Pancontinental Energy: Asymmetric Situation

PEL 87(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian short AD: THE LINK

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

This is a paywalled write-up. I also released a FREE Sintana Energy update today. These were originally the same article, because these companies are connected through PEL 87, but it was too long, so I ripped them apart.

I didn’t like Pancontinental before. I didn’t see a reason to buy even a small position instead of adding to Sintana, but now, after Pancontinental stock crashed due to Woodside leaving PEL 87, and also Woodside leaving PEL 87 left Pancontinental in an asymmetric situation, I think it’s worth a shot at the current price and the current situation. Pancontinental has been added to The AlmostMongolian Portfolio. I think it’s a great risk/reward now when it wasn’t before.

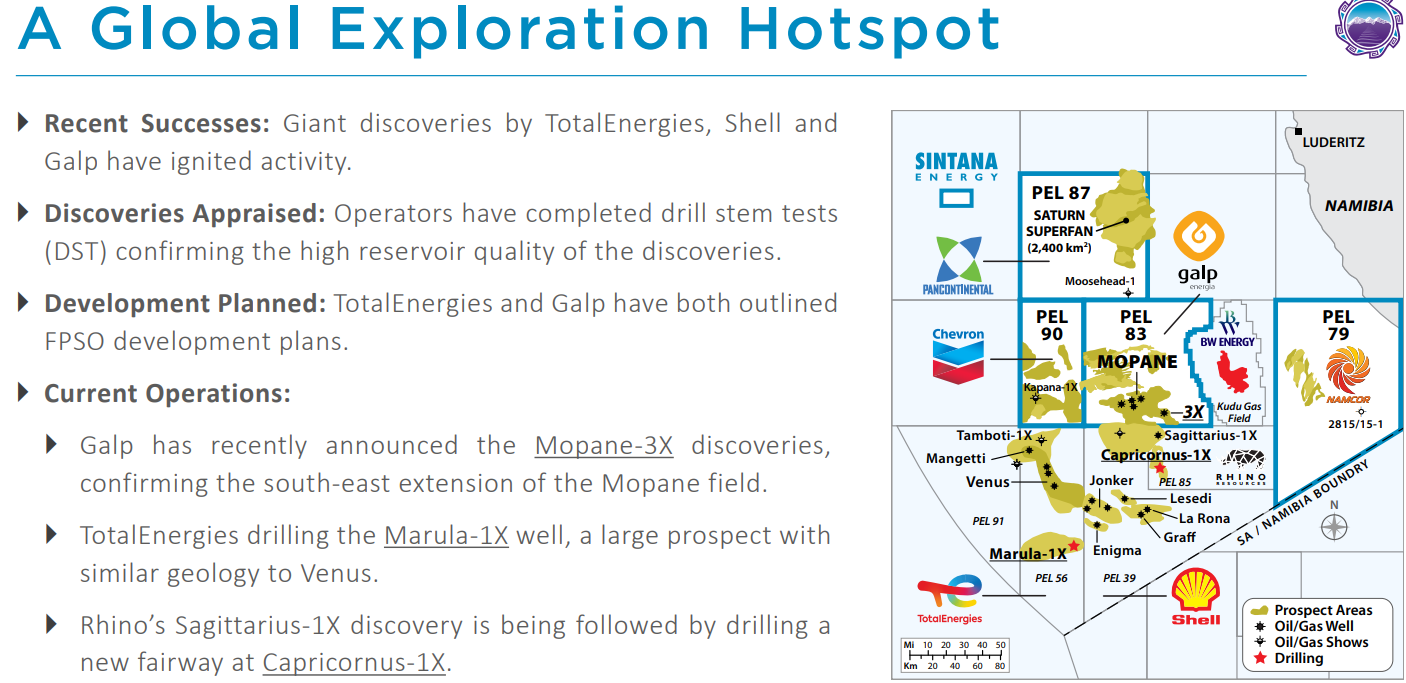

Pancontinental Energy $PCL.AX Investment Thesis

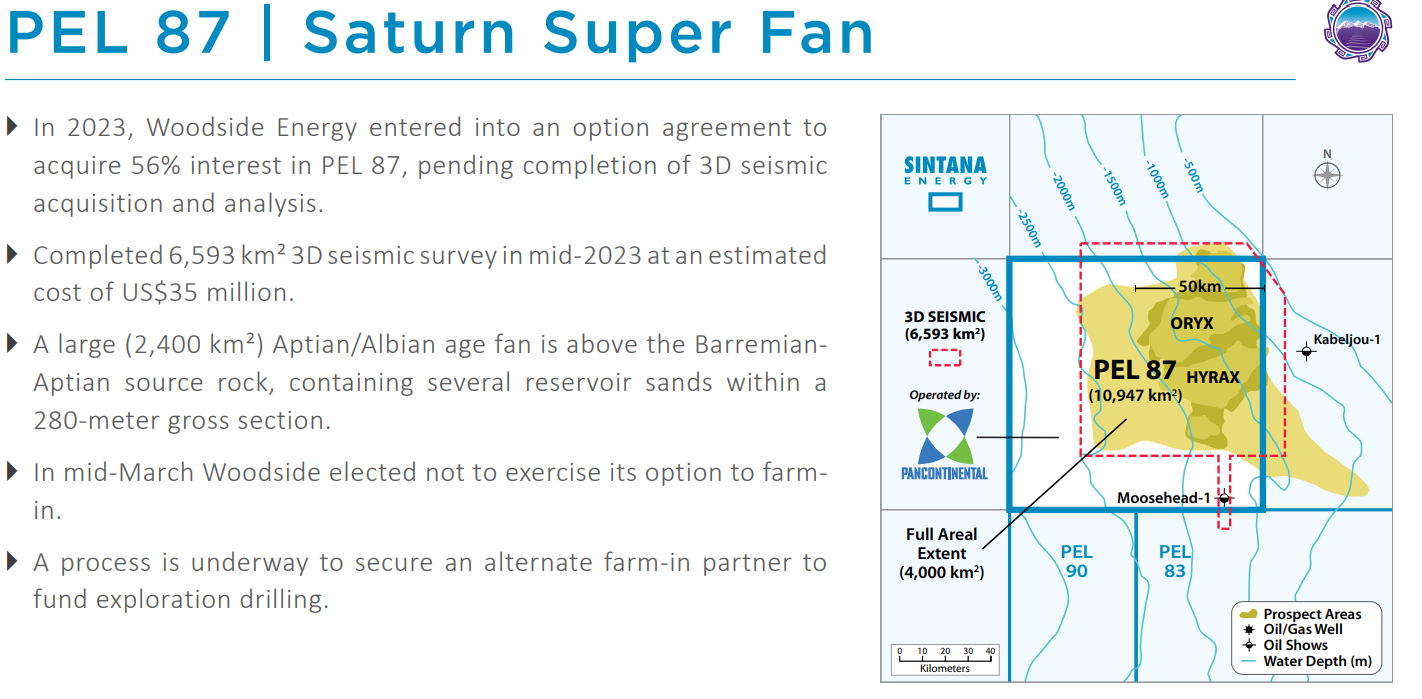

I have already covered the only asset of Pancontinental in the Sintana article, so I’m not doing it again. It is PEL 87. THE SATURN SUPERFAN. To quickly recap, it’s this.

