PlasCred Deep dive + Comparison with Aduro

The winner is...

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian AD: THE LINK

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

There are now two pre-revenue plastic recycling plays in the AlmostMongolian Portfolio, Aduro and Plascred. This sector is a graveyard of failed projects, which makes me question my sanity a bit, but that is the situation I have found myself in.

This article provides a deep dive into PlasCred and compares PlasCred to Aduro for the purpose of ultimately and definitely determining the best investment case in the sector.

Maybe it also serves to indoctrinate PlasCred shareholders to Aduro and vice versa, and to inspire more research. I want there to be a competition between the two shareholder cults, with each finding flaws in the other's investment thesis. I sparked a small skirmish on ceo.ca after sharing my first tweet about PlasCred, but unfortunately, the fighting has since ceased. And both sides have returned to their echo chambers.

There will be a separate section “PlasCred vs Aduro” dedicated to this topic within the paywalled part of the article, but just to compare the investment cases shortly:

PlasCred is a nanocap plastic recycling company advancing toward commercialisation in 2027. Plascred entered the public markets through a reverse merger(similarly to LibertyStream) in 2023. How PlasCred's story differs from Aduro's is that Aduro is bringing to market a new, patented water-based hydrochemolytic technology(HCT) for plastic recycling, and the investment case is that this is going to be the holy grail of plastic recycling technology, which, once fully commercially validated, would be deployed globally through a licensing model. Hence, Aduro is engaging potential partners worldwide and working with large international companies, such as TotalEnergies and Georg Fischer.

Plascred has a different approach. PlasCred uses a patent-pending variant of the pyrolysis technology. Pyrolysis is the most common method for chemical plastic recycling, which uses heat to break down plastics. And instead of a licensing route, they are laser-focused on delivering on a plan in Alberta, building a commercial unit and scaling it up in stages, optimising logistics by partnering with CN Rail, taking advantage of carbon/plastic credits to increase profitability and utilising non-dilutive government grants and loans for the CAPEX.

Aduro’s market cap is 25 times larger than PlasCred’s. From a technology perspective, PlasCred doesn’t promise quite as much as Aduro, but taking into account the company’s much smaller valuation, it promises a lot.

Like Aduro, PlasCred is another story that seems almost too good to be true, the way the companies present it, because both are relatively small, early-stage companies claiming to offer profitable solutions to the massive plastic recycling problem. Which is something that larger companies have repeatedly failed to achieve.

While PlasCred doesn’t promise as much as Aduro does with its technology, what I think makes PlasCred an interesting investment case is a combination of a much lower valuation, shareholder-aligned management, and a clear plan to commercialise with limited dilution:

Some numbers

In Canadian Dollars

Source: PlasCred corporate presentation Q1 2026

Market cap: $20.5 million

Market Cap fully diluted: $27.2 million

Cash position as of September 30th: $220k

The company burns around $200-400k per quarter for normal operations. They have been financing themselves with warrants and small raises in recent months.

No debt as of now, but once they start building their commercial facility, which requires $25 million of CAPEX, they can tap into an $8.5 million debt facility and $7.35 million in grants. This leaves $9.15 million left to be raised.

Insider ownership 30% on a fully diluted basis, and the CEO owns 27,594,997 shares and 5 million performance warrants, which means he personally owns 27.5% on a fully diluted basis.

FYI, when I’m quoting the PlasCred CEO. The quotes are from this presentation from March 2024. It’s the latest in-depth interview/presentation I could find. This company has not been promotional. Sometimes they do short 3-9 minute interviews with Stockhouse or ceo.ca in connection with some new press release. But when it comes to in-depth presentations with Q&A, the 2024 interview was the best source I had to work with.

A quick detour: I came up with a new investment rule as I pondered whether to use “PlasCred’s CEO” or his first name, Troy, when referring to PlasCred’s CEO in this article. I came to the following conclusion:

Never call the CEO or any member of management by their real names, especially not by their first names. Always refer to them by their titles. When you use their real names, you are already subconsciously creating a parasocial connection to the person, which creates an emotional connection to your investment in that company, and this hurts your ability to make investment decisions as objectively as possible.

