Cerrado Gold: Too Cheap To Ignore

They don't know about Cerrado(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian short AD: THE LINK

Get a 7-day free trial and the SUMMER SALE 60$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

If you sign up for 1 year of SA premium using my link, you will get a free one-year premium sub to my substack. Contact me and provide proof.

This article is long. Press “view entire message” when the article gets cut off in Gmail.

If you read my article “follow your ex-investments” you would know that I follow my ex-investments, and if you follow me on Twitter, you may know that I was in this stock briefly starting a small position at 34 cents in last december, averaged up, and then I sold it for a small profit in February at 46 cents, and during last month I returned and built a medium sized position in Cerrado at 63-65 cents.

Why this change of mind? Why re-enter at 37% higher price than I sold at? This write-up will answer these questions and more.

Cerrado Gold has a Gold mine in Argentina, a polymetallic(many metals) development stage project in Portugal, and an Iron Ore development stage Project in Quebec, Canada.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

Argentina gold mine NPV and FCF at different gold prices.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

Based on these images, the combined NPV of the company is 2.02 billion USD, and they make 61.1m USD of FCF per year at 3300$ gold(current price 3436$). The current market cap is 71.77m USD. The EV is 102.77m USD.

Now I have your attention.

Let’s go over some general info before diving into Cerrado’s financials, assets, and capital allocation plan.

Source: Google

This was/is a turnaround play, having already gone up +300% from the lows. The share price increase so far has been a combination of the gold price going up and the company’s deleveraging, with asset sales, which removed the bankruptcy fears.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

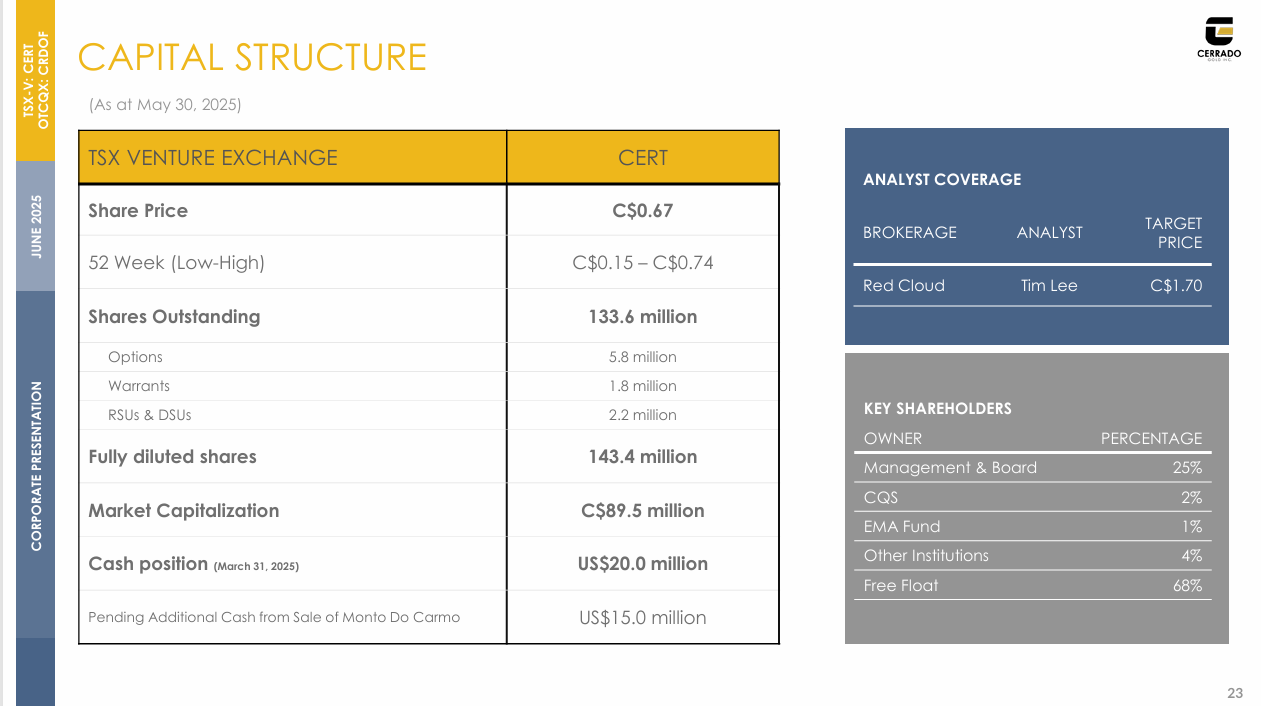

Clean Capital structure with a decent insider ownership of 25%, low institutional ownership, and low analyst coverage. Which is one of the multiple reasons for the current low valuation.

Balance Sheet

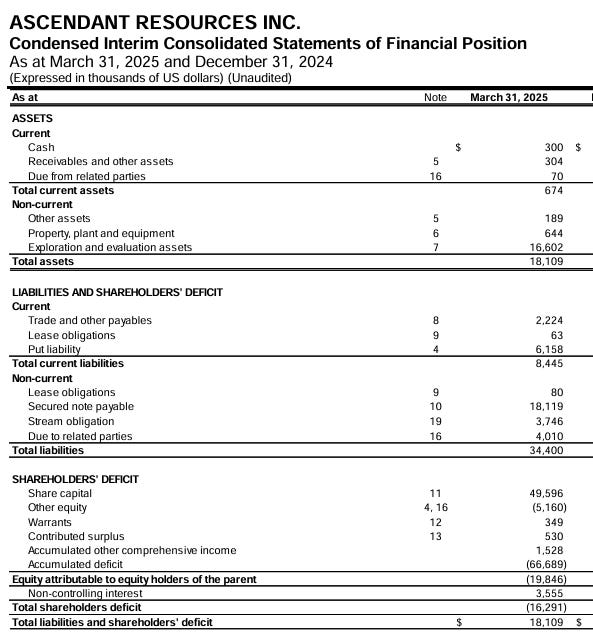

There are two balance sheets that are relevant because Cerrado recently acquired Ascendant Resources, which is not reflected in the Q1 Cerrado Balance sheet. This acquisition has closed, and the dilution from the acquisition is included in the current market cap.

Source: CERT-2025-05-29-interim-financial-statementsreport-english-3fdd.pdf

Source: https://ceo.ca/content/sedar/ASND-2025-05-14-interim-financial-statementsreport-english-4a6c.pdf

There are a bunch of different liabilities, and not all of them should be counted as debt, so I will break down some of these items.

Cerrado side: the 19m of provisions are for eventual mine closure, the 25m stream is accounted for in the costs

Ascendant side: Stream of 3,746m is a stream, 4m of related party debt for Ascendant is owed to Cerrado so that has been cancelled as aqcuisition has closed, 6,158m put liability is a potential sum ascendant may have to pay to acquire 20% of their main project if the company called MF&I decides to make Ascendant pay that, Ascendant owns 80% now, and 6,158m sum is 5% of the post-tax NPV using 10,5% discount rate.

To calculate the EV, I’m including cash and liabilities that are debt.

Now I’m rounding the cash number to 20m and rounding the debt numbers to 6.5m for LT debt, 4m for ST debt,10m for promissory note and 12.5m for prepayment facility, and 18m for Ascendant note.

Our EV is 71,77(Market Cap)+51(debt)-20(Cash)=102,77m USD EV

While this EV leaves out some real liabilities, it also doesn’t include 15m USD Cerrado will be receiving from an asset sale and a potential 10m USD from an option agreement in 2025-2028.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

15m is from the sale of their Brazilian gold assets last year. 45m have already been received, and the buyer is a big company that is solid financially.

10m USD from the option agreement is for a potential sale of some of Cerrado’s exploration properties that the company considers non-core assets in Argentina and can be received at any time before December 30, 2027. Cerrado has already received 4m USD from this option.

Source: Minera Don Nicolas Enters Option Agreement with AngloGold Ashanti Argentinian Subsidiary, Cerro Vanguardia SA, for the Sale of its Michelle Exploration Properties | Panorama Minero

Empire Building Management

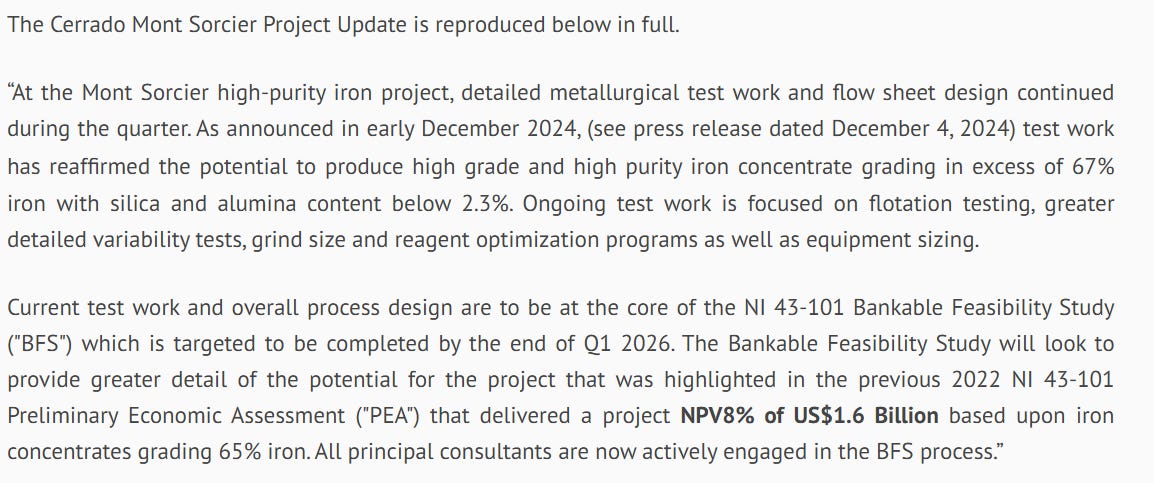

May 2023: Cerrado completes the acquisition of Voyager Metals using stock. 1.6 B$ NPV Mont Sorcier.

May 2025: Cerrado completes the acquisition of Ascendant Resources using stock. 147m NPV Lagoa Salgada.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

As a full ethnic Mongolian, I’m obviously fond of empire building. It’s genetic. But in the case of Cerrado’s empire-building, I have some premonitions about it. While Cerrado did some asset sales last year to deleverage and re-focus the company, based on the official plans the company is putting out, it seems that an empire is being built, and the question is whether Mark Brennan, the CEO, is more like Genghis or Kublai, and what is the quality of his horde?

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

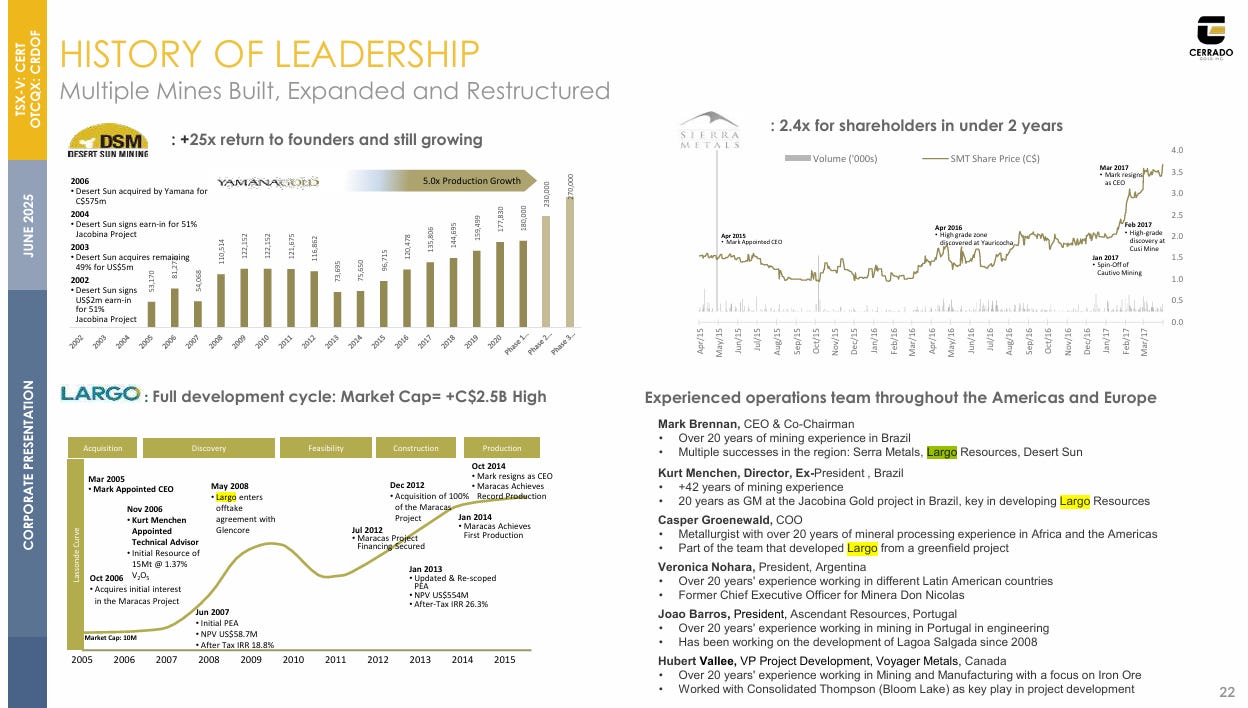

This management has taken it upon themselves to build a mine in Portugal, so it’s good to see a strong track record and experience in building a mine. The CEO, director, and COO all used to be at Largo Resources, and the CEO built a mine at Largo. However, I can’t let them get away with that Lassondo Curve BS(bottom left corner), that sort of visually tricks people into imagining the stock price would also look like that.

