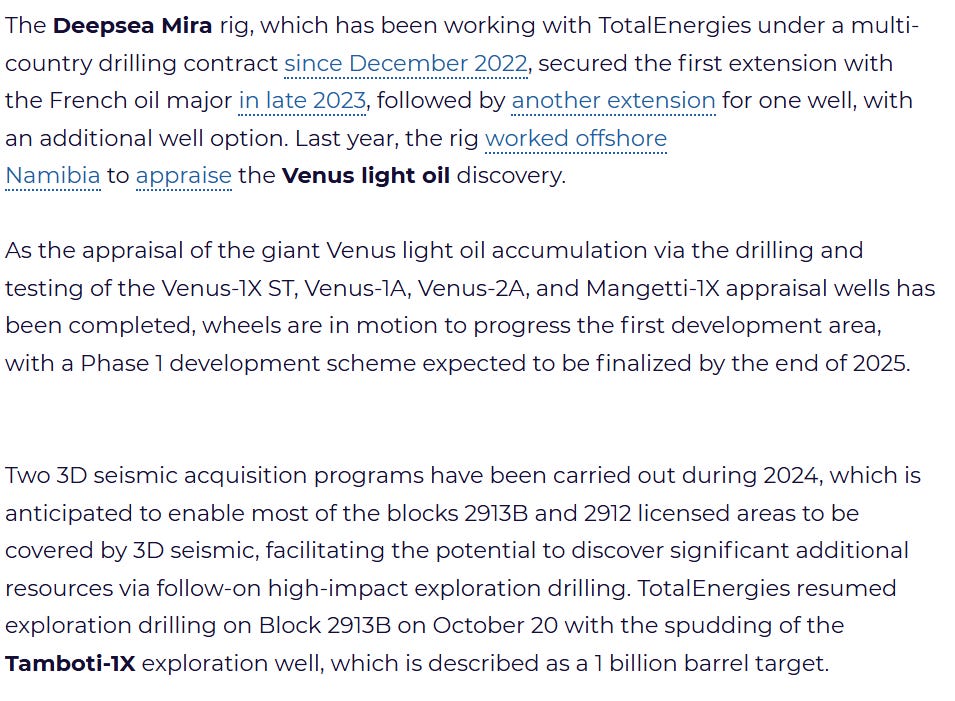

First half of 2025 we have the amalgamation and 3B/4B drilling and we also should have the results for the Tamboti well which is expected to expand Venus by a lot.

“So Tamboti, we anticipate to get the results there. If the well is tested by the end of Q1, 2025, it'll probably be in the objective in December.”

“But we will point you to what Patrick Pouyanne said in that it is an elephant. And he then was asked what an elephant is, and he said over 1 billion barrels. And I would not disagree with that interpretation.”

Quotes from Africa Oil Q3 earning call

Source: https://www.offshore-energy.biz/totalenergies-embarks-on-high-impact-exploration-drilling-ops-offshore-namibia/

If this well goes as expected it would be a significant development.

Source:https://totalenergies.com/sites/g/files/nytnzq121/files/documents/totalenergies_2024-strategy-and-outlook-presentation_2024_en_pdf.pdf

Total is looking to expand Venus from the North with Tamboti results coming soon and potentially from the South as well within 2025.

I have seen estimates for Venus of 1,5-5.1 billion barrels, but considering how many of these prospects have not been drilled yet the final number could be much higher.