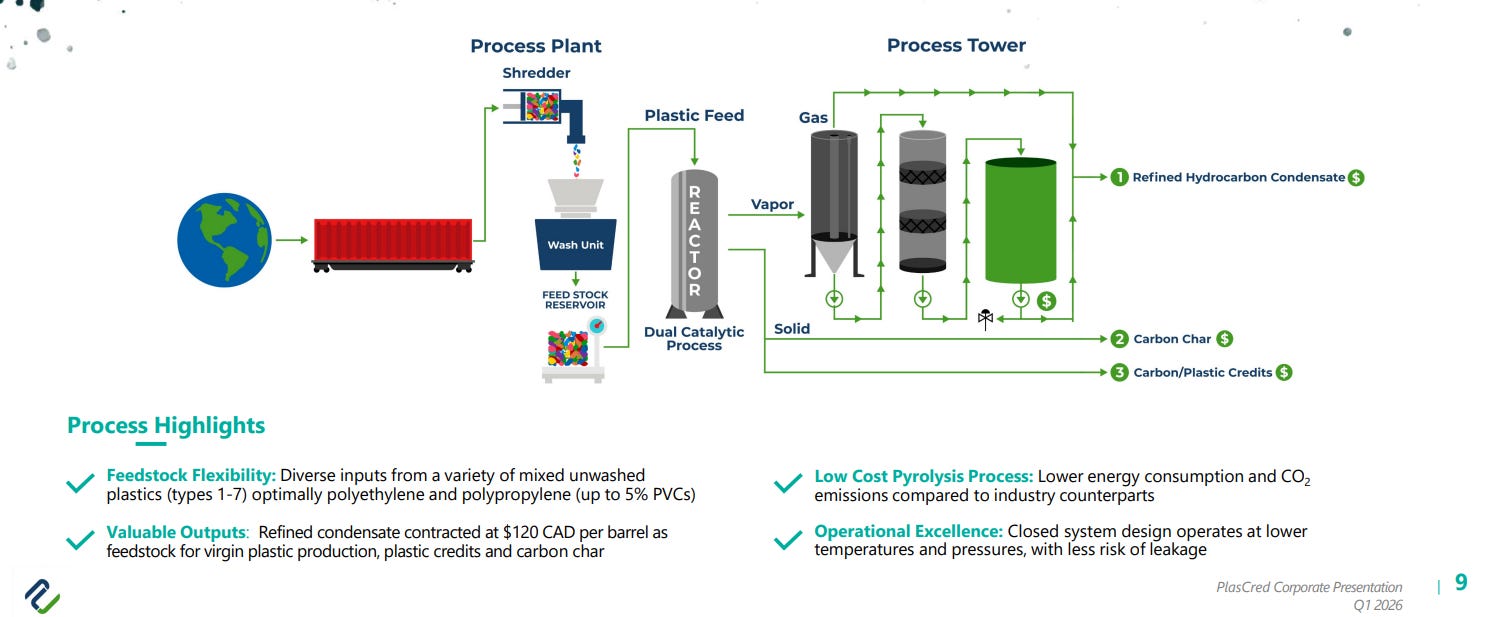

Technology

Source: PlasCred Corporate Presentation Q1 2026

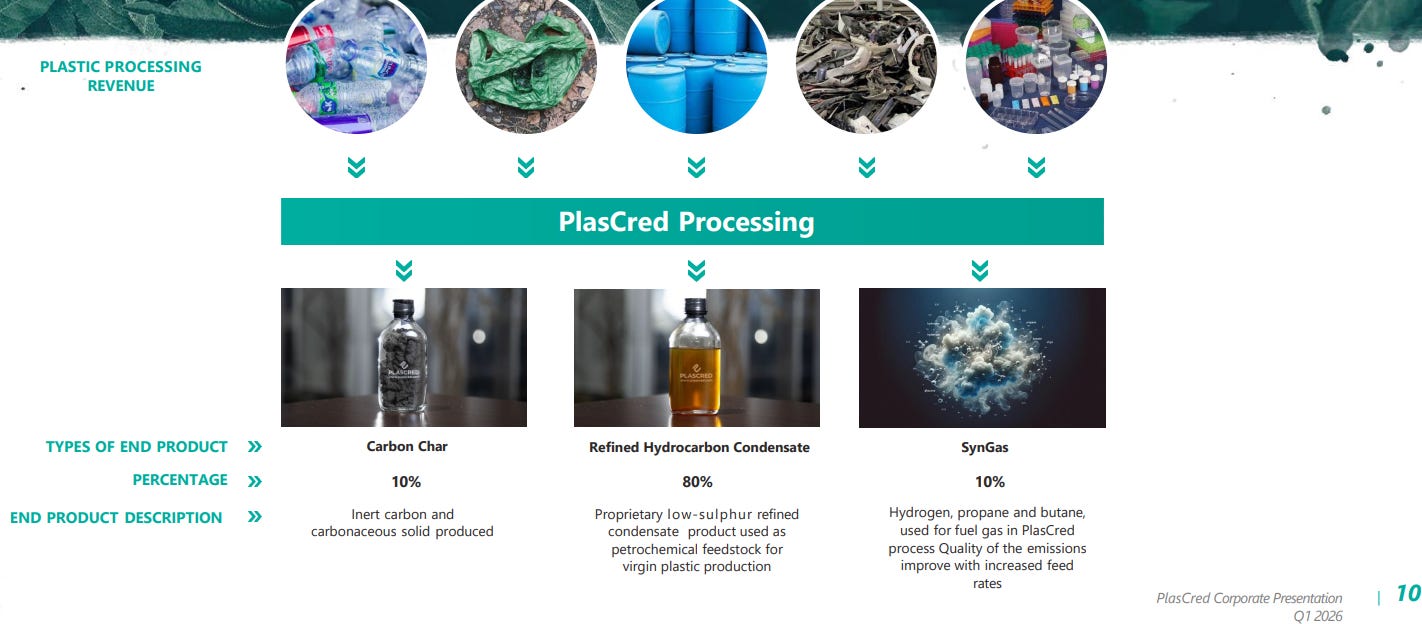

Plascred has a proprietary patent-pending process to turn unsorted, mixed plastic waste into a hydrocarbon liquid or “low-sulphur refined condensate”. The condensate has the following commercial use cases:

Petrochemical Feedstock: Drop-in replacement for virgin naphtha in plastic production

Transporation Fuel Blend Stock: It can be converted into transportation fuels, helping to minimize the drilling of new oil wells.