Source: https://sintanaenergy.com/wp-content/uploads/2025/03/sei_corp_presentation_mar25.pdf

Sintana has a 7.35% working interest in PEL 87. Pancontinental is the operator of PEL 87 and has a 75% working interest.

To explain why I like Pancontinental stock now, I will explain why I didn’t like it before Woodside left PEL 87.

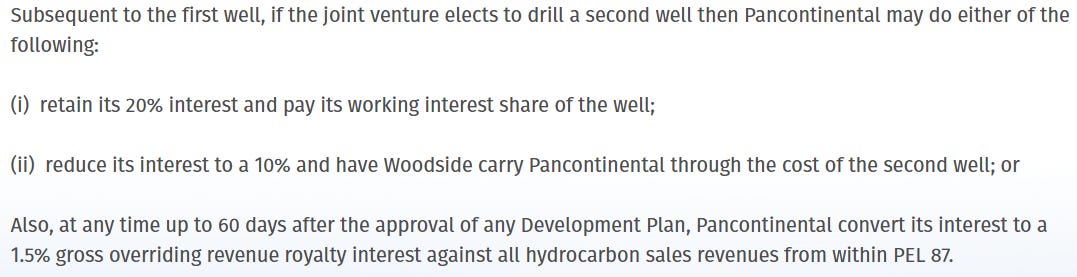

This was the situation then: Wooside was going to get 56% of PEL 87 after committing to drilling the one well. This would have left Pancontinental with 19%, and they had the option to obtain an additional 1% from Custos for 1 million USD. That would have left Pancontinental with 20% working interest.

Source: https://wcsecure.weblink.com.au/pdf/PCL/02924585.pdf

Just from that, the deal looks pretty sweet for Woodside, but a part of the deal was that they have to pay for a 3D seismic over the whole block that costs 35m USD. The drilling of the exploration well costs somewhere around $ 70 million USD. Essentially, Woodside was going to acquire 56% of PEL 87 for $ 105 million USD worth of work.

