Update: Valeura Energy, Metro Mining, Illumin and Ensign Energy Services

HUGE update(paywall removed)

Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program which means I have a financial relationship with Seeking Alpha.

4 companies BIG update. I have written about each of these companies and it’s time to do an update. I like how these investments theses are developing. The stocks are doing fine in terms of price action, but I think each one is going higher based on some of the things I will be covering in this article.

Check out my Mongolian Ad: Mongolian Ad Link

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: THE AFFILIATE LINK

Valeura Energy

Let’s see what’s going on with my favorite. Valeura gets to go first because it’s my favorite.

Source: Google

Valeura should be up way more because we finally got the tax restructuring. Which was one of the big catalysts I talked about in my original write-up.

Valeura had a lot of tax loss carry-forwards, but they were only being used for 20% of their production meaning the benefit was being realized slowly. Money now is more valuable than money in the future so the faster they can utilize those tax losses the more value the market will attribute to them.

Source: ceo.ca

According to this PR, they have 397m USD of tax losses as of September 30th.

Note that Jasmine field is excluded from this arrangement which is around 30% of the production. But going from 20% to 70% of production being able to take advantage of these tax losses is a huge benefit because Thailand has a 50% tax rate on profits for oil companies.

These percentages of production are rough numbers.

Let’s do some math. I’ll use this year’s cost guidance higher range because we have higher production now and current oil production and current oil price to count the next 12 months with these tax benefits

73,8$(current brent)*26 000*365=700 362 000

“Royalties for Thai I licences are a flat 12.5%, and for Thai III licences are a sliding scale between 5% and 15% based on sales volumes” I did not find more details so let’s say royalties 10%=70 036 200

opex=235m

Capex=155m

SG&A=30m

Exploration=8m

Pre-tax profit=202 329 800 USD

70% of it has no taxes=141 630 860 USD

30% has 50% tax=60 698 940*0,5=30 349 470 USD

171 980 330m USD After-tax profit rough estimate for the next 12 months using the current Brent oil price and they would have 194 670 200 USD of tax losses left after this. So basically another year.

This is how I understand it would work, but no promises and they have not given all the details yet.

This company has a 406m USD market cap and 250m USD EV. (156m cash and no debt according to Q3 operations update) EV to after-tax profit based on that calculation=1,45

Also, the Nong Yao C production increase was another catalyst that was achieved.

Source: https://ceo.ca/@accesswire/valeura-energy-inc-announces-nong-yao-c-production

Source:https://ceo.ca/@accesswire/valeura-energy-inc-announces-q3-2024-operations-and

Nong Yao is now their biggest and it always was their most profitable field and now has access to the tax losses.

This is from my original write-up Link to the Original write-up

So they have achieved both of these catalysts Nong Yao and Tax thing. The one factor that is out of their control is the oil price which has gone down from 90$ Brent to 73,8$.

The stock performance is +48,4% from when I first bought, +29,7% from my cost basis, and -4,45% from my original write-up. The last one only reason for it is the oil price, but as I went over in my calculation the cash flow is very strong even at the current oil price.

The other 2 catalysts for Valeura are reserve replacement and capital allocation. Reserve replacement results will come out early next year. I’m expecting strong results like last time. And capital allocation is the 1 catalyst we are still waiting for as Valeura has been hoarding cash.