Pipeline Diluent: Compatible with heavy crude oil transportation requirements.

Source: PlasCred’s website

On top of the condensate, which they can sell at $120 per barrel based on their offtake agreement, they generate additional revenue from carbon char and carbon/plastic credits. Of these 3 additional income streams, plastic credits have the potential to be huge for them, which I will cover more later in the article.

Ideally, you wouldn’t want the char at all and have a higher liquid yield, but PlasCred says it can sell it to asphalt companies.

the black carbon we’re selling that to asphalt companies and the ashal companies are using it for basically pigment in their color for ashphalt there’s also a lot of other companies that are bugging us it so we do have off-take agreements coming with those as well

Source: https://oceanmaterial.com/what-plastics-can-be-recycled/

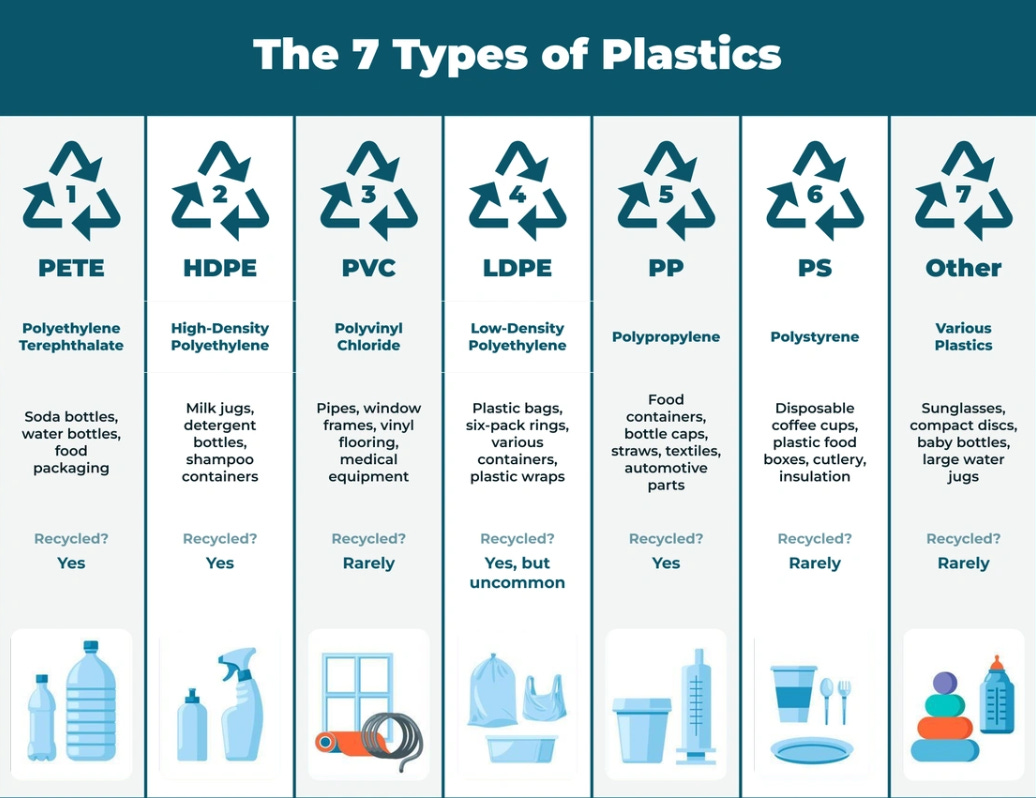

One of PlasCred’s major advantages is its ability to recycle 1-7 plastic types, and also dirty plastics. Allowing the company to take plastic waste in bulk without needing to wash and sort it. Lowering feedstock costs and increasing availability.

Feedstock Flexibility: Diverse inputs from a variety of mixed unwashed plastics (types 1-7) optimally polyethylene and polypropylene (up to 5% PVCs)