After drilling this well, Woodside was not going to solely fund the following wells. After that, Woodside would have paid for their share, but Pancontinental would have had to pay for their share 20%, and for Custos’ share 14%(Sintana owns 49% of Custos), and for NAMCOR’s share of 10%. Pancontinental has a separate agreement with the JV that includes Custos and Namcor, which Pancontinental has to carry these parties to “essentially to FID,” according to Sintana’s IR.

So Pancontinental has 3.6M USD in cash based on the latest financials. They would have had to raise money to pay for these drilling expenses, or they would have had to give up another 10% working interest for Woodside to pay for the expenses of the second well.

Source: https://pancon.com.au/orange-basin-pel-87/woodside-partnership/

What would have been the final working interest of Pancontinental after many wells? Likely way under 10% or to keep 20%, the stock would have been massively diluted. Seems like the best option would be to get the 1.5% royalty eventually, and if the block goes into production, it can be a decent yearly income.

Let’s say 150k barrels per day at 70$ Brent, that would have been 57,487,500 USD royalty revenue per year somewhere in the 2030s.

And what was the market cap when this was the situation? Hovering at the 80-100m USD level. You can see why I was not interested in this stock.

At the time, Sintana's market cap was 195 million USD, and Sintana stock was/is cheap only to PEL 83 and has 7.35% of PEL 87, which is carried further than Pancontinental.

Why even risk it with Pancontinental at that point? I thought. I’ll just get more Sintana to get the PEL 87 exposure for free. Pancontinental had more risk, but not significantly more effective exposure to PEL 87 and certainly not more overall reward potential.

Now the situation is different for Pancontinental, and while I’m not making it a big position like Sintana. The risk/reward is good enough for a small position.

The first reason is that the valuation is much lower.

Source: Yahoo Finance

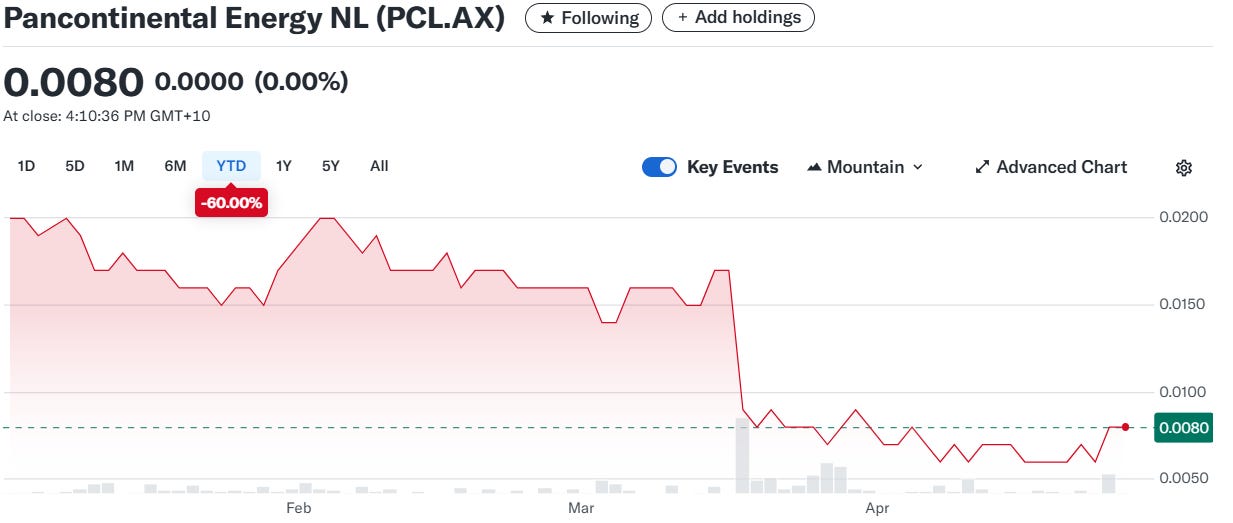

The current market cap is 41 million USD.

41 million USD for 75% of PEL 87.

Source: https://wcsecure.weblink.com.au/pdf/PCL/02926130.pdf

Woodside's leaving has also removed the dilution risk for a decent amount of time.

They had 3.6m AUD at the end of last year and no debt. Pancontinental burns about 1.5-2 million USD per year. They have money for about 2 years before they have to raise money for the normal running costs of the business.

Now, the situation is that while drilling is not happening as soon, and we don’t know when, they are not in a situation where they either have to eventually dilute shareholders heavily or give up a massive amount of working interest.

They are able to take offers and have companies compete to make the best offer while they have 75% WI and 35m USD 3D seismic done, and a prospective resource estimate done.

This is a much better negotiation situation than when they signed the Woodside agreement. Hence, I think they will get a better deal, mostly because of the Woodside agreement that had Woodside pay for so many costs to advance the block that now only benefit Pancontinental.