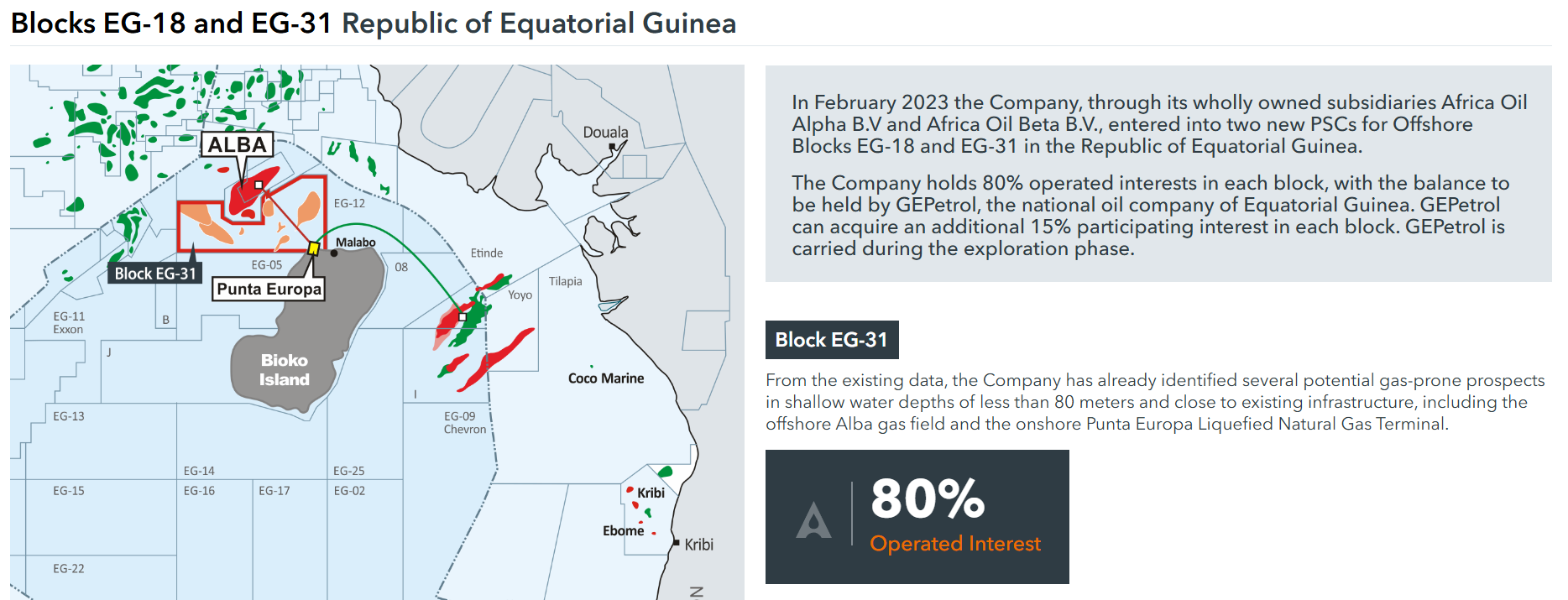

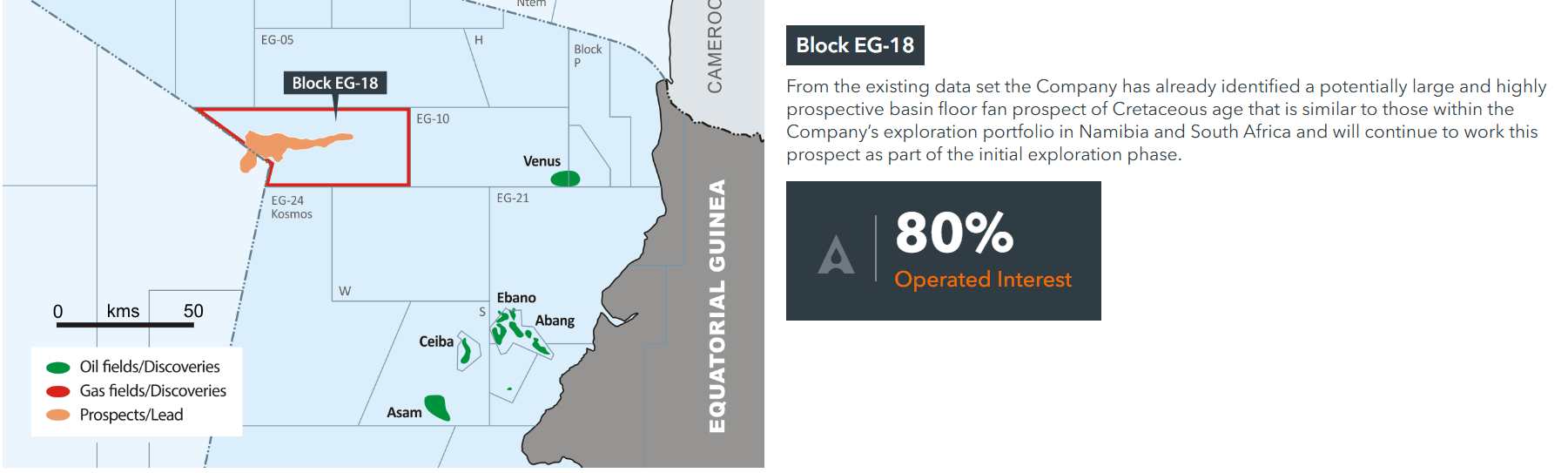

The last asset I will talk about is the Equatorial Guinea assets EG-31 and EG-18. There have been some exploration results in EG-18

EG-31

Source: https://africaoilcorp.com/equatorial-guinea-operations/

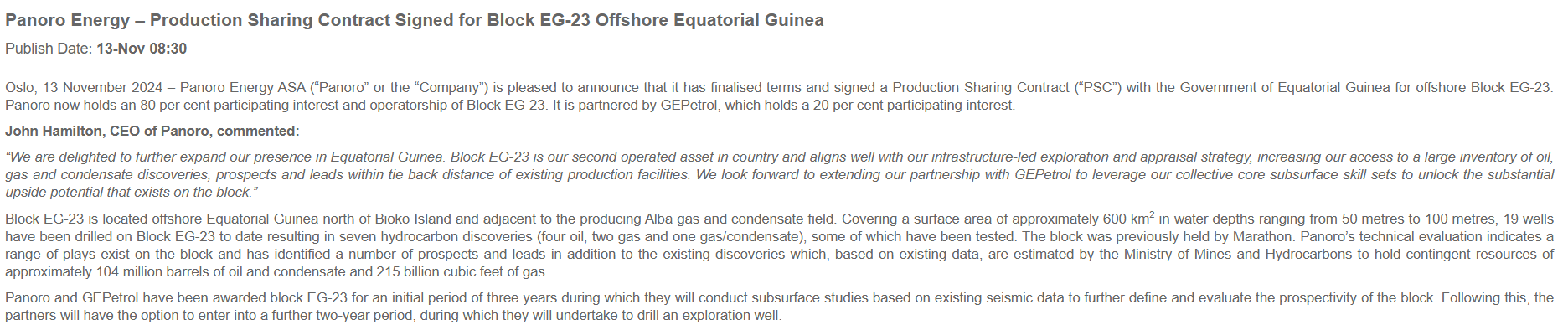

Still a promising asset because it’s right next to a large gas field and an LNG terminal and the block that is above the Alba Gas field and also borders Eg-31 just got awarded to Panoro Energy.

Source: https://www.panoroenergy.com//wp-content/themes/hello-elementor/cision/releasesingledetail.html?releaseIdentifier=8F3168D5DAC41B64

Panoro seems optimistic this some good buzz around the area, but more interesting is the EG-18 exploration results.