Source: PlasCred Corporate Presentation Q1 2026

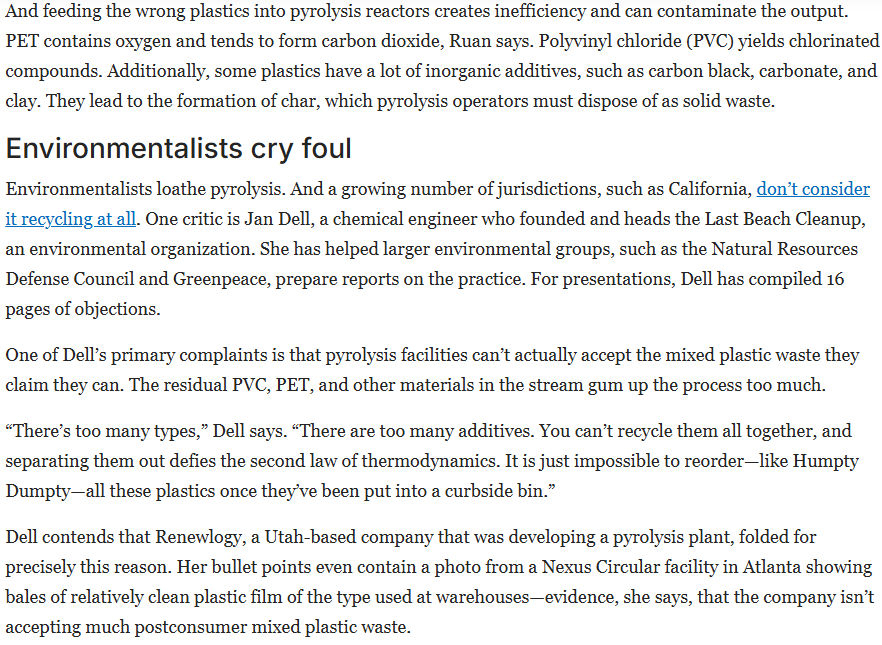

PlasCred uses its own pyrolysis variant. Pyrolysis is the most common method of chemical plastic recycling, but it has also proven to be problematic in many ways. This is one of PlasCred’s issues with its investment story. They are working with a technology with a poor/mixed track record with plastic recycling. Many investors will dismiss the company outright because of it. Here is an example of it, and I fact-checked these claims, and they’re basically true:

Source: OneOfSeven debating stoneybagpipes on ceo.ca

PlasCred has their own spin on Pyrolysis, which they claim is different, but they need to continuously prove they can produce better results than their peers; in contrast, Aduro’s HCT doesn’t carry the reputational weight of past failures, and they can brand themselves as the only ones who have the real solution, which enables more hype to build up among investors, which means easier time of raising money and most importantly stock price going up.

No article like “Chemical Recycling” Is a Toxic Trap” has been written about their tech:

Source: https://www.nrdc.org/resources/chemical-recycling

For more on past Pyrolysis failures and other players in the sector, you can take a look at these videos by Amateur Investing: Agilyx failure and 30 Plastics Recycling Companies Compared