The 3D seismic was 35m USD, and Pancontinental's share is 75%, so 35*0,75=26,25m USD. Woodside spent 26,25m USD on behalf of Pancontinental.

Whether the investment Woodside made was wasted or not, we don’t know, but Woodside seems to think so; but one oil company’s trash is another oil company’s treasure. As proven by Valeura Energy.

The question arises, why did Woodside leave PEL 87?

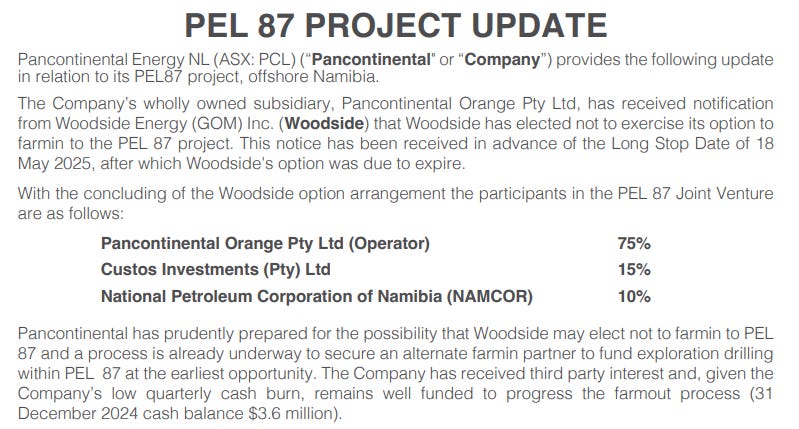

Is it because they analyzed the data and said, “We looked at the data. It doesn’t look good. We are not spending another dime here,” or has Woodside's focus shifted to other areas, and deepwater exploration in Africa doesn’t fit their new objectives as a company?

Of course, Sintana and Pancontinental shareholders wish that it’s the 2nd reason and look for reasons to believe that, and I think the 2nd reason is more likely, but it’s still good to be aware of the bias.

“With significant growth in the pipeline, we continue to streamline our business to focus on core and highvalue assets. Our agreement to divest the Greater Angostura assets in Trinidad and Tobago for $206 million underscores our disciplined approach to portfolio management and optimisation. We applied the same discipline in declining to progress Namibian Petroleum Exploration Licence 87, exiting H2TAS and reassessing the H2OK project.”

It’s difficult to say because let’s say it’s the 1st reason. Would they come out and say it? There is no upside for them to do that, so no. How would we know? We can’t know unless there is a leak, and we couldn’t even know if it was reliable.

So we have to admit it could be the first reason, but we won’t know it. Is it the beloved 2nd reason? There are reasonable reasons to reasonably believe this is the more likely reason. Reason.

Here is what Woodside said in their Q1 report.

“With significant growth in the pipeline, we continue to streamline our business to focus on core and highvalue assets. Our agreement to divest the Greater Angostura assets in Trinidad and Tobago for $206 million underscores our disciplined approach to portfolio management and optimisation. We applied the same discipline in declining to progress Namibian Petroleum Exploration Licence 87, exiting H2TAS and reassessing the H2OK project.”

From this, we can interpret that PEL 87 was not their core asset (I don’t mind hearing) or it wasn’t a high-value asset (I hate to hear that). The Trinidad and Tobago asset they divested was an offshore oil asset like PEL 87, which points to a direction that they are focusing away from these types of assets.

@TommyDeepwater on X made a great post deep-diving into this subject and some other Orange Basin stuff as well. I encourage you to read it fully below.