Source: https://africaoilcorp.com/equatorial-guinea-operations/

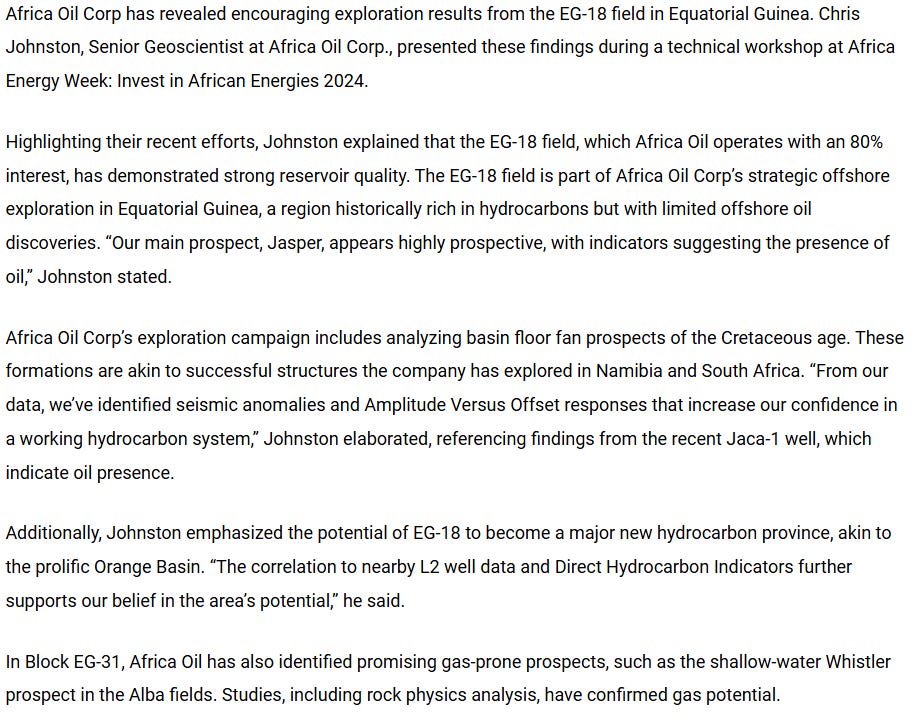

Seems like there is also an oil discovery named Venus in Equatorial Guinea. Why are people naming their oil discoveries Venus?

Africa Oil did this conference which I could not find a video of. At this conference, they had some comments about these assets I had not heard before.

Source: https://aecweek.com/africa-oil-corp-shares-exploration-results-in-equatorial-guineas-eg-18-field-at-aew-2024/

Source: https://aecweek.com/major-oil-gas-farm-in-prospects-unveiled-at-african-farmout-forum/

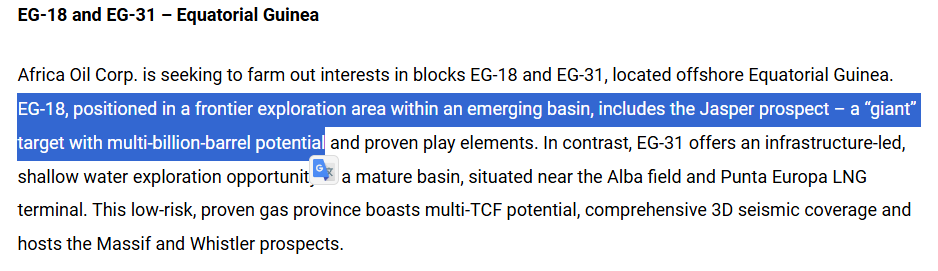

This is quite interesting. Obviously, if they would drill this “Jasper” prospect and it would be a multi-billion barrel find it would be huge for the stock and they didn’t even talk about these assets in the Q3 earnings call but seem quite optimistic about them.

This was presented at “The African Farmout Forum” with 16 other companies. They are pitching these assets for a farm out but it’s kind of odd that they are now going to conferences marketing these blocks when during last year’s Q3 call they said they had so many people trying to get in and had to extend the deadline to get more bids in although this was referring to EG-31.

“The exact timeline on EG 31, we weren't going to ask the bids by the -- towards the end of December, mid-December. But because there has been such a level of interest in it, we're not going to get everyone through. We've just extended the bid deadline to I believe February 1 for that. So I think we had to extend that because there's too many people in there.”

Still no farm out for EG-31 even with so much interest and so many bids they had to extend the deadline.

Summary

As you can see we have multiple catalysts lining up for early next year

-Amalgamation with BTG bringing large dividends. Africa Oil will also screen much better.

-End of tax loss selling season

-3B/4B drilling

-Tamboti results

-EG-18 more exploration, Jasper Prospect, Farm-out

The stock is temporarily suffering from weak oil prices and tax loss selling. I think this is a perfect set-up for a rerating during the first half of 2025.