Source: Google

I didn’t take the exact days when Mark became and resigned as CEO, but those are the correct months, and while the stock is down a bit during his reign, it’s not too bad in the context of the commodity market. The stock went through the commodity supercycle bubble, the 2008 financial crisis, recovered, and then in 2014 commodity prices started dropping again, which caused the stock to drop right after Mark left, and the mine Largo had been building started production.

The CEO has built a mine at Largo, had success at Sierra and Desert Sun, and owns 5,756,422 shares, which is about 4.3% of the company’s shares.

As I said earlier, I sold this stock and then bought back in, and the reason why I sold was the acquisition of Ascendant and the plan to build a mine in Portugal. The reasoning was that it added risks and changed the thesis from “deleveraging with asset sales, focusing on core assets, buybacks, dividends, easy re-rating” to “building more mines with existing cash flow”. The first thesis was easy money at the current valuation. The second thesis has more upside potential, but the money is not as easy. And with cash flowing commodity stocks, I’m always looking for easy money. I’m not looking for a potential 10- 100x like with something like Aduro or Heartbeam. With stocks like Cerrado, my goal is a +50- 200% return and to take profits in 6-18 months and rotate to something else.

Source: AlmostMongolian

For those interested. I sold Africa Oil 2nd round couple of months ago. It’s cheap, but it doesn’t stack up with other opportunities. They have no motion. Total is dragging its feet with Africa Oil’s Orange Basin assets. Stall cityyyyy!

I still hate the Portugal acquisition. Even if it ends up being a great success, I will not say later that I should have supported it. Based on the information I had at the time and have now. It clearly raises the difficulty level of the money. We were on level 1 difficulty of money, and then they raised it to level 2 with some extra rewards for shareholders if they beat level 2, but I want them to play on level 1, because this is mining, and level 1 is difficult enough.

And the market agreed with me on this acquisition. I got out at 46 cents when it was announced, and right after the stock fell back to 35 cents. The gold price and developments with the Argentine gold mine have caused the subsequent recovery. The stock has gone to 74 cents now despite the acquisition, not because of it.

And I can’t ignore the fact that they acquired a related party and its implications. Was it the best acquisition they could have made that just happened to be a related party that was founded and chaired by the CEO of Cerrado?

The optimistic argument would be that the CEO knows the asset inside and out, and knew it was undervalued, and it was only a modest premium, and it was a shrewd play because the dirt on the project has metykogplfinic rock, which means with more drilling it will quadrupple the research. You must do your research.

The pessimistic argument would be that the CEO bailed out his failing Portugal project by using his cash-flowing company Cerrado, and is now using Cerrado’s cash flows that could be going to, for example, massive buybacks for his risky pipe dream, possibly for emotional and selfish reasons based on his long involvement with the Portugal Project and his own shareholding in it prior to the acquistion.

Source: https://ceo.ca/asnd

This is the stock performance of Ascendant before Cerrado acquired it. Later in the asset deep dive section, I will talk about this asset more. Even some positive things.

Their Capital allocation plan also includes stock buybacks. They have a normal course issuer bid in place, but they have not been utilizing it.

Source: https://ceo.ca/@accesswire/cerrado-files-notice-to-implement-normal-course-issuer

In February, they said they would start the buybacks once the acquisition closed. It closed, and they haven’t bought back anything. June 2nd, according to some guy in ceo.ca, they are supposedly starting it after the underground development goes according to plan, and I will not verify this information.

Source: tsxventurewatch, ceo.ca

This is starting to sound negative, so it’s time to move on to why I like this stock and why I bought back in, which is due to their other assets and some recent developments with those assets. If they never acquired Portugal, and this company would be just Argentina and Quebec, this would be a top 3 position of mine; now that they did, it’s 7th among the 11 positions in The AlmostMongolian portfolio, which is still a major achievement for any company. Only around 0,00099% of the world’s companies ever get there.

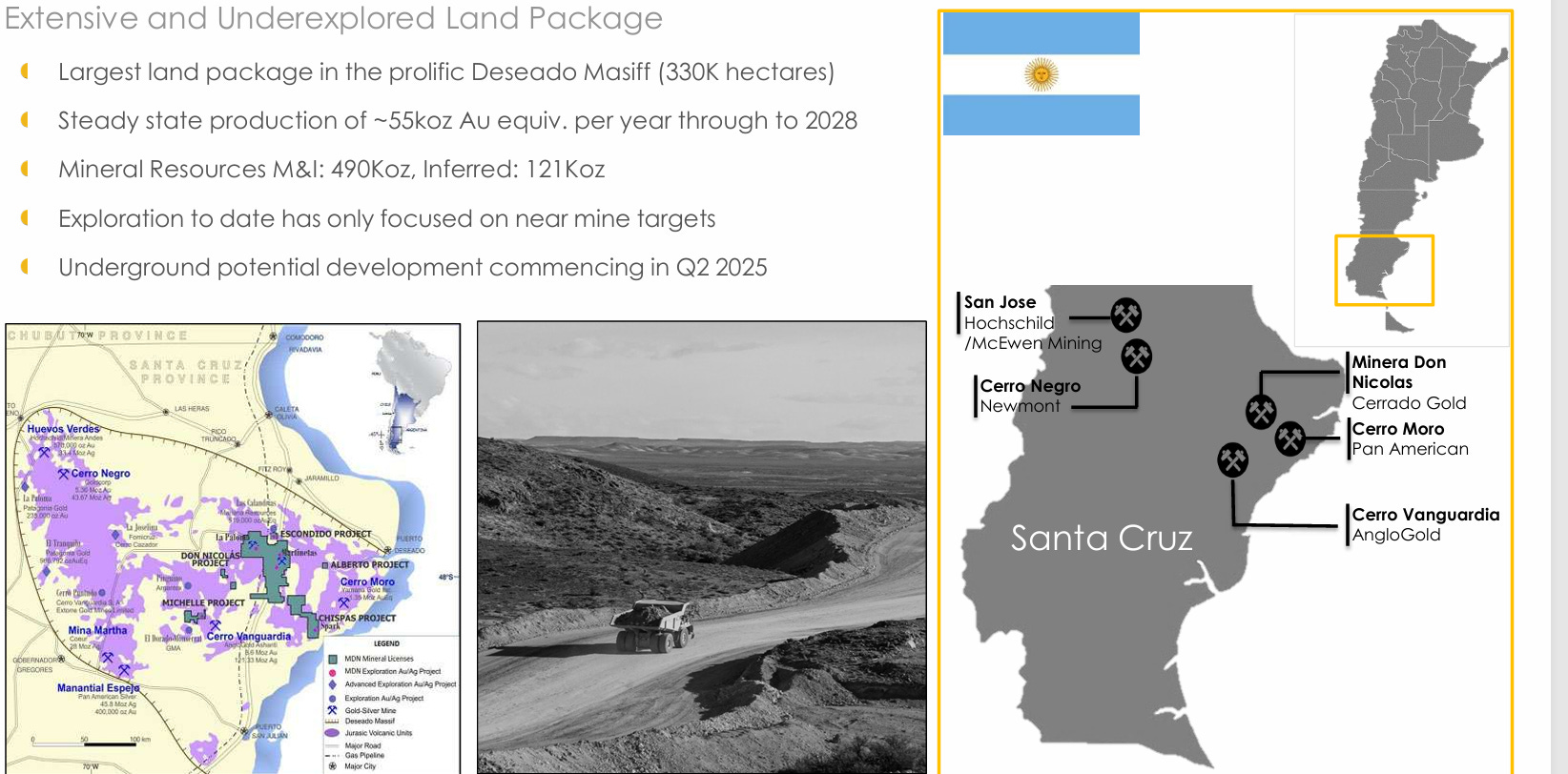

Argentina

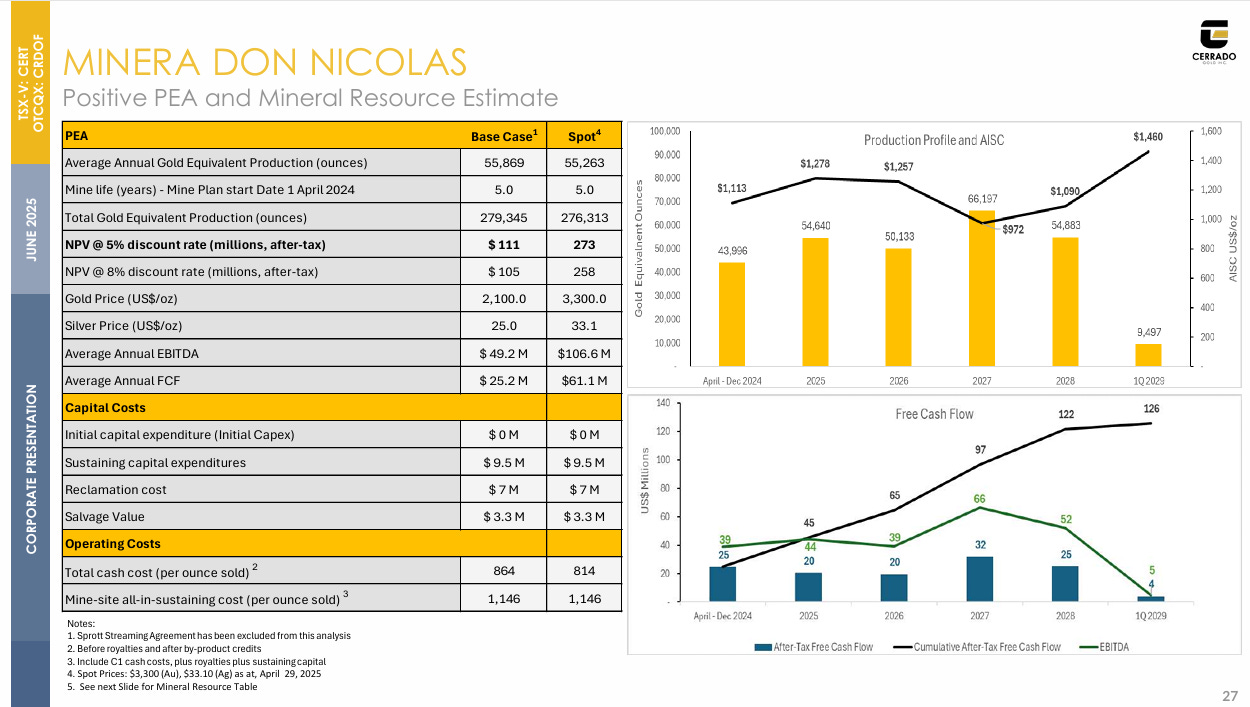

The Argentina gold mine, Minera Don Nicolas, which I will refer to as MDN for the rest of the article, is the core of this investment thesis. If the gold price hovers around 2500-3500$(current price 3452$) and Cerrado doesn’t fumble operationally, the stock is very cheap based on just MDN.

Source: https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

At 3300$ gold and producing 55,263k GEO(gold equivalent ounces) per year, they make 61.1m USD of FCF. Their guidance for 2025 is 55-60k GEO. The company uses GEO because the mine also produces some silver, but the majority of revenue comes from gold.

With this lower than the current gold price and the low end of production guidance number, the P/FCF=1.17 and EV/FCF=1.68 (using my EV calculation)

MDN 111m USD NPV at 2100$ gold and 273m USD NPV at 3300$ gold. NPV is not that high because, at the moment, the official LOM(life of mine) is only 5 years. Cerrado is working on extending that significantly. To be honest, I don’t care about NPV, because I’m not a nerd with science books and a calculator going “Erm, what is the NPV on this?”, “I need to calculate the NPV before investing in anything”. I don’t even know what NPV means.

Whatever NPV is, Cerrado has 2,02 billion USD of it: Argentina 273 m+Portugal 147 m+Canada 1,6B. Huge discount to market cap and EV. Usually you see discounts like this with companies that have a development project, but no cash flow, because the market is taking into account the fact that a company will have to do a lot of dilution or give up a large % of the project to a larger company to be able to develop it, but Cerrado has significant cash flow and lender support for project development.

There is a lot more potential in MDN than 55k ounces per year and 5 years of LOM, as it’s shown as the base case on the slides. A collection of factors caused the past 12 months’ financials not to be as good as one would think based on the gold price, and I will go over why that is and why Cerrado is projecting much higher cash flows going forward, starting with Q2. Some of these factors are definitely going to improve their numbers, and some are up to Cerrado to execute.

MDN production growth

Last year, Cerrado produced 54 494 GEO. Their original guidance for 2025 was 50-55k GEO, but in the Q1 production update PR, they announced that they are increasing the guidance to 55-60k. Which caught my attention at the time, as I was still rationalizing not investing in Cerrado at the time.