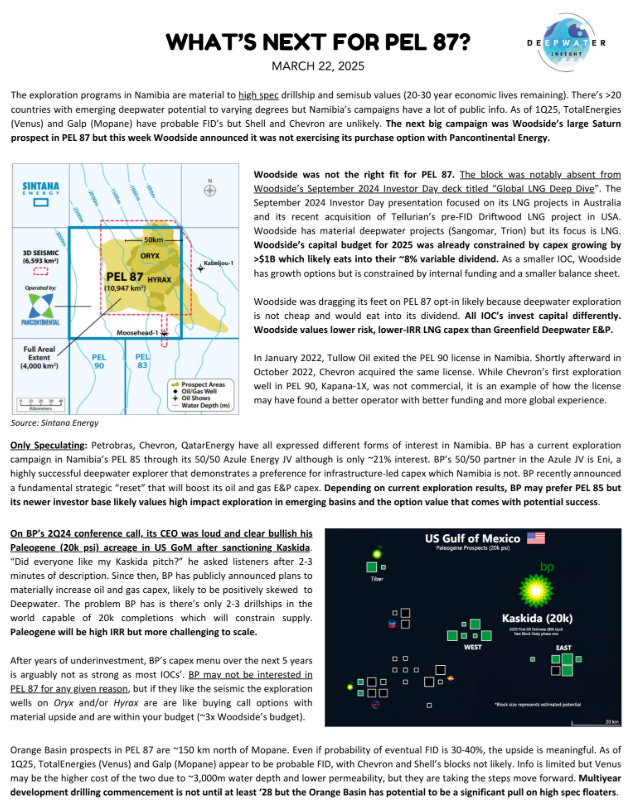

Source: https://x.com/TommyDeepwater/status/1903413823362806100/photo/1

In short, Woodside is focused on large LNG projects. Developing these projects while keeping their high dividend would be difficult while developing PEL 87 as well. So PEl 87 had to go.

I think this is a good argument, and I did some research myself as well that corroborated it.

Source: https://www.woodside.com/

First thing, when you scroll through the first page, it’s all about climate, LNG, and energy transition.

They are also investing in things like Ammonia.

Source: https://www.woodside.com/docs/default-source/investors/climate-related-investor-engagement-updated-march-2025.pdf

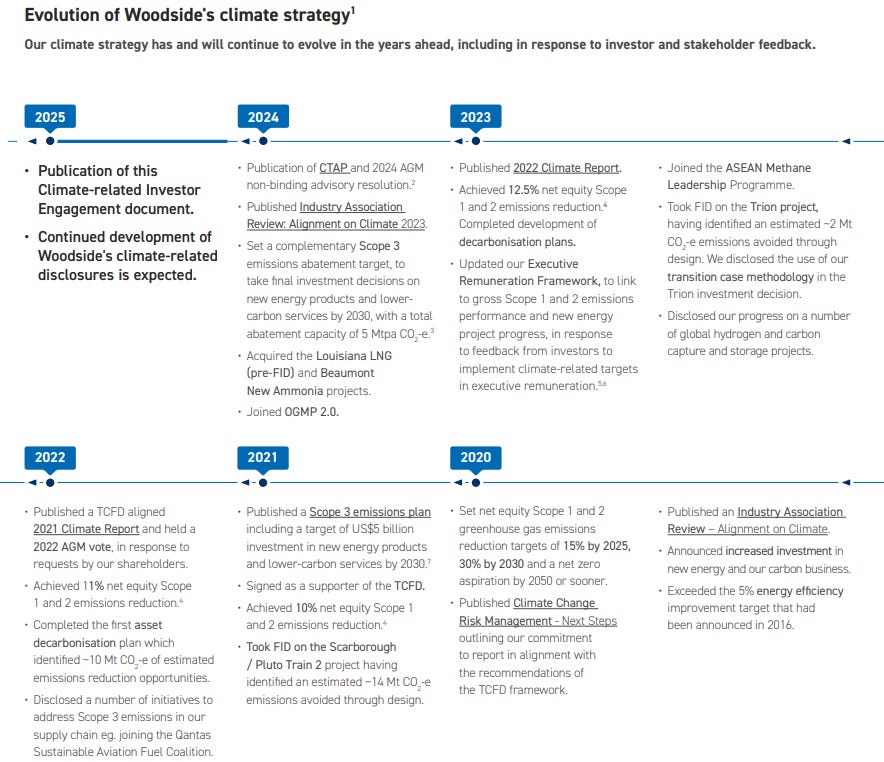

This is from their new Climate-related investor engagement document.

There has also been an activist battle among Woodside shareholders to have a more robust climate strategy.

Source: https://www.netzeroinvestor.net/news-and-views/shareholders-reject-woodside-energys-transition-strategy

These are not Fintwit shareholders; they didn’t reject Woodside’s plan because it was too green. They rejected it because it wasn’t green enough.

Source: https://www.netzeroinvestor.net/news-and-views/briefs/shareholders-push-for-vote-against-woodside-directors

There has been serious pushback against this company for not being green enough, so it isn’t crazy to say this was likely one of the reasons that Woodside left PEL 87.

If we look at their growth projects, we do see one oil project in there, but this oil project has been in development for a long time and is going into production already in 2028. Unlike PEL 87, which would have taken until the 2030s.

• The Beaumont New Ammonia Project was 90%

complete, with Phase 1 of the project on track for

startup in the second half of 2025.

• The Scarborough Energy Project was 82%

complete, and remains on track for first LNG cargo

in the second half of 2026.

• The Trion Project was 26% complete, and remains

on track for first oil in 2028.” Woodside Q1 results

At the same time they are telling how they are reducing emissions for their only oil project in their climate report “Took FID on the Trion project, having identified an estimated ~2 Mt CO2 -e emissions avoided through design. We disclosed the use of our transition case methodology in the Trion investment decision.”