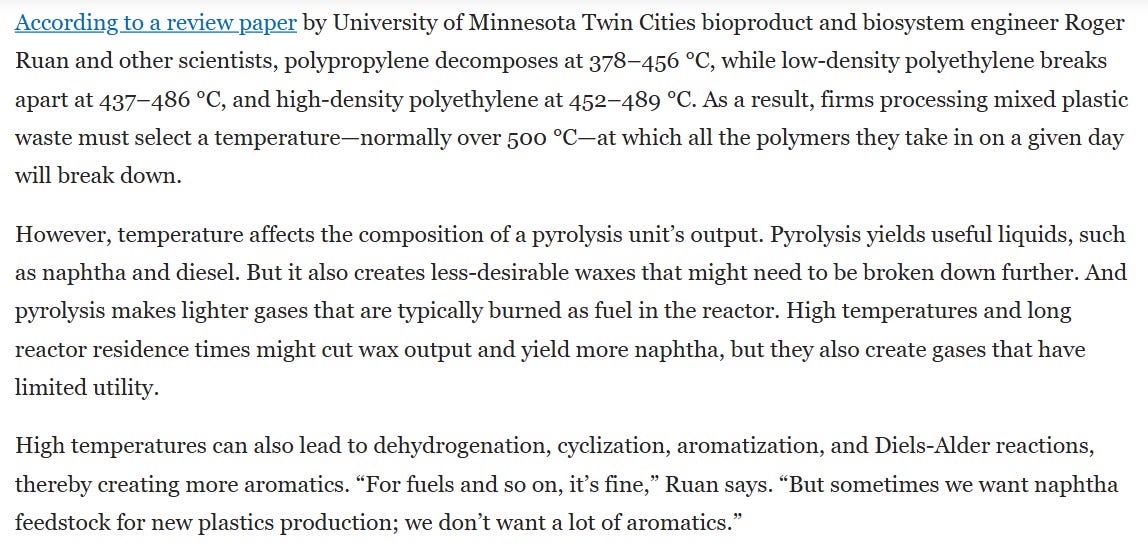

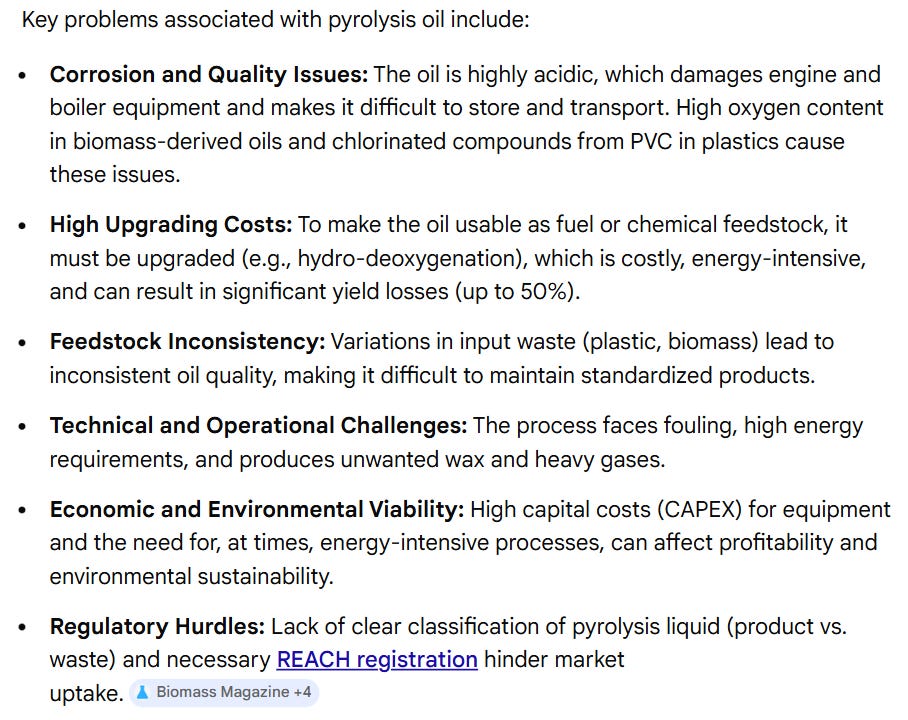

One of the problems with pyrolysis is the heat required for the process, using 400-800 celcius temperatures to break down plastic, which presents many problems:

Source: https://cen.acs.org/environment/recycling/Amid-controversy-industry-goes-plastics-pyrolysis/100/i36

Aduro uses a lower temperature range of 250-350 °C with its water-based method to avoid these problems.

PlasCred also claims lower temperature as one of its advantages:

On our journey around the globe we went to Europe where they're using supercritical steam, high pressure, high temp. A lot of the rotary kilns, they're using 600 to 800 degrees C, which is the wrong tool because it cokes off. We were able to get it down to less than 350 degrees Celsius, so that means I can take all the mixed species of plastic regardless of if it's C1 to C7 and be able to two-phase it at a nice lower temperature. That means less energy—half the amount of caloric value—so we're really successful in that. Better yields and less energy, really correct, and now you generate less waxes and you've got a better finished product. So when you go to on the back end when you go to refine it, you've got a bigger yield upwards of 80%.

Pilot

A company listed on the CSE can be quite liberal with its projections and claims, but as investors, we need to find out what is backing the company’s statements. Many of PlasCred’s claims are backed by results from its pilot plant, Primus, which has a capacity(they’re not running it all the time) of 0.4 tonnes per day, resulting in around 2 bpd of condensate.

Source: https://plascred.com/wp-content/uploads/2024/09/2024-09-11-PlasCred-Neos-FEED-Update-Q2-2024-PR.pdf

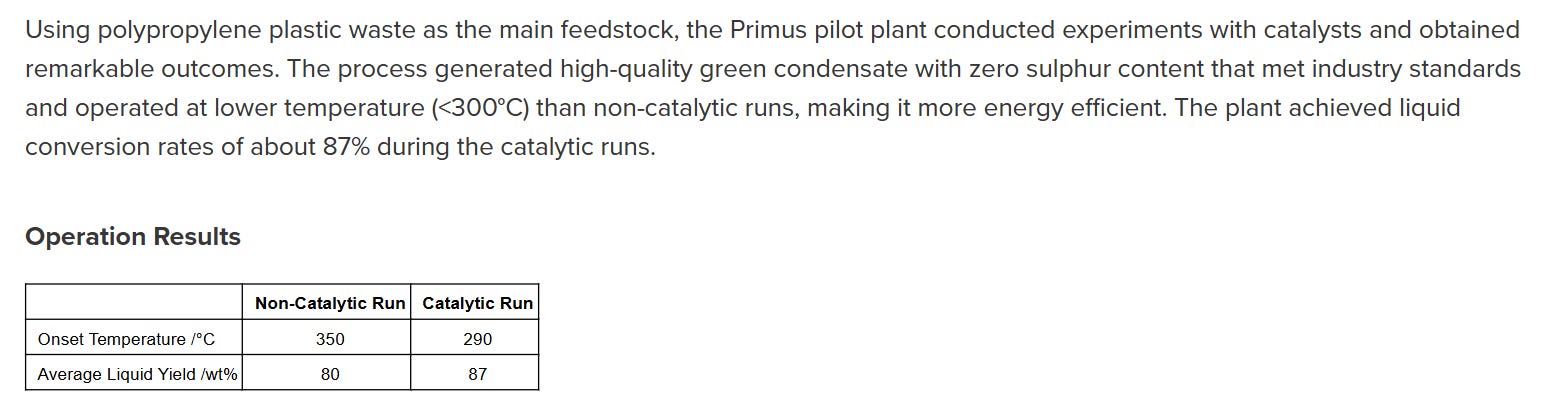

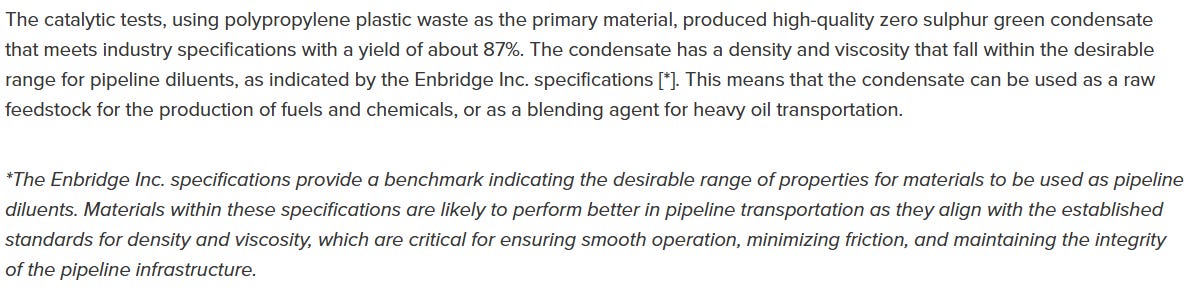

PlasCred says their liquid yields are up to 80%. Which is a decent yield, especially for Mixed plastics. What’s backing these statements?