One reason for the low valuation is that the market doesn’t seem to trust Cerrado reaching its guidance. Their production dropped from 16,604 GEO in Q3 2024 to 10,431 GEO in Q4 and 11,163 GEO for Q1 2025, which means there needs to be a large production increase to achieve the guidance.

Q1 production annualized would be 44 652 GEO. If the company achieves the low end of the guidance, 55k for 2025, the rest of the quarters should average 14 612,33333333k GEO per quarter (14 612,333333*3=43 836,999999+11 163=55 000).

Let’s see why the production dropped and their plan to get it back up and from there to record levels.

The reason for the drop: “Operational results for the fourth quarter demonstrated a decrease in production relative to Q4/23 as high-grade ore to the CIL plant declined as mining from the Calandrias Norte pit was completed, and as the operation transitioned to focus on heap leach production. Ore from the Calandrias Norte open pit was exhausted late in the quarter and is now being replaced by processing lower grade stockpiles through the CIL plant.” Annual results PR

This Pit with high-grade ore was completed in Q3. Now they are transitioning to “Heap Leach” production and underground production. Heap Leach is a method for processing low-grade gold ore by spraying cyanide on it. This caused a dip in production, and if they are successful, the production will reach record levels in 2025 with these two production methods ramping up.

Source: Cerrado corporate presentation with AlmostMongolian correction with paint

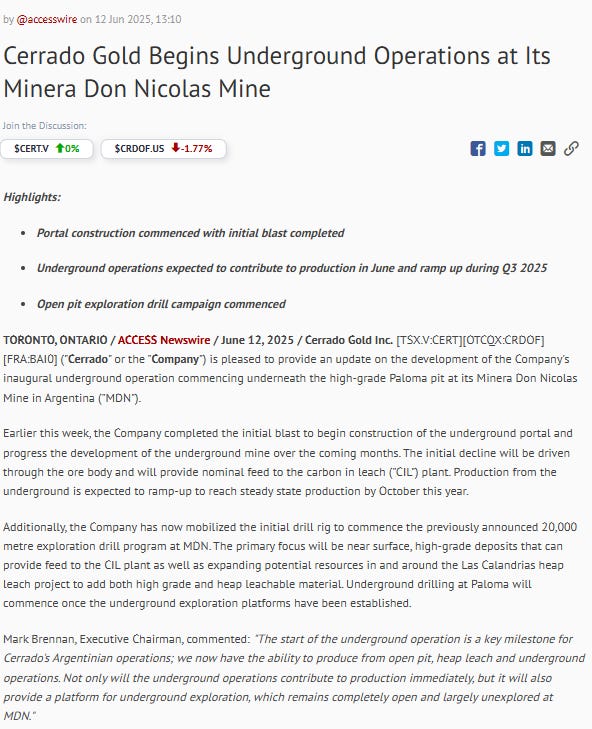

I had to correct Cerrado there It’s June 2025 not 2026. They just press released it.

Source: https://ceo.ca/@accesswire/cerrado-gold-begins-underground-operations-at-its-minera

“Production from the underground is expected to ramp-up to reach steady state production by October this year.”

The underground won’t have a significant impact on production until Q4, maybe Q3. The delivery of the guidance will depend on the combination of UG and HL ramp-ups.

““The focus at MDN remains to ramp up production rates at its heap leach operation to 4,000-4,500 GEO per month” (Source: Q1 earnings PR). This would take them to a 48- 55k annual run rate for Heap leach. In Q4, they got to 6,897 from Heap leach and 2,800 in March.

They have installed stuff to support increasing HL production. “The addition of the new crusher circuit was completed just after quarter end, providing increased ore availability to the pad. While supporting higher production, additional crushing facilities are also expected to reduce the feed size to the pad and thus improve recoveries. As the reduced size feed and larger pad stockpiles are leached, it should lead to higher production rates and unit costs are expected to decline as a result.” Q1 earnings PR

“Operational results for the first quarter saw gold production in line with Q1/24, with the heap leach operation reaching a new production record of 6,897 GEO for the quarter. The expanded crusher is now fully operational and the quantity of ore being placed on the pad has increased. With higher gold prices, the CIL plant continues to process lower-grade stockpiles and is planned to continue processing low grade stockpiles through Q2/25, after which it will be blended with new high-grade material from the underground mining operations which will increase the average grade throughput at the mill.” Q1 production results PR

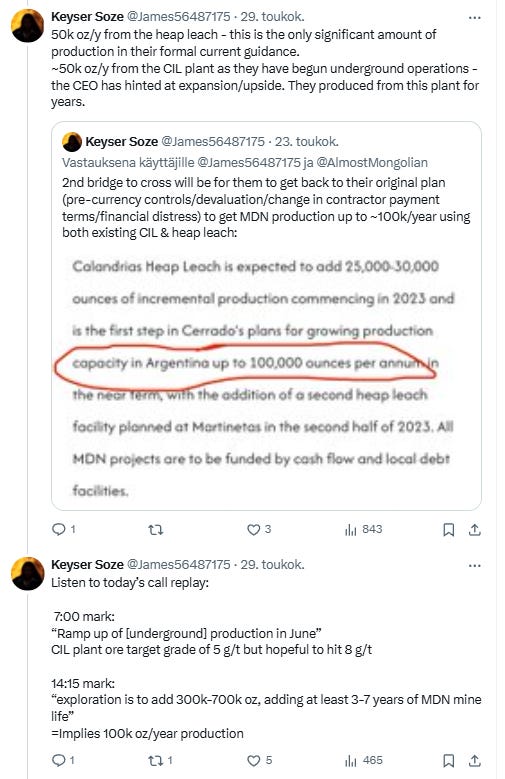

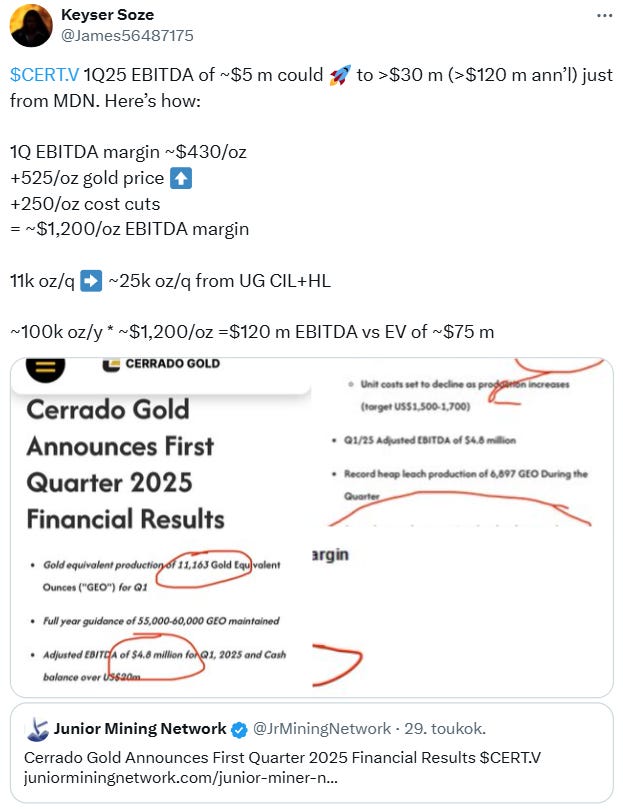

What I’m more interested in is the production rate they can get to after both UG and HL have ramped up. The exit production rate of 2025, as the guidance is assuming a high production increase in the 2nd half of the year. At the current gold price, there would be insane cash flow potential. Keyser Söze in Twitter from that movie here makes a case for a potential 100k per year. I had to correct his username there.

Source: Keyzer Söze

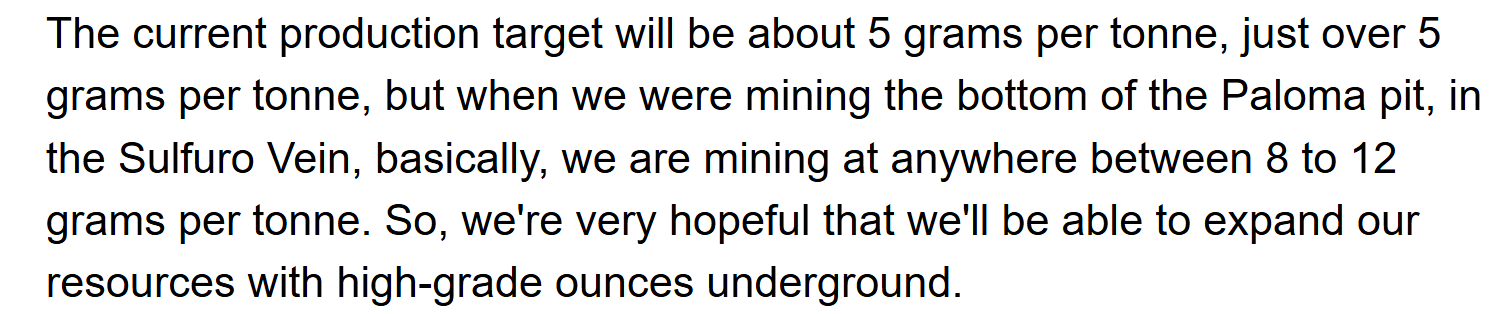

Here are those full quotes from the Q1 earnings call transcript. Very convenient to look at transcripts from my Seeking Alpha Premium.

Source: Seeking ALpha PRemium

Here is Keyser Söze making calculations of how much Cerrado could make at that production level.

Source: Keyser söze

I’m not assuming they will reach 100k. I’m happy if they can reach their guidance while increasing LOM. But this is something that’s possible with Cerrado’s infrastructure, according to them, and if the UG is successful, I see it as a realistic possibility.

“Just to remind everybody, we're producing 55,000 to 60,000 ounces per year currently. Our expectation, our hope is that we can grow our mine life first, and then second of all, look to expand on that production base. We have a 1,200 tonne per day CIL plant that is largely unutilized and underutilized. So, from that perspective, we have the capacity to produce a lot more. That's the importance of having high-grade material going through that plant. It will really just add substantially to our bottom line and reduce our operational costs dramatically” Q1 earnings call

Hedges

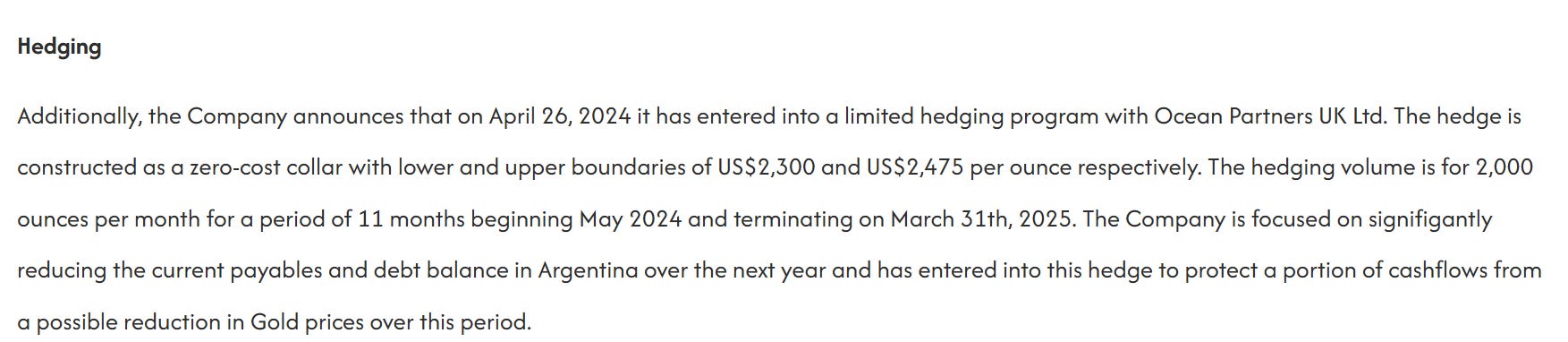

Q1 2025 Cerrado realized just 2,520$ gold price per ounce while the gold price averaged above 3000$, and the reason is old hedges.

Source: https://www.juniorminingnetwork.com/junior-miner-news/press-releases/2931-tsx-venture/cert/159970-cerrado-gold-announces-q1-gold-production-results-for-its-minera-don-nicolas-mine-in-argentina-2.html

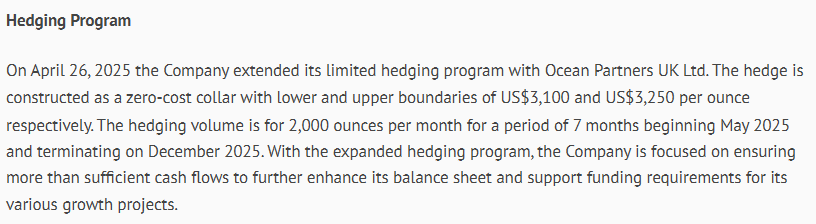

Cerrado was hedging more than half of their gold production in Q1 at lower gold prices, and this hurt their numbers in recent quarters, but the positive thing is that 31.3.2025 this program was terminated, which means the whole Q2 Cerrado is realizing prices above 3000$. They did enter into another hedging arrangement at higher prices of 3100$-3250$ again for 2k ounces per month.