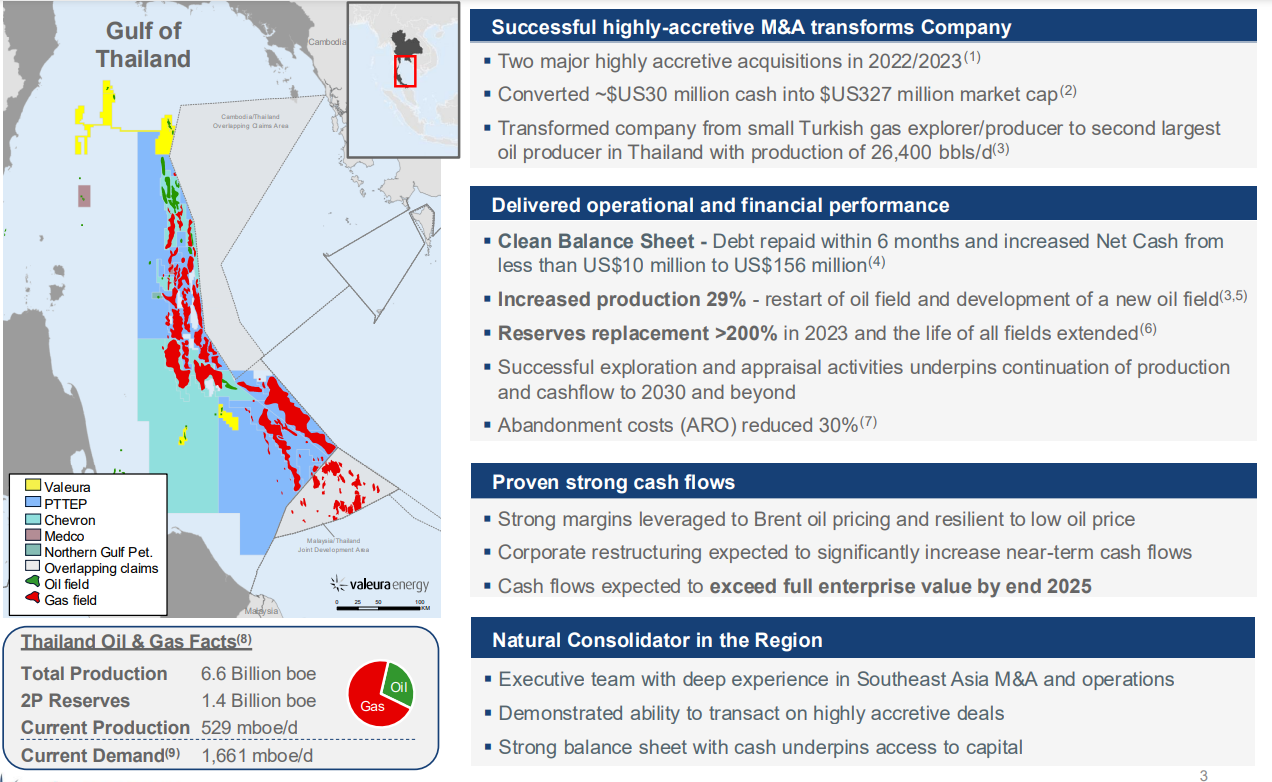

They are obviously working on an acquisition which is their speciality. They did the best acquisition I have ever seen. This was the Mumbadaalalalala acquisition. The Kris acquisition was very good as well. They got those tax losses from the Kris acquisition and are applying them now to Mumbadala fields. Very nice synergy there. Usually, I don’t want the companies I invest in to do acquisitions, because so many times they are not good or they take a long time to pay off, but with Valuera I want them to do acquisitions because of their track record.

From their new presentation, we can get some ideas for what they are planning on that side.

Source: https://www.valeuraenergy.com/wp-content/uploads/2024/10/2024-10-corporate-update-VF.pdf

They are showing all the fields and different operators in the region. Then later they say this when they are talking about the oil and gas sector in Thailand.

“Reduced # of operators ▪ Major companies exiting due to materiality ▪ Very few operators of Valeura’s scale and capability ▪ Governments seeking proven operators Shallower buyer pool ▪ Diminishing pool of credible buyers ▪ Difficult to raise capital for new entrants ▪ Competitive pricing and unique structures possible”

Major companies exiting. From the companies shown in the picture, Only oil major is Chevron. Mecdo(Indonesian company) and PTTEP(Thai national oil company) are pretty big as well, with revenue in billions so it could be one of those as well.

I would guess it’s Chevron becau😴😴😴

They also mention the usual methods for returning capital

“▪ Potential shareholder returns - Capacity for share buybacks in the short to mid terms - Future growth will support sustainable dividend”

I guess these are 2nd to acquisitions when it comes to management preference. If they can’t get anything done on the acquisition front they will do buybacks and dividends. This has also been my impression from their other presentations and earnings calls. They think of growth as a priority.

Source: https://www.valeuraenergy.com/wp-content/uploads/2024/10/2024-10-corporate-update-VF.pdf

This is our new timeline. A lot of organic growth plans. I’m optimistic about those based on their track record with these assets. They mention maintaining production at the current assets until 2030’s.