Pilot results using PP as the main feedstock

Source: https://www.newswire.ca/news-releases/plascred-circular-innovations-inc-announces-initial-catalytic-test-results-with-patent-pending-primus-pilot-plant-822170753.html

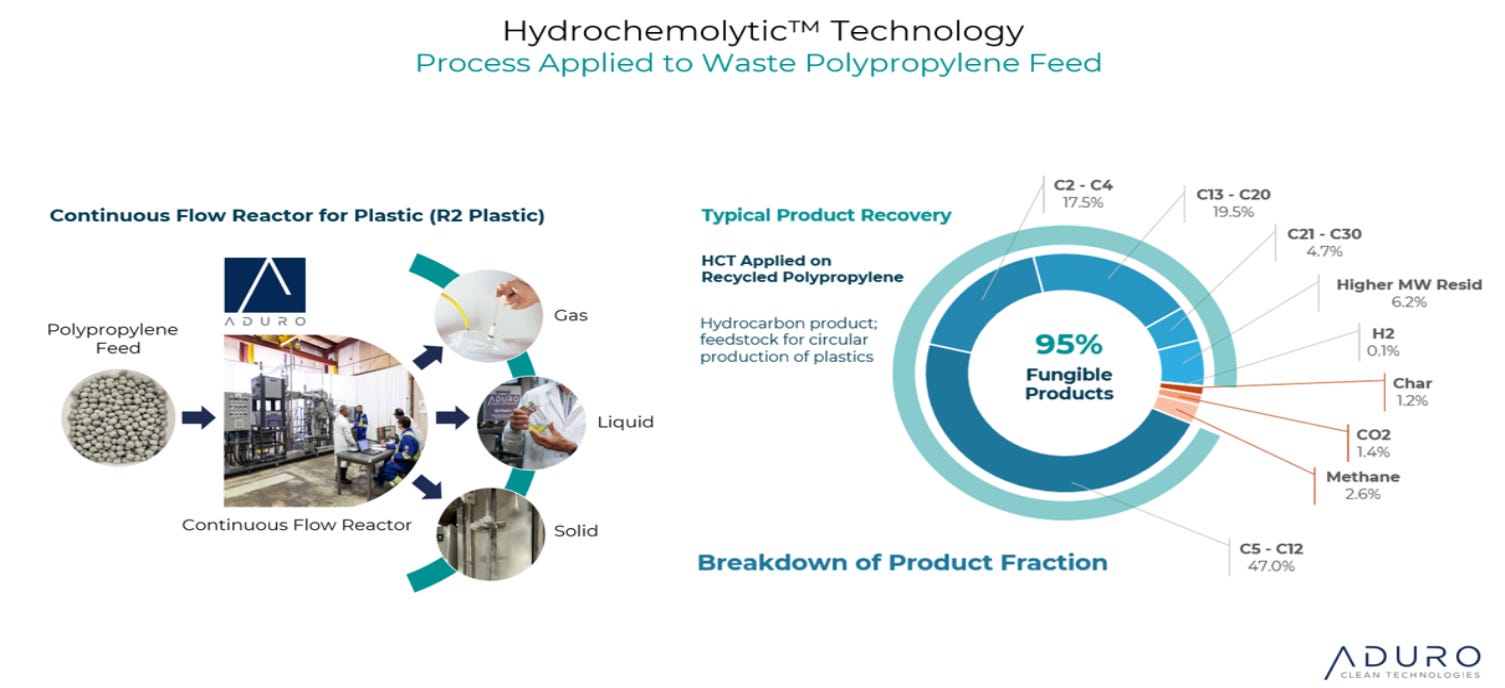

Comparison: Aduro got a 95% yield on PP feedstock

Source: https://www.globenewswire.com/news-release/2024/02/15/2829816/0/en/Aduro-Clean-Technologies-Shares-Sample-Test-Results-from-its-Continuous-Flow-Unit-Experimentation-and-Optimization-Program.html

But for PlasCred, it’s still good. Aduro has the best yield out of everyone for PP. And PlasCred has a higher-than-average pyrolysis yield for PP, which, according to these sources I found, ranges from 55-80%. Source 55-65%, Source 80%. When it comes to finding an average or benchmark, it’s difficult, as there are so many variables and differences between the sources and the ways they arrived at their results.