After their shareholders have already told them they are not green enough, there is likely no room for another oil growth project, while they are also streamlining their portfolio with sales of other assets like the Trinidad oil field and 40% of the Louisiana LNG.

I think the massive cope argument is correct, and it’s more likely that Woodside left PEL 87, not because they looked at the data and concluded it’s a bad prospect for commercial oil, but due to shifting priorities within the company regarding energy transition and capital allocation.

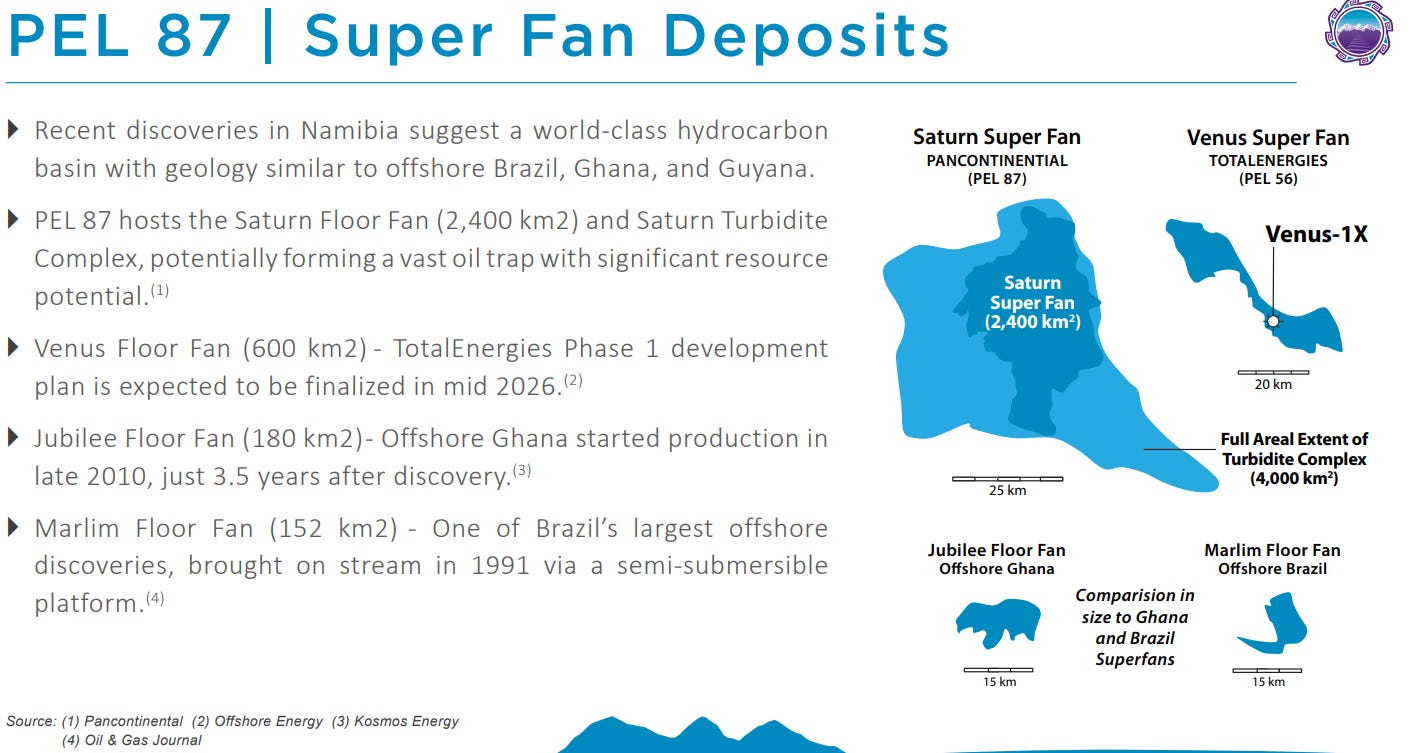

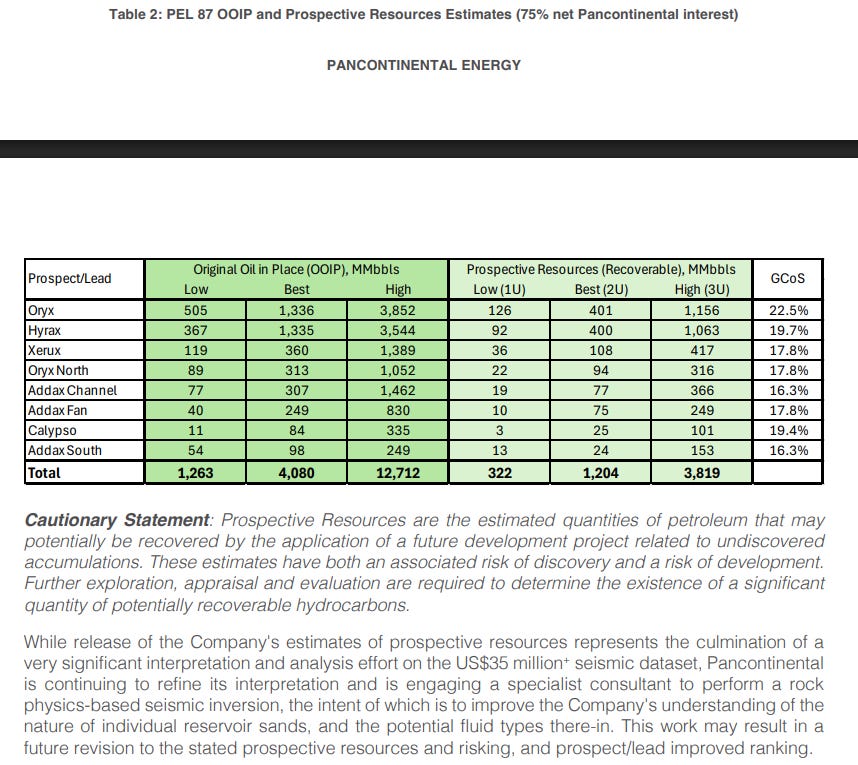

Prospective Resource Estimate

Pancontinental released the prospective resource estimate on the same day as Woodside's leaving announcement, which is likely to soften the blow on the share price.

The stock was down massively anyway, but I know that the market liked the prospective resource estimate announcement because of the way these two announcements were timed. Woodside's announcement came when the NA markets were open, and Sintana's stock reacted badly to it. Then the Prospective resource announcement came when the Australian market was open, but the NA closed, because the Australian market reacted to both at the same time, Woodside's announcement overshadowed the prospective resource, so Pancontinental's stock went down anyway. Now the next day, Sintana had already reacted to Woodside, but had not yet reacted to Prospective resource, and Sintana's stock went up the next day when Prospective resource was the only news for Sintana.