“Capital / Organic Investment ▪ Capex: Maintain production 20 mbbl/d to 25 mbbl/d into the 2030’s(1) ▪ Expex: Selectively target organic resource growth”

The whole Valeura bear thesis has been their lack of reserves, but they have shown and are showing that if you invest in these assets there is still a lot left. Now they are saying they will maintain 20-25k BPD into the 2030’s which is a huge statement.

I wonder if they will be able to get the production from these assets above 30k BPD before 2030’s. The amount of organic growth initiatives they are doing makes me think that is their goal.

Source: https://www.valeuraenergy.com/wp-content/uploads/2024/10/2024-10-corporate-update-VF.pdf

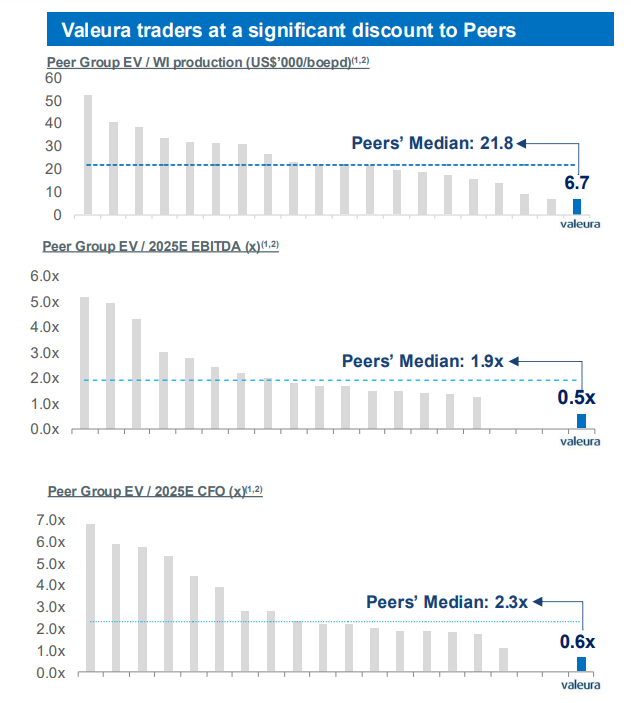

Another valuation reminder at the end. The sector is cheap and Valeura is the cheapest one in the cheap sector.

update to the update

The next day after this article was released Valeura finally announced a stock buyback

Source: https://ceo.ca/@accesswire/valeura-implements-share-buyback-programme

10% of the float is easy for them to do. I think this is about keeping the shareholders happy while they work on their acquisition. Regardless, this is a very positive development.

Another update to the update 28.11.2024

Source: https://ceo.ca/@accesswire/valeura-energy-inc-announces-jasmine-development-drilling

-26% increase in production in the Jasmine field from before the new wells were added.

-Another five-well drilling program started in Manora, because of the strong performance of Nong Yao and Jasmine I'm also optimistic about Manora. Although it is their smallest field, but this means potentially a much higher increase.

-"We expect the results of these wells, and the recent production rates to be considered as part of our year-end reserves assessment, and to support our target of achieving more than a 100% reserves replacement ratio." This will be a big catalyst next year if they overdeliver on reserve replacement. Which I predict they will.

Valuera also announced a CEO interview on the same day and I made some notes.

-200m extra near-term cash flow from tax losses "supercharging" the company

-This is why the company can do buybacks at the same time as pursuing organic and inorganic growth

-Q4 production 26k BPD and even higher going into 2025

-Expectation for 2025 production above analyst guidance

-"looking at a really good number" talking about the 2024 reserve replacement number

-"Early in January we'll actually release our year-end or quarter-end results watch for the cash flow the cash numbers there we think it's going to be a very good quarter for us"

-Wassana redevelopment to extend production to mid-2030s even potentially to 2040s. Decision on this redevelopment likely in Q1

Source: https://www.valeuraenergy.com/wp-content/uploads/2024/11/2024-11-corporate-update-V3.pdf

As I look at this new timeline I’m quite optimistic as operationally everything except the tax loss restructuring has happened on time. And in that case, they were working with regulators so a lot of it is out of their hands. But in terms of organic growth and reserve replacement, they consistently outperform and are on time and under budget.

The Wassana redevelopment, Jasmine more infill drilling, and new exploration target and Manora infill drilling. I think these will provide positive smaller catalysts paired with stock buybacks while we wait for the acquisitions.