Source: https://ceo.ca/@accesswire/cerrado-gold-announces-first-quarter-2025-financial

While these hedges limit Cerrado’s upside if gold goes up, I actually like them and wouldn’t mind if they hedged even more of their production at current prices of around 3400$, and the reason for this is that they make great money at these prices. The market is not pricing in their earnings above 3k gold.

I’m neutral on the gold price. I’m not a bull or a bear on gold. If they can lock in amazing cash flow after the gold price has surged, I like that. I would be willing to miss the gold price upside to limit the gold price downside if I have no opinion about the direction of the gold price.

The old hedges rolling off will improve Cerrado’s results going forward, regardless of their operational performance.

Production costs

Cerrado is predicting falling AISC(All-in-Sustaining-Costs) per ounce going forward.

Their AISC in Q1 was 1,932$ per ounce. And in the Q1 earnings release, they guided 1,500-1700$ AISC per ounce for 2025.

“Going forward, as rental equipment is replaced, a more stable fiscal environment materializes and production increases, costs are expected to decline.” Q4

The predicted decrease in production costs is attributed mostly to increasing production. There is also the rental equipment that is being replaced by Cerrado’s own equipment, which should decrease costs, but I haven’t found the exact financial impact of it. The removal of currency controls in Argentina will also help with costs.

Costs down, pricing up, production up. 61m USD of FCF at 55k per annum. Even bigger factor this year than the earnings is their success in increasing the resource and succeeding UG. That’s how they can get a real revaluation. They need to have story of long term production from their assets. That’s what needed to happen with Valeura as well. If the market doesn’t believe the company can produce for +10 years from their high cash-flowing assets the market will always have an excuse to put a massive discount on the stock.

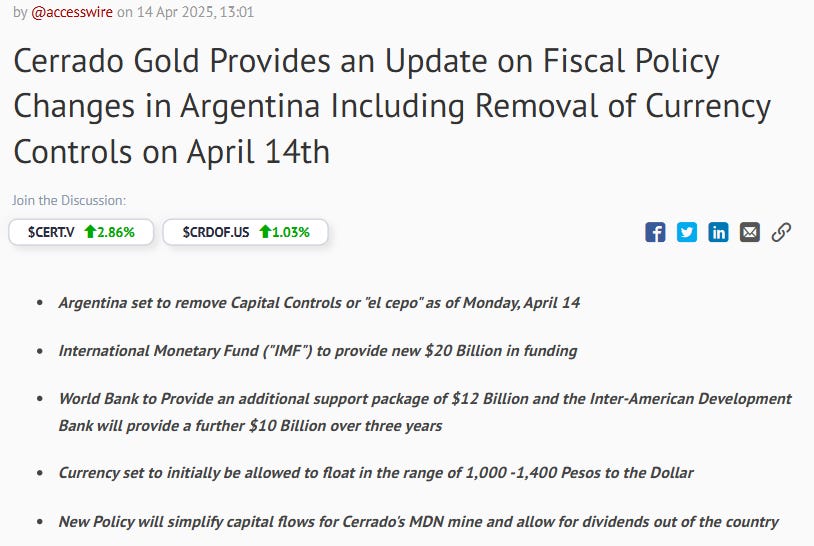

Argentina currency controls

Source: https://ceo.ca/@accesswire/cerrado-gold-provides-an-update-on-fiscal-policy-changes

This was one of the things that got me to re-enter Cerrado. This was expected to happen at some point as the new libertarian president had this goal, but when we are talking about politics sometimes promises made are not promises kept so I was not expecting it to happen this soon.

This has many benefits, first being that Cerrado can now easily get money out of Argentina and, for example, pay dividends.

“As part of this phase of removing all Capital Control on Friday, the government announced companies will be able to repatriate profits out of the country as of 2025, subject to some restrictions and the use of the differential exchange rates or "dollar blend" used by exporters will be eliminated and the deadlines for the payment of foreign trade operations are to be relaxed. This is expected to attract new investment into Argentina. Funds from prior to 2025 will need to exchange the debt for dollar-denominated security bonds. Individual Argentines will also be able to legally exchange pesos for dollars without a US$200-monthly limit.” 14.4.2025 Cerrado PR

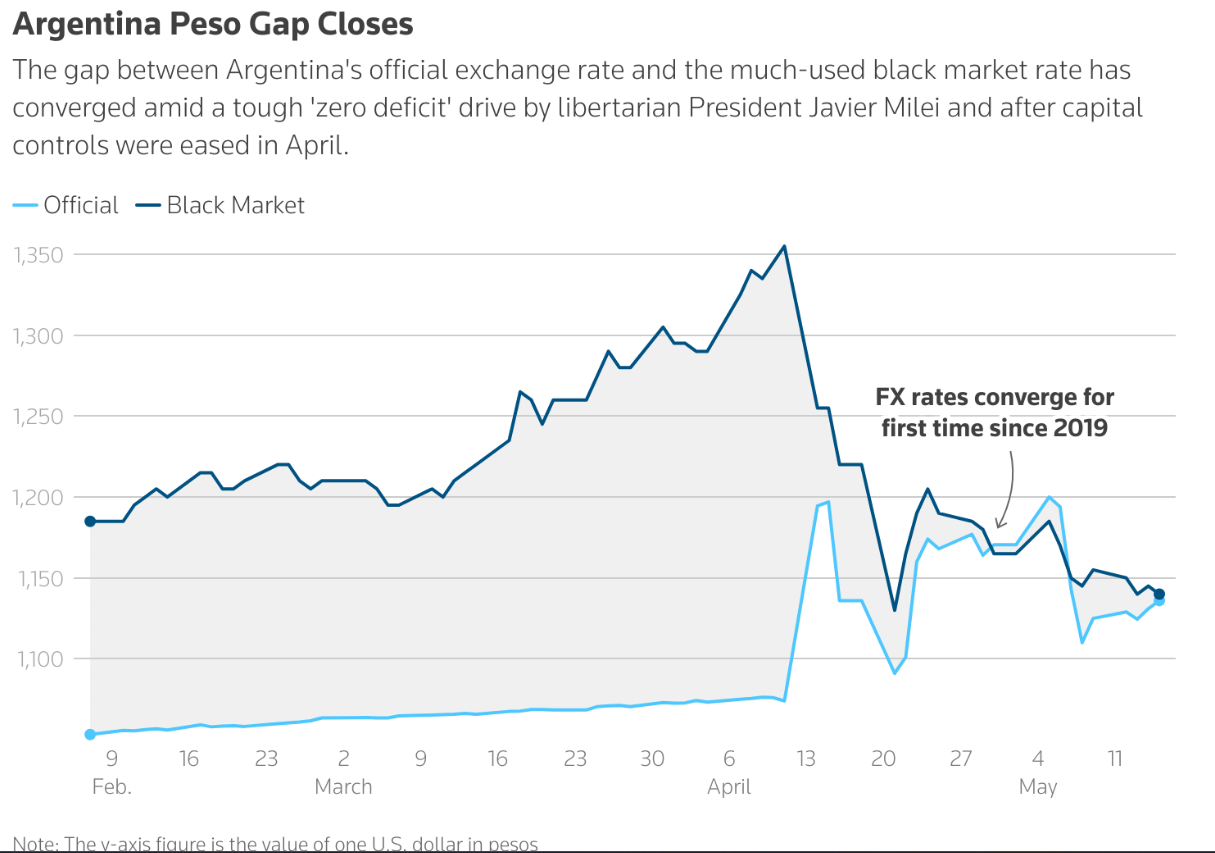

Source: https://www.reuters.com/markets/currencies/argentinas-black-market-dollars-falters-currency-controls-are-eased-2025-05-16/

The old currency control regime hurt miners’ purchasing power and profitability because miners were forced to convert USD export earnings to Peso at an inflated official rate, which overvalued the Peso in comparison to the real black market rate.

For example, Cerrado would export gold and get USD, and then need to convert that into Peso at the official inflated rate to spend it in Argentina to pay for salaries, equipment, etc. And they would not get the full value of their dollars because of the official rate, but now this isn’t a problem as the official rate and the black market rate have finally converged due to this policy change.

“Along with the opening of the foreign exchange market, modifications were also introduced for foreign trade operators. From April 14, importing companies will be able to pay immediately for goods arriving in the country, eliminating the need to wait weeks or months as was the case with the previous system. This flexibility will be applied without distinction of products. The new scheme also impacts the payment of services acquired abroad, such as streaming platforms, online training or consultancies. According to the provisions, if the service provider does not have a corporate relationship with the buyer, payment may be made from the first day of use.” 14.4.2025 Cerrado PR

For a mining company in production growth mode, importing equipment from outside of Argentina all the time, not having to wait for weeks or months for that equipment, is very beneficial.

There are many other benefits too and in general it just makes Argentina a better operational environment and a more attractive investment destination and will also help the market valuation of companies operating in Argentina as perceived and real risks are reduced.

For long-term holders there is a risk that the libertarian president does not get re-elected. His term ends 10.12.2027. I doubt I will be holding Cerrado that long. I don’t usually plan to hold commodity stocks for a long time. I have a thesis for a revaluation, and I will move on when that happens or if I see a better opportunity.

Milei also has a strong chance of getting re-elected if he defeats inflation. He has already managed to reduce it a lot, and he is one of the more popular presidents in Latin America.