So that’s how I know this was good news, even according to the so-called “market”.

Here it is.

Source: https://wcsecure.weblink.com.au/pdf/PCL/02926131.pdf

There is quite a big range here. These are numbers for 75% of the block net to Pancontinental. Low means 90% confidence, Best is 50% confidence, and high is 10% confidence. There is also no associated gas with these estimates. Only oil.

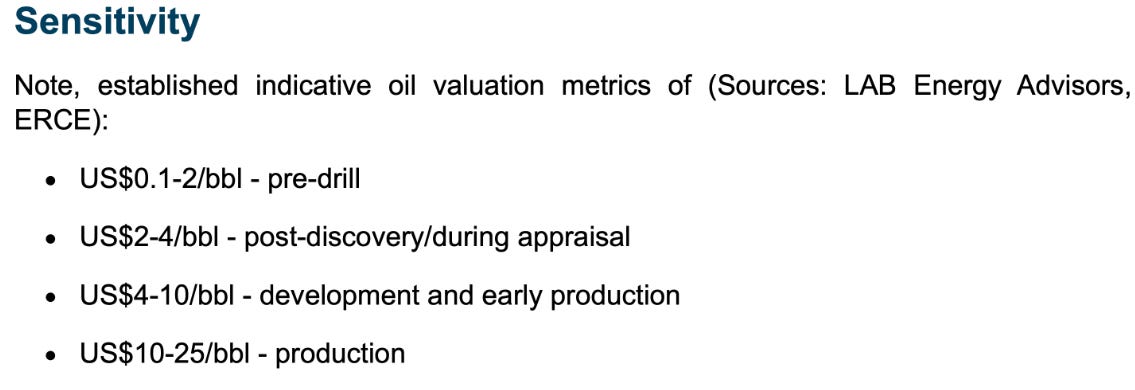

How would you value a prospective resource? According to this website, you can use 0,1-2$ per barrel.

Source: Lab Energy Advisors, ERCE

You can spin the numbers around. The lowest number I can come up with would be using the lowest recoverable estimate of 322 million barrels and 10 cents per barrel, and that would be 32,2 million USD. The highest estimate using a recoverable high estimate of 3,8 billion barrels and using 2$ per barrel would be 7.6 billion USD. Then you could triple that if you use original oil in place, but as you can see, this is quite arbitrary. But almost every calculation you make with these metrics, you get a number that’s way higher than the current market cap.

Another way you could try to value this block based on prospective resource is to use another block in the Orange Basin that is in the same stage of development, and that would be the beloved 3B/4B. It’s also ready to drill and has a prospective resource estimate. 3B/4B also has a real valuation from the private market. Not based on analysis, but based on a real transaction.