Source: Google

The stock because of its strong performance is not far away from the highs despite the oil price weakness. And I do not think oil prices can go down a lot from here without a black swan event. OPEC+ has already delayed their production increase twice and now there are rumors they are delaying them even further. They clearly don’t want to raise production in this oil pricing environment and I don’t think the US producers will “drill, baby, drill” either at this oil price despite what the new admin does. We have heard this from many big companies in the US. Well, I could go on about the oil price, but my point is the risk from the weak oil price is in my opinion mostly priced in while the reward from potentially rising oil price is not.

If you keep doing DD on Valeura and put it all together you will find it difficult to pass it.

Ensign Energy Services

I laid out the whole investment thesis in my video released last May.

Ensign's investment thesis is all about deleveraging.

Market cap 557m

Debt 1,09B

FCF is being used for deleveraging.

In theory, every dollar of debt paid off should be added to the market cap everything else being equal. Of course, this is not how it works in practice because valuation changes as the market’s views and market conditions change, but this is something that adds value to the common share every quarter.

So Ensign plans to reduce debt by 200m this year, which they are expected to be able to do, and another 200m next year.

What the stock price will do is based on sentiment which is based on how fast the market thinks they can deleverage and that is based on FCF now and what FCF will be in the future.

FCF and the sentiment around is based on what kind of numbers the company is putting out and what kind of market environment we will see in the foreseeable future. Ensign just reported their Q4 numbers and we had the US election.

So Let’s talk about the numbers, the impact of the US election and take a look at what management said in the call to see how the thesis is progressing.

Q3 was decent. The numbers were almost identical to last year’s Q3

Source: https://ceo.ca/content/sedar/ESI-2024-11-01-interim-financial-statementsreport-english-141f.pdf

FCF is counted as operational cash flow-capex, but to get a better number to see the real profitability I will use Mongolian earnings that I used in my video.

Mongolian earnings=operating income+deprecation and amortization-capex-interest expense-taxes

24.5+91-37,4-23,8-2,8=51,5m of real cash flow

annualized 206m for debt reduction

So that is a decent result. Nothing crazy. Note the reduction in interest cost which has always been an important part of the thesis.

Considering that interest cost at the q3 run rate is 95.2m per year.

The interest was 31,2m last year Q3 and it’s 23,8m this year. This is due to them paying back debt and the interest rate being lowered due to it being a floating interest rate.

In the Q3 earnings call they said this

“Interest expense will be between that $20 million to $25 million. So that leaves you about $65 million of free cash flow left over for debt repayments. There is potential for some non-operating cash inflows from some property and asset dispositions that could come into Q4.”

They are predicting 65m of FCF for debt repayment for Q4 which annualized is 260m. Which would be a 46,7% FCF yield.

I’d rather make that my expectation for the next year based on what I will cover next.

Market conditions

Source: https://ceo.ca/@newswire/ensign-energy-services-inc-reports-2024-third-quarter

Total operating days were a bit higher than last year. The weakness in US was offset by the strength in Canada.

The Q3 earnings call was also quite bullish about Canada

“starting with Canada. The combination of expanded pipeline capacity, both for oil and LNG, the tightening differential, and with the low Canadian dollar, the net effect is that more drilling will occur in the Western Canadian sedimentary basin. It's safe to say that the demand for high-spec singles and high-spec triples is at the highest it has been in quite some time, at least a decade. This has also helped to drive the high-spec double market to enjoy utilization above 60%, which is a typical threshold where a contractor is able to move pricing. Almost one-third of Ensign's Canadian fleet are high spec doubles, so we have lots of product to feed into this construct.

Our fleet of high-spec singles and high-spec triples are essentially booked well into 2025. Canada is back to the first quarter levels of activity, which rarely happens in the Canadian market in the third quarter.”

The Canadian market is very strong next I’ll add some quotes from Precision drilling Q3 call to give more info on the Canadian market

“We've been pleasantly surprised by the near instantaneous customer response to these market drivers with a wide swath of our client base increasing activity almost immediately following the Trans Mountain Pipeline entering service. Utilization for our Super Single rigs, drilling heavy oil, and for our super triple rigs, drilling Montney Gas and gas condensate are both at historic highs for these rig classes.

And I'd say the demand was probably 10% to 15% higher than we expected resulting from that pipeline expansion. So we're watching anxiously to see how LNG Canada fires up. We know the gas is going to the pipe now to get the facility commissioned.