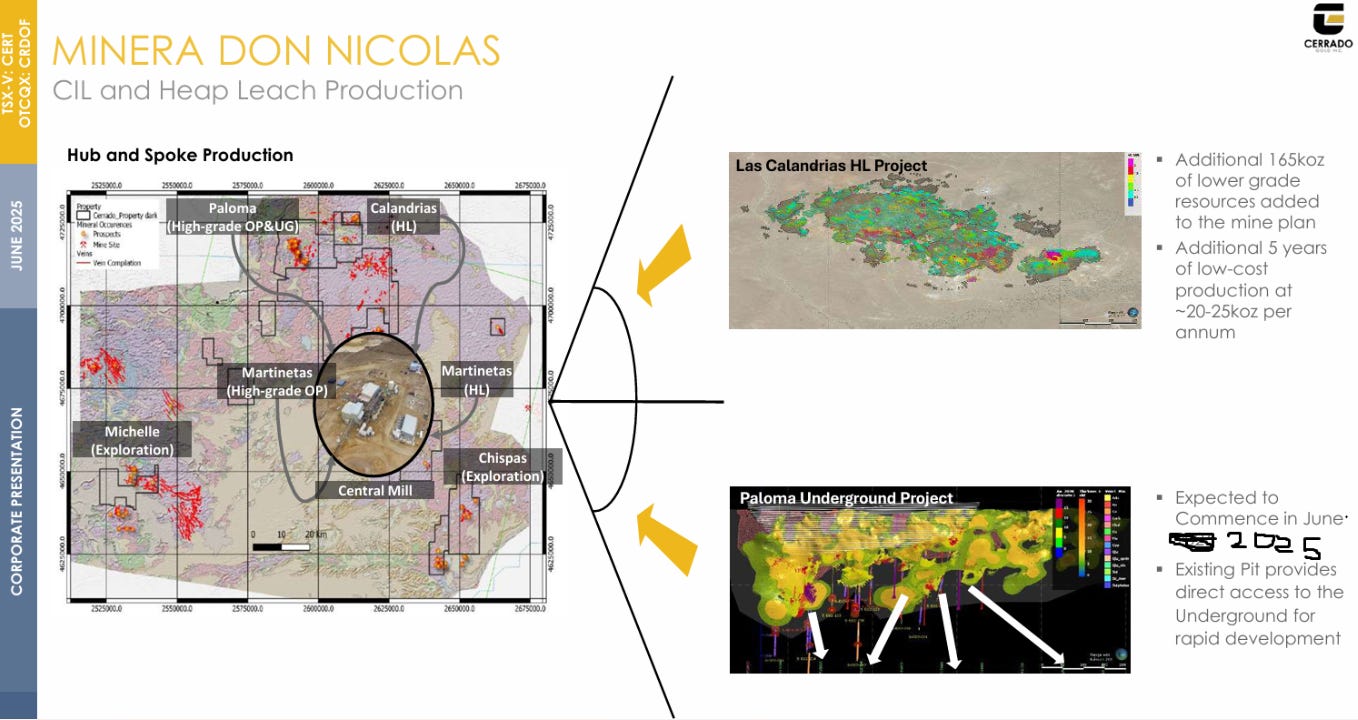

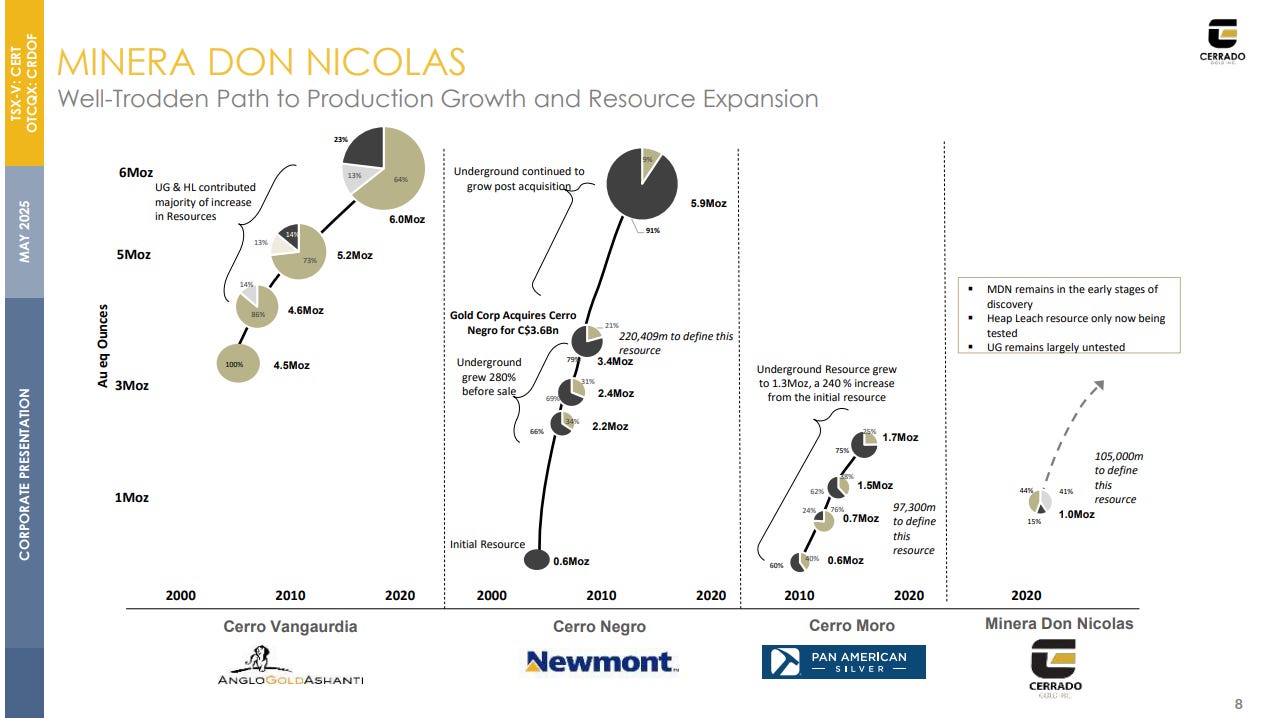

Life of mine(LOM)

The official LOM is 5 years. How are they planning to extend that?

Source: https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

See how the small circles lead into bigger circles. It shows how some of the nearby mines have increased their resource by going underground, which is exactly what Cerrado is doing. I showed the PR from 12.6 earlier; the UG operations have started.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

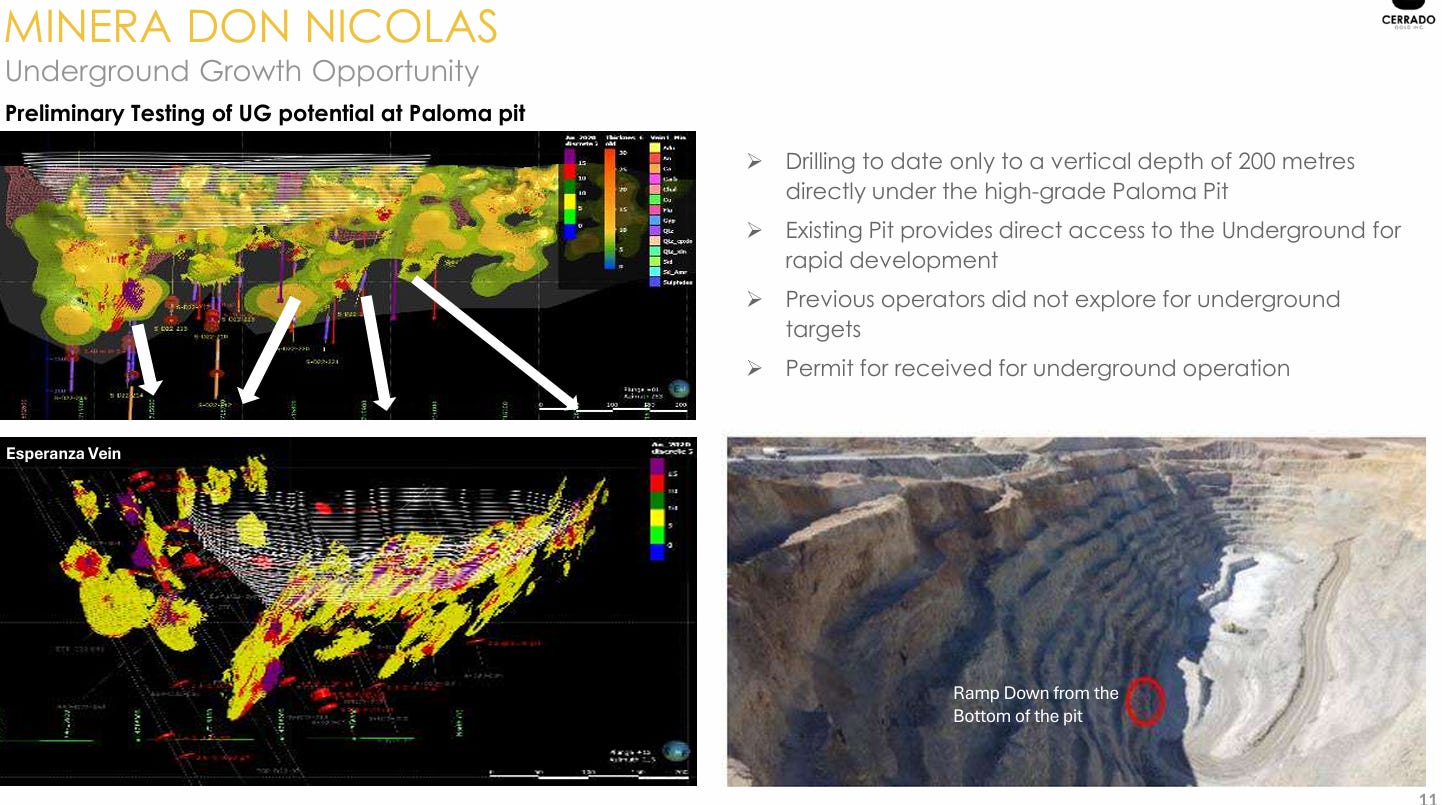

Here is the plan for the underground developments. Here is some maps, pictures and graphs.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

They are going in from the red circle there. That’s the spot. They are going to dig down from there to find gold, and the resource is going to increase.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

You see the middle picture. There is the open pit above, and that’s where they are mining right now. Under it, you see the yellow, green, and turquoise colors. That’s all gold, I think.

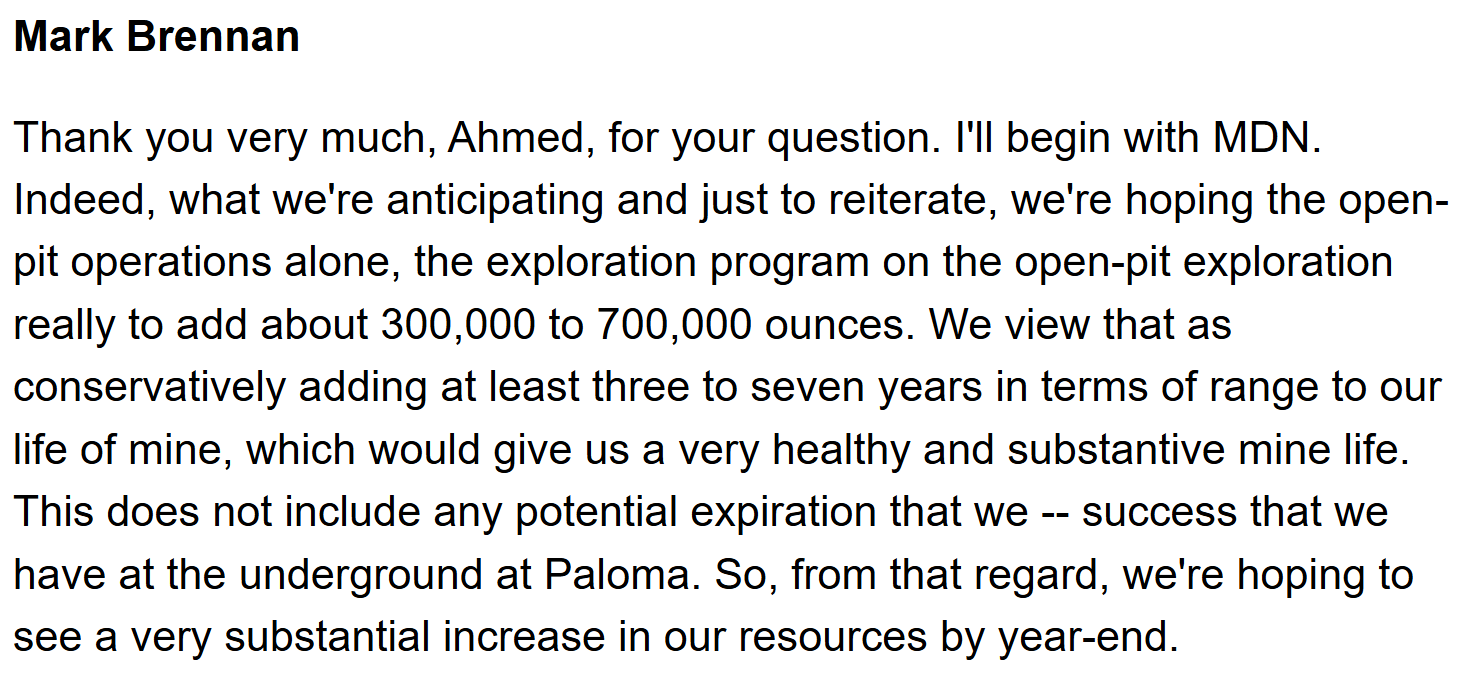

Their current 20,000 metre drill program that they “conservatively” expect to multiply their mine life, does not even account for the Underground potential.

“we're anticipating and just to reiterate, we're hoping the open-pit operations alone, the exploration program on the open-pit exploration really to add about 300,000 to 700,000 ounces. We view that as conservatively adding at least three to seven years in terms of range to our life of mine, which would give us a very healthy and substantive mine life. This does not include any potential expiration that we -- success that we have at the underground at Paloma.” Q1 earnings call

If they achieve 300-700k it would be a huge catalyst considering their current official resources that are: Measured & Indicated resource is 490k and inferred 121k.

. Source: Wikipedia

After this 20,000 metre open-pit drill program, Cerrado is planning to explore more underground, where they are targeting high-grade “veins” after they start underground production.

To summarize Argentina a bit. Currency controls, hedges, transition to heap leach have caused recent financials to be lackluster, but going forward these things are being removed from being a problem(hedges, currency controls) or they are being turned into strength (successful HL ramp up). The gold price is surging. Underground operations are starting with the potential to transform the company. An open pit drilling program has started, which the company expects to significantly increase LOM.

Portugal, Lagoa Salgada, 80% ownership

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

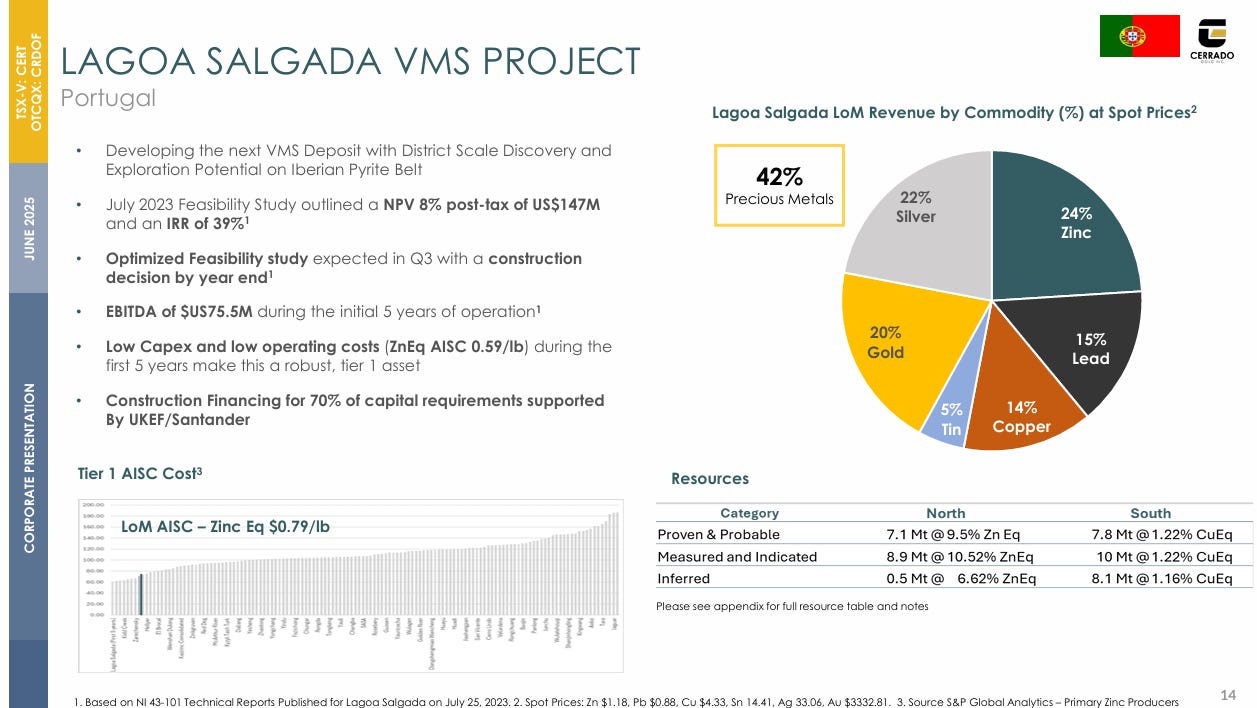

Lagoa Salgada is my enemy, but I will cover it nonetheless. It’s kind of a mix of metals, polymetallic, they say, even Tin in there. Remember tin?