So let’s take 75% of the P50 prospective resource from both. Using only oil estimates, as PEL 87 doesn’t have associated gas estimates.

3B/4B=2 291 250 000 barrels

PEL87=1 204 000 000 barrels

3B/4B has about 90% more.

This is how 3B/4B is valued, and note that 3B/4B is in the South African side of the Orange Basin, and it is a worse and more unstable jurisdiction than Namibia.

It's valued at a much higher level than Pancontinental. This is from my Eco Atlantic article

Again, we see private market valuations wildly different from public market valuations for Orange Basin blocks. The 428m valuation for 3B/4B is the best one as it's relatively recent and the transaction had multiple big players involved. Africa Oil, Qatar Energy, and Total Energy were part of this transaction and agreed to this valuation.

Pancontinental is 25 million USD

3B/4B is 428 million USD has 90% more oil, but has 17 times higher valuation

Are Total and Qatar Energies wrong, or are the retail shareholders who make up the Pancontinental valuation wrong?

I guess we’ll see over time.

Farmout

All of the blocks that are advanced in the Orange Basin have a Major company as an operator. Expect PEL 87.

Pancontinental Director Barry Rushworth commented "These results verify the Saturn Complex as a highly attractive exploration play, particularly given the significant size of the targets and major discoveries that continue to be made to our south within a comparable geological setting. The PEL 87 Joint Venture is well placed and in a prominent position within the Namibian Orange Basin, with an extremely valuable, high quality and extensive 3D seismic dataset. PEL 87 is the only permit not held by a major oil and gas company that is adjacent and on trend to the giant Mopane discovery, which is believed to host some 10 Billion barrels of oil-in-place".

You could also say it’s the only advanced block in the Orange Basin not held by a major oil company. Block that has the amount of work done as PEL 87 and has a prospective resource estimate.

Source: https://sintanaenergy.com/wp-content/uploads/2025/03/sei_corp_presentation_mar25.pdf

PEL 85 is also. Rhino’s partner, Azule Energy is a 50/50 JV between PB and ENI. PEL 87 is the only one available.

What are the odds that they can’t find a farmout partner? I would say very low. It has to be the most exciting undrilled block in the hottest exploration area in the world.

It could take 1-18 months. Hard to say how tough Pancontinental will negotiate and how competitive it’s going to be. I’m sure they are getting constant pressure from investors to do it as soon as possible, because investors know that when it happens, the stock will go up even if it’s not the best deal they could get, and in the stock market, there is always opportunity cost with waiting for an event to happen.

If we have to wait for years, it will be a big opportunity cost to hold Pancontinental when other companies could be doing all sorts of value-adding activities during that time, but I don’t think it’s likely.

Summary

-Woodside most likely left PEL 87 due to changes in the company’s strategy and focus, and not due to PEL 87 geology, based on my analysis. Although we don’t know that for 100%.

-Pancontinental is in an amazing position to negotiate a good farmout deal with a major due to Woodside doing a lot of work for them and then leaving. Hence, leaving Pancontinental as the beneficiary.

-They are the only advanced block in the Orange Basin not in the hands of a major oil company.

-They do not have to raise money for about 2 years.

When we look at the situation with the stock I think that this is pretty low risk entry. The company is an inherently high risk as it’s a single asset exploration company in Africa so that may sound grazy, but consider what are the risks for Pancontinental that could cause the stock to crash from its current range of 0,006-0,009? What could happen to cause the stock to go to 0,003 AUD?

Not much. There are always black swan global events or political events in Namibia that can not be overruled, but because there is not much going on with the company, the company is financially sound and the stock has already reacted to the one event that could cause the stock to crash, which was Woodside leaving. I think the biggest risk would be simply farmout negotiations taking along time and having a slow decline or staying in the current range and suffering from opportunity cost.

And then we look at the reward and the farmout probably has 2-3x upside potential based on the fact that it should be a much better deal and possibly a deal that will carry Pancontinental all the way to production. Let’s say they get 15% carried to production and have their obligations towards Custos and NAMCOR taken care of. That doesn’t sound unlikely and would be massivelly bullish outcome.

Of course, after the farmout, the drilling presents a new set of risks, but I think the stock has a lot of upside based on the asymmetric catalyst of the farmout itself, which is why I like the current risk/reward. The stock will be way higher when they get to drilling.

Regardless, this is still the smallest position in the AlmostMongolian portfolio, primarily due to opportunity cost. I believe the stock will remain within the current range for the next few months, and I doubt the farmout will occur soon. Likely late this year, at the earliest. But they can always surprise. I’m looking to gradually increase this position at the lower end of the range 0,006-0,007 AUD. My current cost basis is 0,007 AUD.