Pilot results using Mixed Plastic

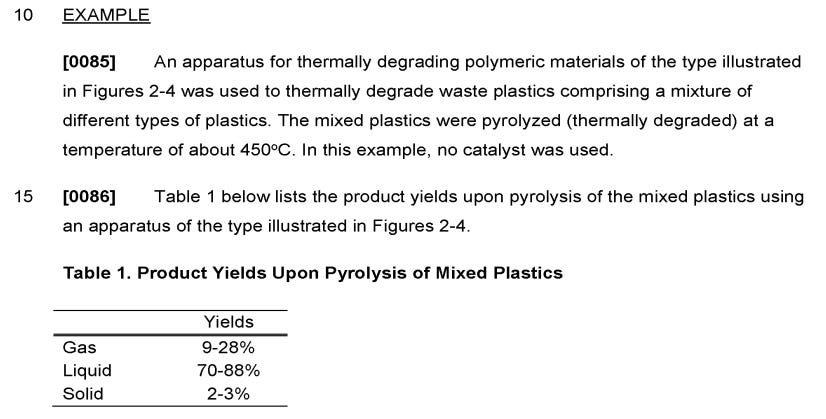

Source: https://cdn-ceo-ca.s3.amazonaws.com/1kpgpuj-plascred%20patent.pdf

With different mixed plastic feedstocks, PlasCred got a range of 70-88%. The temperature here is higher (450 °C) than the temperature the CEO mentioned in the interview, where he said they can process mixed plastics at 350 °C.

When it comes to mixed plastics, what is even more important is whether they can handle problematic plastic types in the mix and truly take unsorted feedstock. The problematic plastic types for pyrolysis are PET and PVC:

Source: https://cen.acs.org/environment/recycling/Amid-controversy-industry-goes-plastics-pyrolysis/100/i36

PlasCred’s CEO is very confident they can handle PVC and PET, supposedly in unlimited quantities:

Limits to the amount of PVC and PET that you can handle?

As much as possible, no limits, no limit, yeah, no limits, yeah

Their presentation does say “up to 5% PVCs”, which would imply limits.

“What happens to the PVC hydrogen chloride in particular? Yeah, so you’re always going to get PVC. Those chlorides are very damaging to the finished product, so you don’t want to bring in those chlorides whatsoever. We have a unique process within our whole burn period and we’ve been able to do a workaround and be able to subtract that. What’s really cool is a lot of the chlorides that will be building up in the plant—they’ll actually come back; we’re going to bring all that back through our wash water to wash the plastic, so actually every molecule gets used.

We have a technology that, say we got a slug of PVC—say 5-10%—not only can we segregate that, but we can actually reuse that and take the chlorides off and basically reuse that as a process within our water. It’s pretty good because we don’t want it to end up in the finished product. That’s why, out of everybody else who is doing pyrolysis, you know, they’ll use that and that can create those chlorides and hydrochloric acids that are damaging. We’ve built a technology into our process that eliminates that and works with plastic.”

So that’s what they say, and the 70-88% yield result was with mixed plastics that “in some embodiments” may include PET and “in some embodiments, the feedstock comprises PVC”. That’s what we have to go off for now.

Similarly, Aduro lacks detailed results when dealing with contaminants, but based on what they have press-released, they imply results of over 80% liquid yield on mixed plastics with PET and PVC. This was from the PR, which highlighted their graduation from Shell’s GameChanger Program, which in itself gives these results more validation, as the tests were conducted with Shell’s oversight:

Following the agreed program, Aduro conducted a series of technical evaluations to assess the performance of its patented chemistry, including selectivity toward steam-crackable hydrocarbons in the C₅–C₂₃ range, suppression of olefin formation, and tolerance to common contaminants such as PET, polyamides[nylon], and PVC. Under the tested conditions, the process yielded over 80 percent liquid hydrocarbons with lower gas and char formation. These findings suggest potential advantages in feedstock flexibility, product selectivity, and process efficiency. In addition, Aduro advanced its understanding of reaction kinetics and process design parameters, which now inform the further development of its proprietary system architecture.

These results confirm that Hydrochemolytic™ Technology holds the potential to convert complex, contaminated waste plastics into high-quality liquid hydrocarbons under continuous operation, using readily available industrial equipment.

Source: https://investors.adurocleantech.com/press-releases/press-releases-details/2025/Aduro-Clean-Technologies-Graduates-from-Shell-GameChanger-Program/default.aspx

The fact that they can say over 80% rather than up to 80% like PlasCred is significant, as it implies that all the mixes they tried, including those with contaminants like PET, Nylon, and PVC, still achieved liquid yields of over 80%.

The End Product

PlasCred obviously talks favourably about their end-product, but one concern raised is that, if they do pyrolysis, their product is technically pyrolysis oil, which has a bad reputation. Here is a quick AI summary of the problems:

PlasCred claims to be able to make a better product than what usually results from pyrolysis, and they call other types of pyrolysis oil “monster juice”.

On our journey, we watched how a lot of people were doing pyrolysis. They create “monster juice” at the end — they don’t have a real goal of creating a finished product, and it’s not very good. Anybody can do pyrolysis, but you really have to be able to tear the molecule apart. Because of our process, we have a patented reactor[patent pending] and an ex-situ catalysis process that allows us to put the molecule back together the way we want and come up with a finished C5 Enbridge-spec condensate.

This currently trades for about $105 to $110 per barrel, so it’s very profitable.