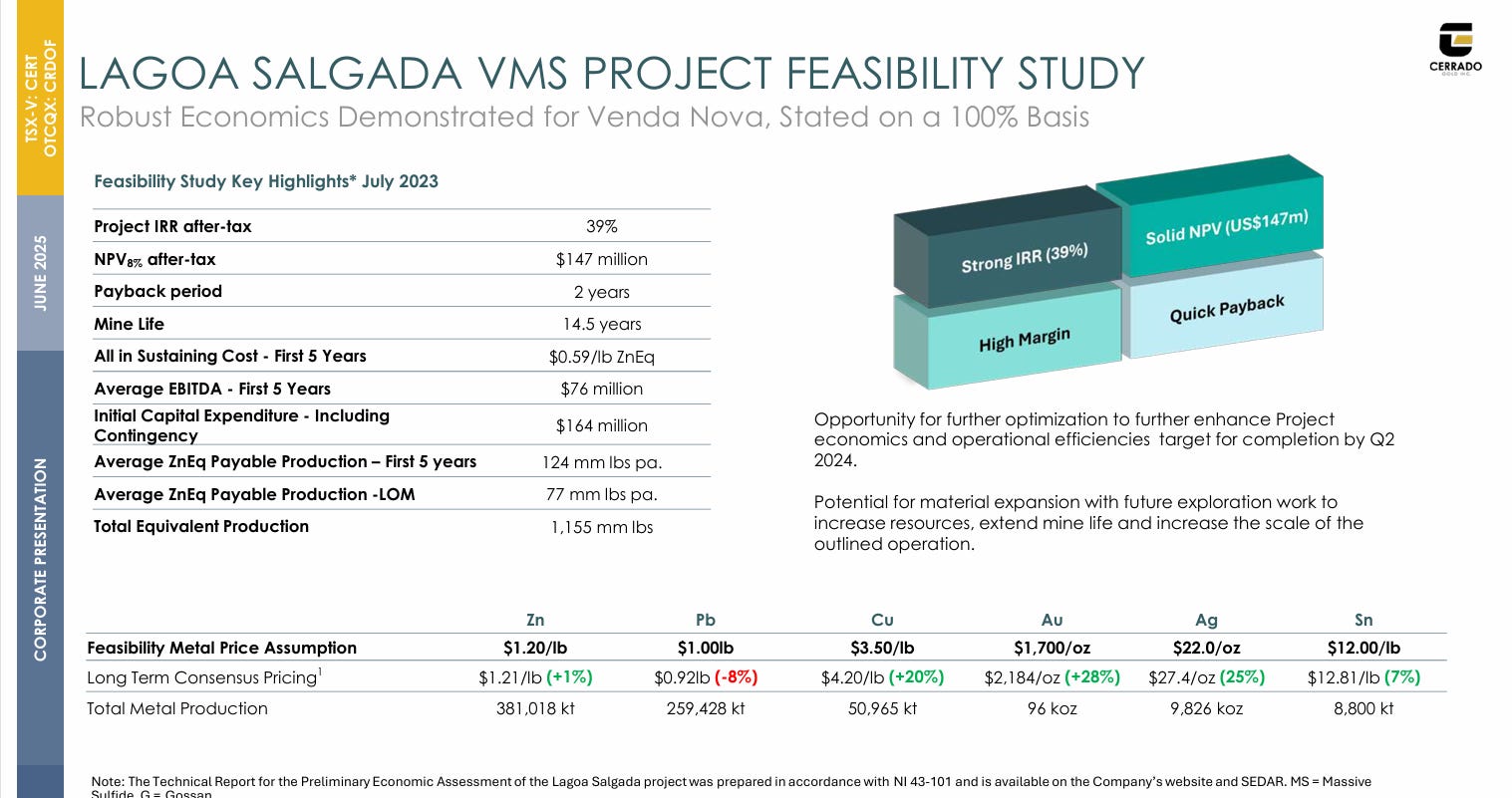

From the bottom left corner, you can see that Lagoa Salgada has low costs. IRR(Internal Rate of Return) of 39%, which is good.

The NPV of 147m and the EBITDA of 75,5M USD reflect much lower metals prices because they are based on a Report published July 25, 2023. Here is the full insanely long NI 43-101 report: Link to the report

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

Zinc and Lead prices are around the same now as in the feasibility study assumptions, but Gold, Silver, Copper, and Tin are all much higher. Especially gold trades currently more than double the feasibility price. Their goal is to publish updated feasibility report in august, which will show higher NPV and EBITDA projections: Is that going to be a catalyst? Maybe I’m not sure if that’s priced in or not. It should be, but a lot of investors don’t figure out these things and this is mostly retail held stock.

“Upfront capex requirement of US$164 million (including US$12 million of contingency)” Lagoa Salgada Capex according to Cerrado’s Website.

Not much of that is projected to be spent on Lagoa Salgada this year. The big capex spending starts in early 2026, which is Cerrado’s goal to start construction. Even with Cerrado’s strong cash flow, this needs external financing, and this is how Cerrado has planned it.

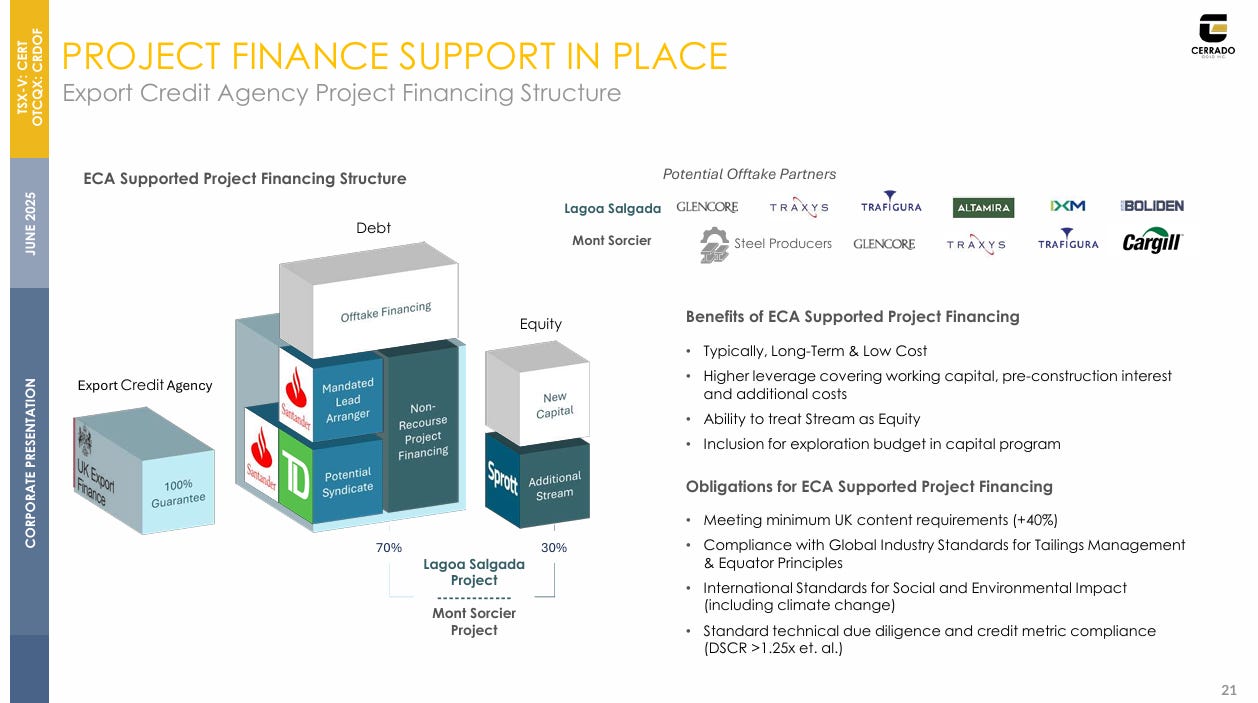

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

Look at all of these boxes. Let’s hear it from the CEO instead of from the boxes.

“We have very strong support from the UK export credit agency as well as banko Santander uh to fund the project on a se to provide project capital of about 70% of our capital requirements through very lowcost debt lowcost long-term debt um and and we'll be utilizing that uh to to to really uh limit whatever dilution it will be required We're also working with Sprat uh streaming Sprat streaming have already a stream on this project Uh they're extremely supportive Would like to look at adding to their stream Um so we're you know we expect we'll be able to get an offtake on this project” May 6-8 Metals & Mining Virtual Investor Conference

If they get 70% of the Capex from long-term low-cost debt, that would limit or remove the need for dilution if the gold price holds up and the company delivers on production.

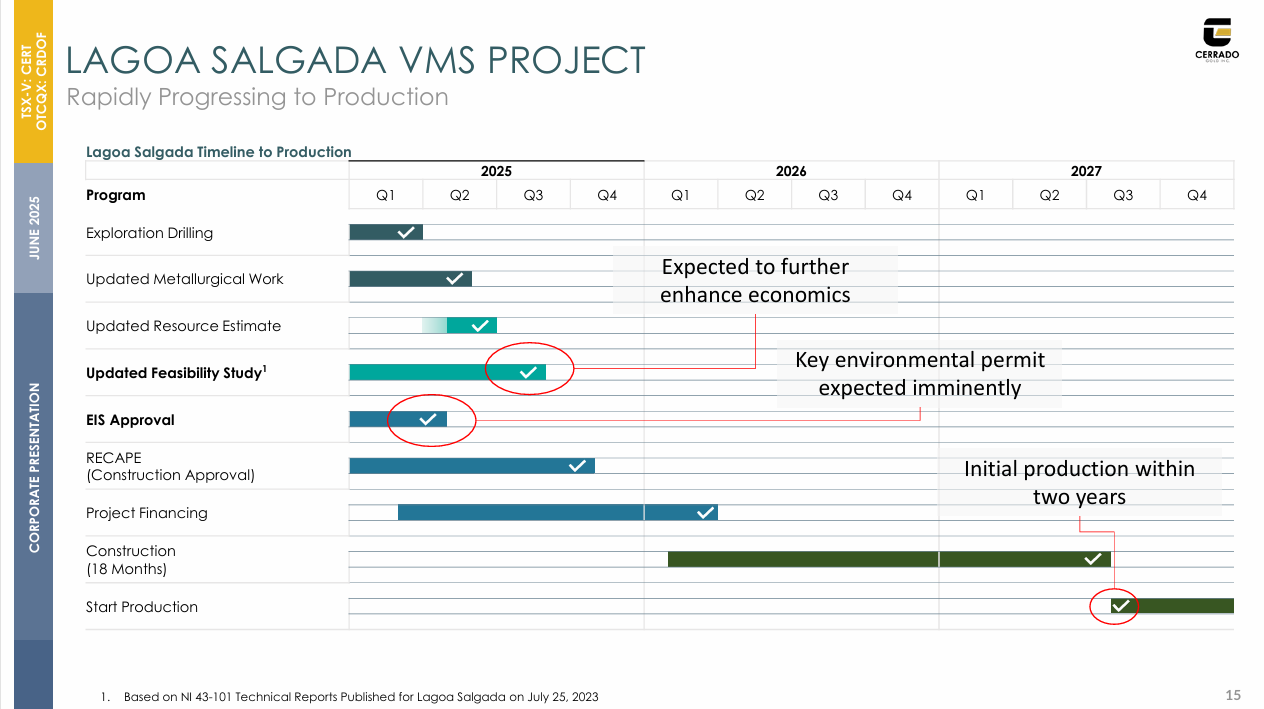

Cerrado is looking to put this into production with this timeline.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

There is one imminent positive catalyst or possible bearish event and that is the Environmental Impact Assestment Approval and we should be getting this announcement basically now.

“We expect our environmental impact assessment approval imminently. We have received initial notification that the approval process is coming to its conclusion. And so, we'd be able -- we expect to be able to announce that very shortly. And that will follow up with the feasibility study sometime in the July-August period, with the publication of the feasibility report in August.” 29.5.2025 earnings call

It’s more than 2 WEEKS from this call, and we are angrily/furiously waiting, growing angrier by the day.

The news releases like the one below are also spooking the shareholders, so we are not only angry, we are spooked as well.

Source: https://alentrium.pt/en/este-projeto-nao-deve-avancar-peticao-contra-mina-da-lagoa-salgada-reune-mais-de-2-mil-assinaturas/

I really need these people to stop resisting. I don’t like people standing between me and my money.

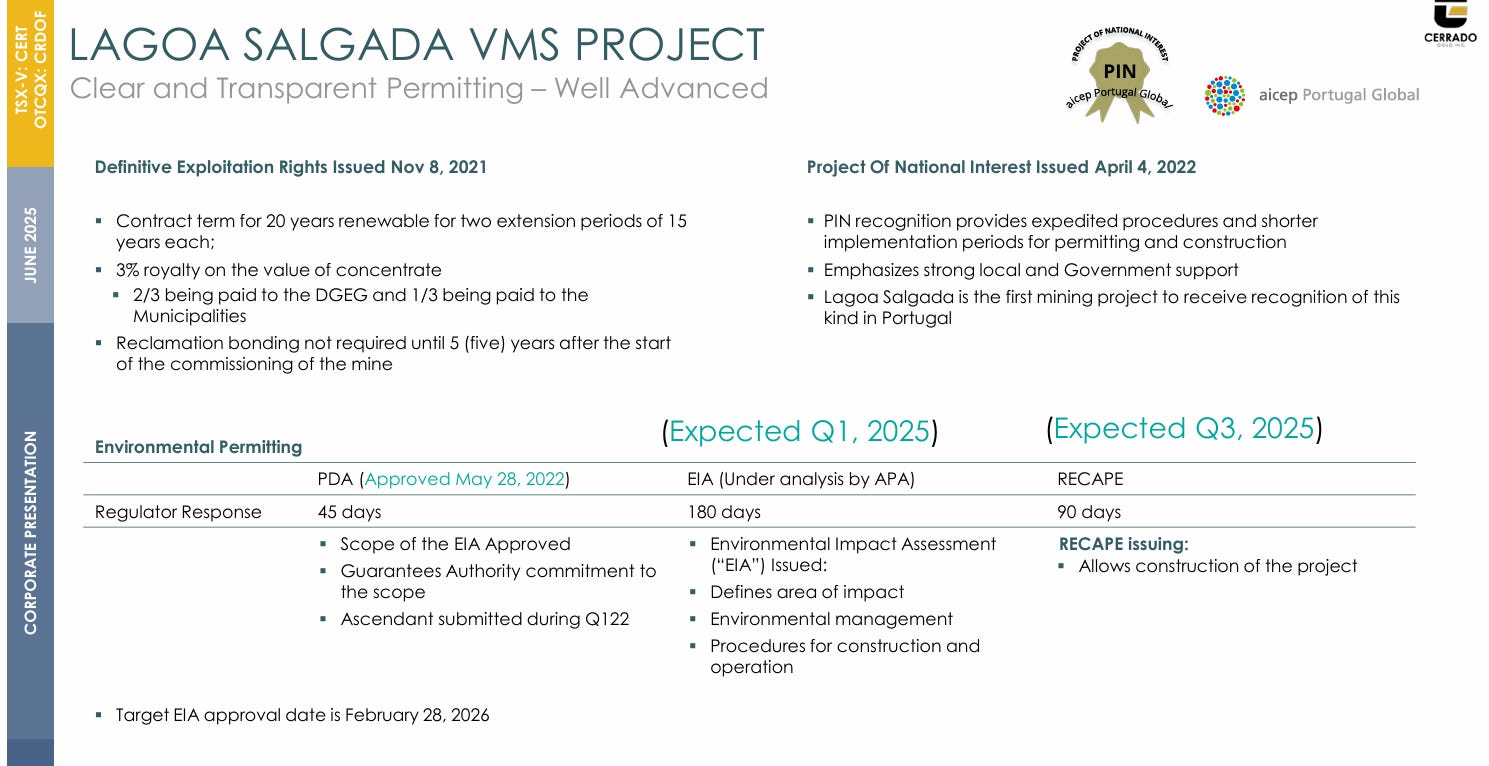

While there are opponents, there are also supporters. Lagoa Salgada is the first mining project that has received the title of Project of National Interest in Portugal.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

“On April 28, 2022, the Company announced that the Lagoa Salgada VMS project (the “Project”) has been recognized by the Portuguese Government as a Project of National Interest (“PIN”). The award, dated April 4th, 2022 is based on various economic, environmental and social factors and its positive impact on the local Municipalities covered by the mining concession, the surrounding region and for Portugal. “ Q1 MD&A Ascendant

Here is the CEO reassuring a concerned shareholder in the earnings call: “As it applies to your question with regard to permitting in Portugal and Lagoa Salgada, we feel very similar to MDN on this project. First of all, we will have the strong support of the local and the federal government. We're a project of national interest or PRIN project, which means that we have the strong support of the local community, the local government, as well as the federal government. And we expect to see our EIA permit announced within the coming days, if not weeks. So, we're very optimistic about that.”

On top of the EIS approval, they need to get construction approval, and they are targeting that for November or the late 4th quarter.

We’ll see. They are very optimistic. I think it’s more likely that they get the permits than not. If they don’t get the permits for this and the stock falls a lot, I’ll likely buy more because I’m only in this stock because of Argentina and Mont Sorcier as a bonus.

Now onto the Geology section of the Lagoa Salgada Section, which I hate, because I don’t know anything about geology. However, in my opinion, geological knowledge is unnecessary when investing in mining. Just listen to your heart.

They have three slides about Geology here. I don’t want to pad this article out unnecessarily with those slides because I have no comments of value about them. I don’t want to say anything in these articles that’s not valuable.

Recently, they said that the Lagoa Salgada metallurgical program was a strong success.

“with respect to Lagoa Salgada in Portugal, we're just coming to the end of our very successful metallurgical test program. So, that's been a very strong success.” 29.5.2025 earnings call

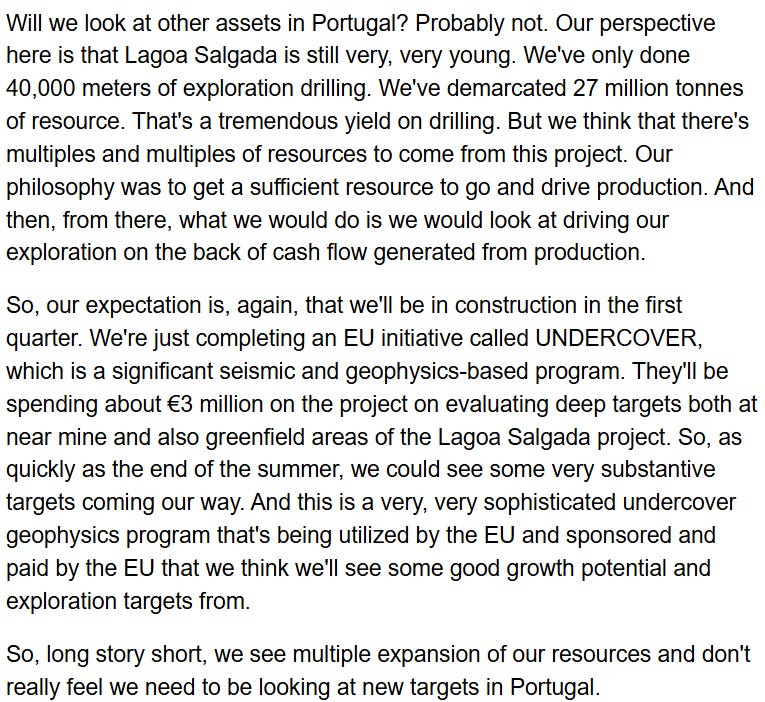

What’s good about Lagoa Salbarbaba is that there is a lot of potential for resource expansion. Here is the CEO answering a question about whether they are looking at other assets in Portugal. I’m happy that he said “probably not”, but I’m unhappy about the “probably”.

Source: Seeking Alpha Premium, Cerrado Gold Q1 earnings call transcript

Lagoa Salgada adds a group of risks to the Cerrado thesis, while offering some upside. Even significant upside if they can significantly increase the resource while getting all the permits.

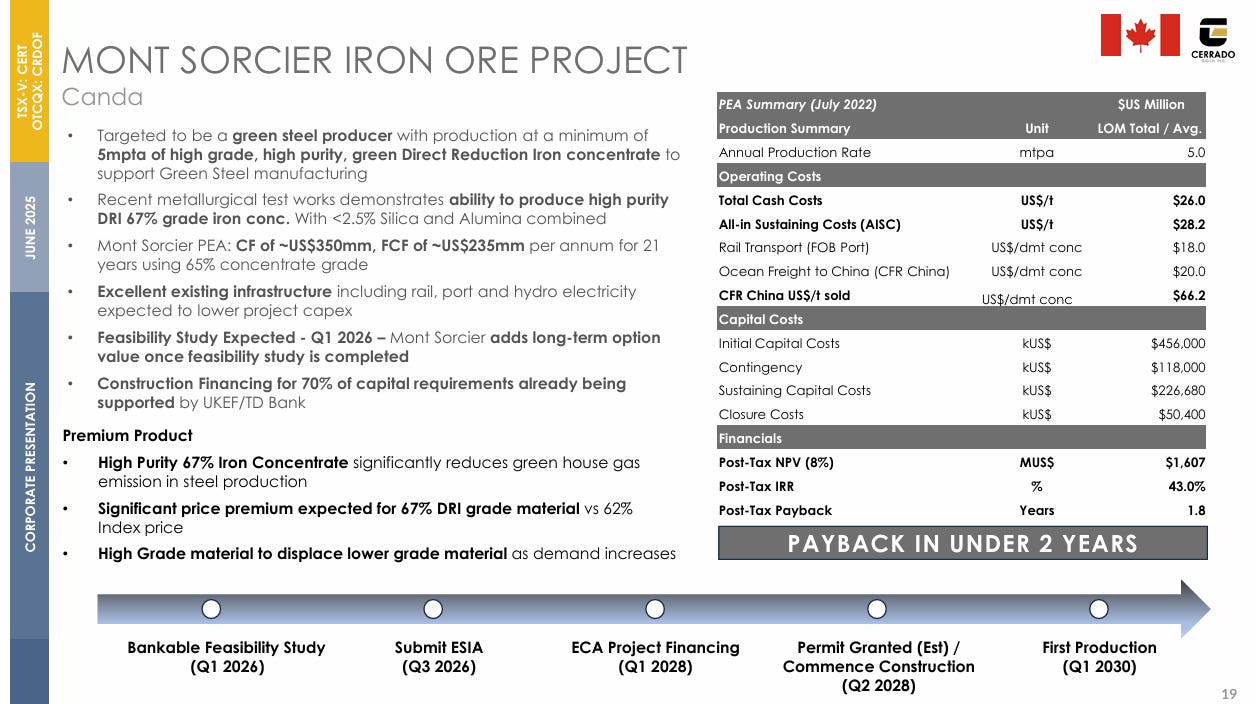

Mont Sorcier 100% ownership

This was the only asset I knew about when I first looked at Cerrado, and it was the initial draw. I knew about it through Globex Mining, which I recently sold for +77%, partly because I needed cash to buy Cerrado. Globex had a 1% royalty on Mont Sorcier, which was their most promising royalty.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

The great country of “Canda”. C-A-N-A-D-A. 2nd time I have to correct these amateurs in this article. Such disrespect to the 9th largest economy of the world and to the 0,4% ethnic Finnish population who are the main driver of Canada’s economy.

Despite its massive size, great jurisdiction, and favorable economics, the problem is it doesn’t have any momentum right now. First production in 2030. That’s forever. I hope they would sell it even at a massive discount to NPV, because it’s not priced in at all, and the stock would go up. Imagine if they could sell it at 100m USD. The stock would go up. I don’t care about their Empire building. Unless they sell, get a major as a partner it or do a Globex-style option deal, this asset won’t have a huge effect on the stock within my time frame of 6-18 months for a rerating based on developments in Argentina.

The current official plan is to use MDN cash flows to build Lagoa Salgada and LS, and MDN cash flows + their lender support to build Mont Sorcier. The big one.

“we have very very strong support uh for the the funding of this project um just like with our our Portuguese project uh we have UKF the UK export credit agency uh who are who are looking to support this project to provide us up to 70% of the the capital requirement uh for the project um and we feel very comfortable that uh streams and and Andor royalty um and and offtakes will go a long way to requiring very limited Equity to build this project and and The Limited Equity that that will be required we're very hopeful that we can use the cash flows from Portugal uh to to develop this project ” Cerrado 3.4.2025 webcast

Cerrado says this in their corporate presentation: “UK Export Credit Agency and TD Bank have been Mandated as Lead Arranged for Non- Resource Project Financing for up to 70% of Upfront Capital Requirements”

The financing that they are talking about with Lagoa Salgada and Mont Sorcier is a letter of interest and not legally binding. It was originally for Mont Sorcier and their Brazil project they sold.