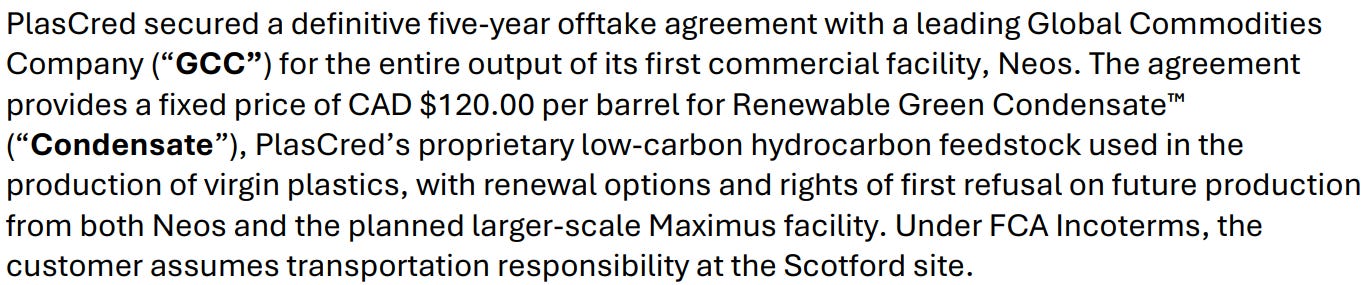

What gives PlasCred’s statements weight is their Offtake agreement. This provides a fixed price of $120 per barrel for a 5-year period with a “Global Commodities Company”. The CEO has revealed that this company is Trafigura(source). A company with a revenue of $240.3 billion in 2025.

Source: https://plascred.com/wp-content/uploads/2025/06/2025-06-03-PlasCred-YE-2024-PR.pdf

Trafigura had tested the product produced by their pilot (I assume) and, based on that, said they could pay C$120 per barrel for it, which amounts to roughly C$1000 per tonne(US$730). And that underpins their financials and profitability assumptions.

PlasCred says that the product is used in the production of virgin plastics. Can it actually go straight into a steam cracker to produce new plastic? Whether it requires expensive post-treatment has remained unclear to me. After asking shareholders and the IR, shareholders weren’t sure, IR didn’t respond, I assume it can’t go straight into a steam cracker, because it would be a big selling point if it could, and that would also explain the pricing in the offtake, which should be higher for a product that could.

This is how they describe the product they got from recycling PP, which is good feedstock.

Source: https://www.newswire.ca/news-releases/plascred-circular-innovations-inc-announces-initial-catalytic-test-results-with-patent-pending-primus-pilot-plant-822170753.html

Given the fact that they don’t make it clear whether it can go in a steam cracker as it is when PlasCred sells it, and they have multiple use cases outlined, some of them seemingly lower value like pipeline diluents and the lower range pricing, I think the product is not of that quality, but if they can sell it at C$120 and have no problem with cost over runs and scaling the process, it doesn’t matter as much their process would be very profitable either way, which will be covered soon.

Also, given this green condensate that used PP as feedstock, it met industry specifications, but I didn’t find another official result stating that a product derived from a mixed feedstock with contaminants met industry specifications. In general, they claim they can do it, but I would like to see that result in an official PR. I want a clear answer to this, and for the steam cracker question, because I may change my PlasCred positioning based on those answers.

Why I made a big point about the product’s ability to go straight into a steam cracker is that if a company can do it, they can truly claim plastic circularity and secure premium pricing. Very high pricing with government incentives in certain countries. This video dives into how Aduro could easily get over 2k USD per tonne. Aduro’s goal is to produce an end product from mixed plastics that can go to a steam cracker as is or with minimal modification, and they have some promising initial results from testing their mixed plastic-derived product in a pilot-scale steam cracker:

The trials were carried out in October 2025 at an established pilot-scale cracking facility in Europe, using a hydrocarbon liquid product Aduro produced from a mixed waste plastic feedstock consisting of polyethylene, polypropylene, polystyrene, PET, and polyamide. The Hydrochemolytic™ oil was processed in the pilot-scale steam-cracking furnace as-produced, without dilution or further pre-treatment, under various operating conditions.

Cracking of the Aduro Hydrochemolytic™ oil was achieved under stable furnace operation with yields of ethylene and propylene, key building blocks of polyethylene and polypropylene, comparable to those from comparable fossil feedstock. Most significantly, the cracking trials showed that this particular Aduro product may be used as a cracker feedstock without additional hydrotreatment or dilution

“This testing was completed by a global organization with deep expertise in steam-cracking technologies and operations, and their evaluation points to strong potential for liquids produced through our Hydrochemolytic™ Technology to meet the strict performance needs of cracking operations,” said Ofer Vicus, CEO at Aduro.

Source: https://ceo.ca/@GlobeNewswire/aduro-clean-technologies-reports-successful-pilot-scale

To summarise this section, Aduro clearly shows more potential with their end product. PlasCred product, while lower value, seems to be good enough for various commercial uses validated by the offtake with Trafigura, which is a big deal as it implies they can avoid many of the problems of pyrolysis peers, and the offtake underpins their financial projections for their commercial plant and helps with their most immediate challenge, funding that plant:

This was around 40% of the article. 60% is behind a paywall and covers PlasCreds funding situation, commercialisation, long-term growth story, CN rail, Management, catalyst and risks, thoughts around my positioning, catalyst, risks, and most importantly, the final PlasCred vs Aduro clash.

To access paid content for free, you can use the two buttons below to recruit new AlmostMongolian subscribers. Free subscribers count. The rewards are stacked.

PlasCred’s path to commercialisation

…