. Source: https://cerradogold.com/news-media/news-2023/cerrado-gold-announces-potential-uk-export-credit-agency-support-for-project-finance-at-its-monte-do-carmo-and-mont-sorcier-projects

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

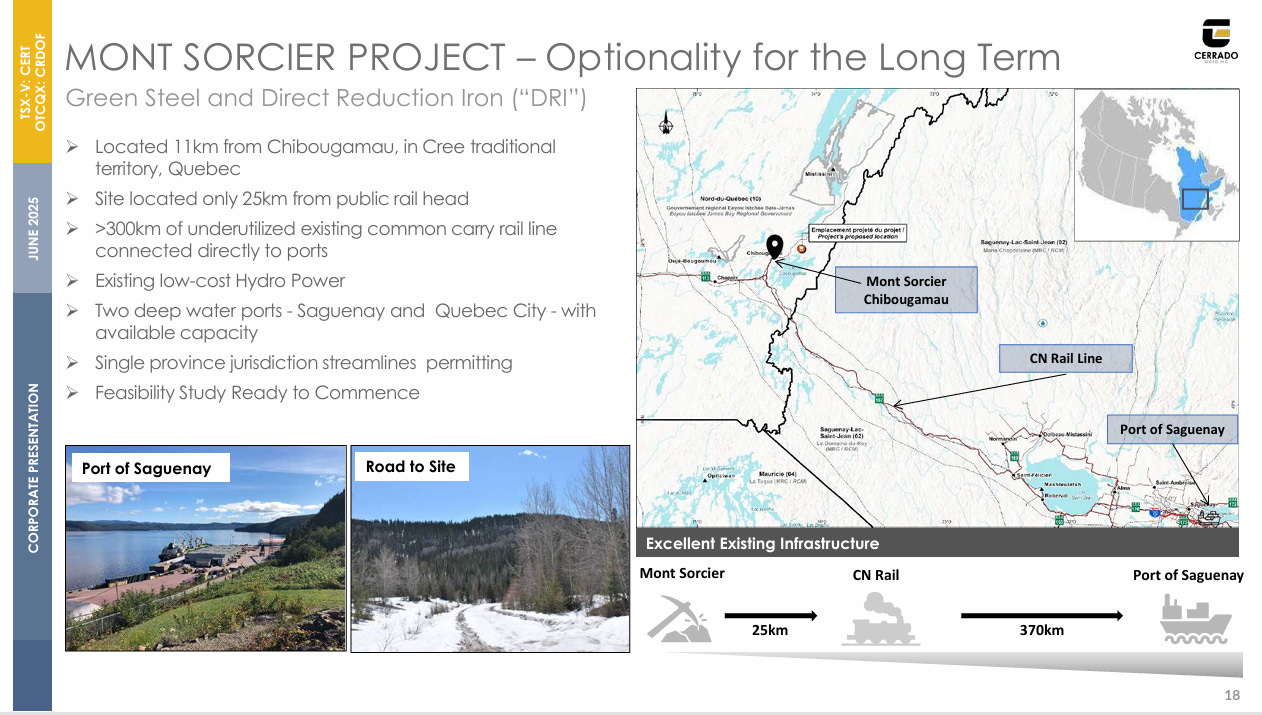

The jurisdiction is good. Workforce, infrastructure and not much politically friendly. Here are more details from the CEO:

“We're in a very very good jurisdiction from the perspective of infrastructure. Shamu has a town of about 7,500. The community, basically, they're a mining community historically. A lot of their population have to leave Shamu on a fly-in fly-out basis to other mining camps in Canada, and what we anticipate is that, you know, once we can start getting the Mour project moving, a lot of these people would much prefer to be at home, going home to their parents, their families, in the evenings. So, from that perspective, you know, we're about 380 kilometers away from a deep sea port that's with a common carrier rail line, the CN rail line, which means we have to get access to it under government pricing. The reality is that it's running today at about 30% capacity. The deep water port of Sagon basically doesn't have a customer yet. We've signed a letter of intent with the port of Sagen for our material, and there's plenty of capacity for them to take our material. Port Sagon is a federal and Quebec funded project; they've put in about $200 million. It's a deep water port and can take very very large ships for all our requirements that we require. So, from that perspective, we're in a really strong, very positive jurisdiction in all manners as it relates to mining friendliness and wanting to see this project move forward.” Cerrado 3.4.2025 webcast

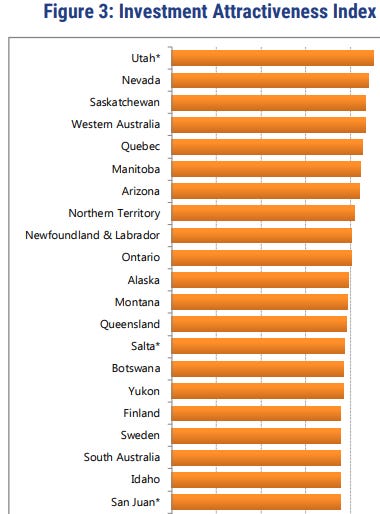

Source: https://www.fraserinstitute.org/sites/default/files/2023-annual-survey-of-mining-companies.pdf

In Fraser Institutes annual survey of mining companies in 2023 (2024 is not out yet) Quebec ranked as 5th in the Investment Attractiveness index globally.

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

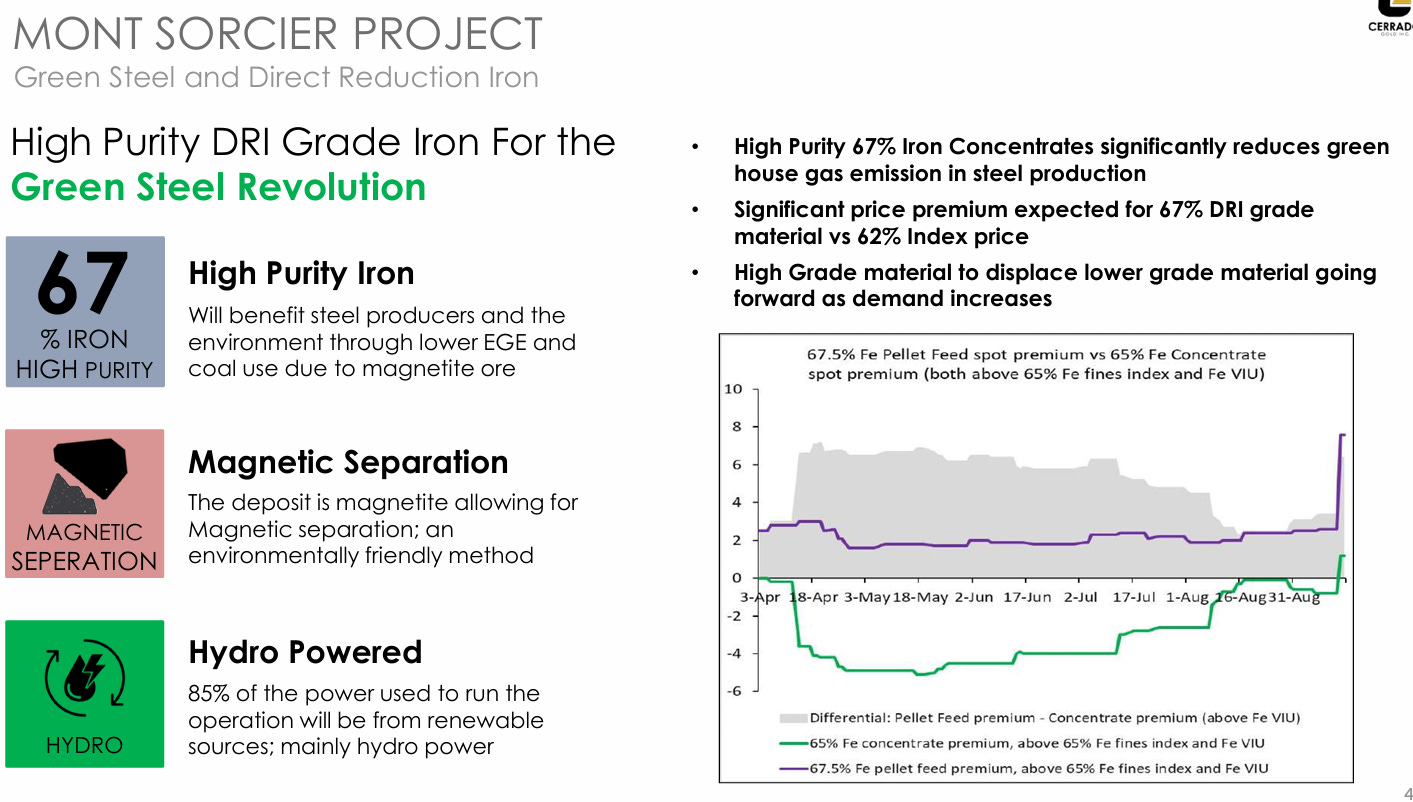

Cerrado is highlighting the 67% Iron which get a premium to lower grades. We have some upside for the NPV and the EBITDA numbers once they get the new feasibility study done in Q1 2026 because the current PEA assumes a 65% iron product “PEA Does Not factor in DRI Grade product Premium now anticipated” Corporate presentation.

Source: https://ceo.ca/@GlobeNewswire/mont-sorcier-iron-vanadium-update

It will be interesting to see what the NPV will be assuming 67% product.

There is also some expansion potential.

Source: Corporate presentation February 2025

“current mine plan only is looking at the North Zone um we have a Total Resource Global resource of 1.1 billion tons um we're using about 300 million tons for the uh for for the for the uh mine plan for 21 years um and from that perspective um we expect to see um you know we expect to see expansion coming very early after our initial production in 2030 so lots of growth in terms of uh operational growth” Cerrado 3.4.2025 webcast

Source:https://www.cerradogold.com/images/pdf/Presentations/2025/Consolidated_Cerrado_Gold_Corporate_Presentation_-_June_2025_-_Print_Version_compressed.pdf

Everything about Mont Sorcier tells me that Cerrado should just find a way to simply do something with it that makes the stock go up, because they could if they gave up the idea of developing it themselves. Sell, partner, option, etc. Otherwise, it will remain a valuable asset that will not get a proper value within the market valuation of Cerrado until years from now, when it starts nearing production.

Summary

“With stocks like Cerrado, my goal is a +50- 200% return and to take profits in 6-18 months and rotate to something else.” AlmostMongolian

I said that earlier in this article, but that was for stocks LIKE Cerrado for Cerrado specifically I’m looking for a 100-300% gain from this one, and my time frame is 6-18 months, which can always end up being shorter or longer based on the situation. Like I said earlier, with commodity stocks, I’m not looking for long-term investments. Carrado has 10x potential, but that’s not my thesis. I think that’s unlikely within my time frame.

The key variables that are going to provide upside or downside are MDN operational performance, gold price, and Portugal moving forward. Mont Sorcier remains a valuable high-potential asset, but it doesn’t have any motion right now. I honestly hope they would sell it even at a massive discount to NPV, because it’s not priced in at all, and the stock would go up. Imagine if they could sell it at 100m USD. The stock would go up. I don’t care about the Empire building. Unless they sell, get a major as a partner it or do a Globex-style option deal, it won’t have a huge effect on the stock within my time frame.

Current market cap is 71,77m USD and I’m looking to sell at 140-280m USD market cap.

Investing is all about probabilities. Any investment can lose or make money, but I like Cerrado because I think most scenarios and most likely possible future outcomes are bullish.

Here are some scenarios:

Bearish scenario: Gold price falls to 2100$, and they can’t deliver on production, LOM increase, Portugal=Market cap falls to 10-30m USD. Still, maybe profitable, Mont Sorcier, money coming in from asset sales, debt not current, cushions the blow

Slightly bullish scenarios = gold price falls to 2100$, but the company delivers on production, LOM, and Portugal. 25m USD FCF still, LOM problem fixed, record production, hard to see the stock not going up despite the gold price, as the high gold price or the production increase are not priced in at the current valuation. 70-140m USD market cap.

Slightly bullish scenario = Gold price stays above 3000$, but they get to only 45k GEO in 2025, LOM increase not as much as expected, Portugal moves forward, but with budget inflation, bad drill results. Some problems, but the market is not pricing above 3k gold, the market is pricing in production issues, and the market is not pricing the LOM increase Cerrado expects. I think the stock would still go up in this scenario. 70-140m USD market cap.

Bullish scenario = Gold above 3k, Production guidance achieved, LOM increase from 20k metres drilling program within the range the company projected 300- 700k, UG ramp up successful, Portugal moves forward as planned. This is the scenario where everything goes according to plan, and gold doesn’t fall much. 200-400m USD market cap.

Wildly bullish scenario=Gold price goes to above 4000$, they get to above 100k GEO production, Portugal moves forward as planned with resource expansion and successful drilling, Mont Sorcier gets monetized. 500-1500m USD market cap.

I didn’t put a neutral scenario, because that’s the scenario where some things go according to plan and some won’t or the gold price won’t co-operate and that is because I think most scenarios like that will end up as bullish, because the stock is so cheap and the stock is not pricing in so many positive catalysts.

And that is my base thesis. Most futures I see, I make money on Cerrado.