We're still hearing the first shipments are going to be happening at the end of the second quarter in 2025 for LNG Canada. So I think that we'll see rig demand increase and it might be two or three rigs or it could be a little more, maybe four or five rigs. But it feels like demand is in that kind of two to five rig range to balance out the needs for LNG Canada.”

So this year Canadian market strength was based on TMX pipeline expansion and next year LNG Canada will be added on top of it. Considering that new rigs are not really being built and US might rebound next year rates for these rigs might just rocket up.

Back to Ensign Q3 earnings call.

While we witnessed very competitive bidding into the third and fourth quarter, we did strategically place ratcheting rate increases, compounding as we moved through the fall season and into the winter drilling season.

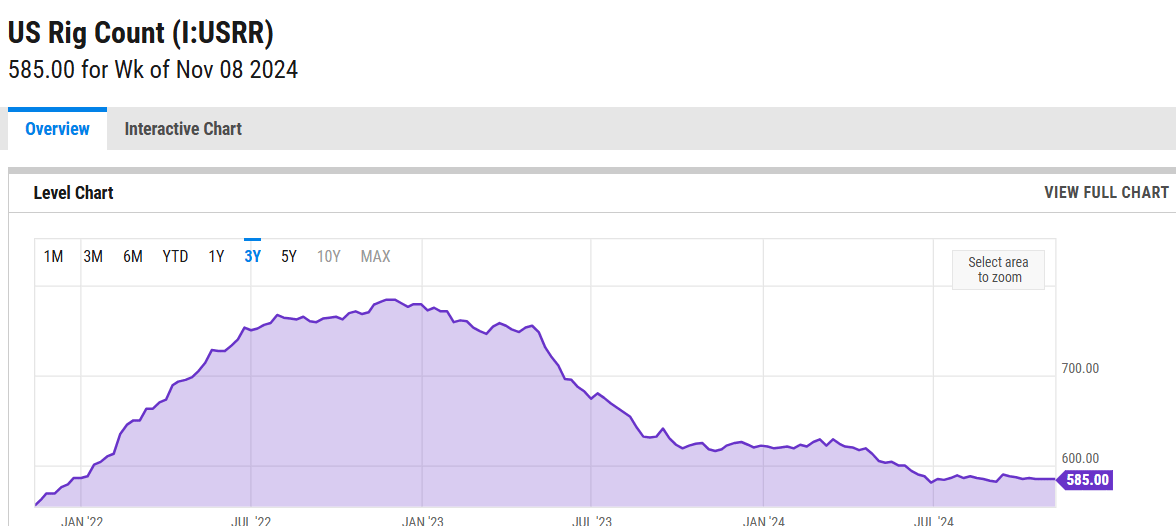

Demand is very high, revenue is booked well into 2025, and they are talking about moving up pricing. Rates going up while this↓ is US rig count is big.

Source: https://ycharts.com/indicators/us_rotary_rigs

“Our US well-servicing business unit, which is focused primarily on the Rockies in California well-servicing market, continues to enjoy high-utilization in the upper 80s and delivered a record quarter.”

nice.

“And as I mentioned, the cost to put a new rig together is right now burdensome. Rates are not up into the 50s, where they would need to be to support a $50 million super-spec triple type rig, which is what the operators are always wanting.”

“Going into Q1 with 2025 looking fairly stable to static kind of year-over-year. We don't really see a big demand for CapEx or anything like that. So everything is looking like I said on the right side going forward."

Not building new rigs and no big Capex which is good. This is a supply/demand thesis and we don’t want anyone building rigs.

“looking forward, it continues to be an exciting time for Ensign as we build on last quarter's robust Canadian and international market fundamentals. We are seeing an improving long-term outlook in all our US markets, but don't expect any meaningful growth until back half of '25 or into '26. With over $800 million of forward revenue booked under contract”

Quote from Precision Drilling Q3 call

“we remain confident in the Canadian and international markets while we expect a modest increase in the U.S. as reloaded budgets for 2025 kick in.

With 2025 budget reloads on the horizon, we are seeing signs of a modest rebound in U.S. activity as we've added seven term contracts since the end of the second quarter with activation dates ranging from beginning late this year into the first few days of 2025.”

Both Ensign and Precision are saying similar things about the US market there is an improving market going into next year, but nothing significant.

Trump’s win “drill baby drill”

Is this big for Ensign?

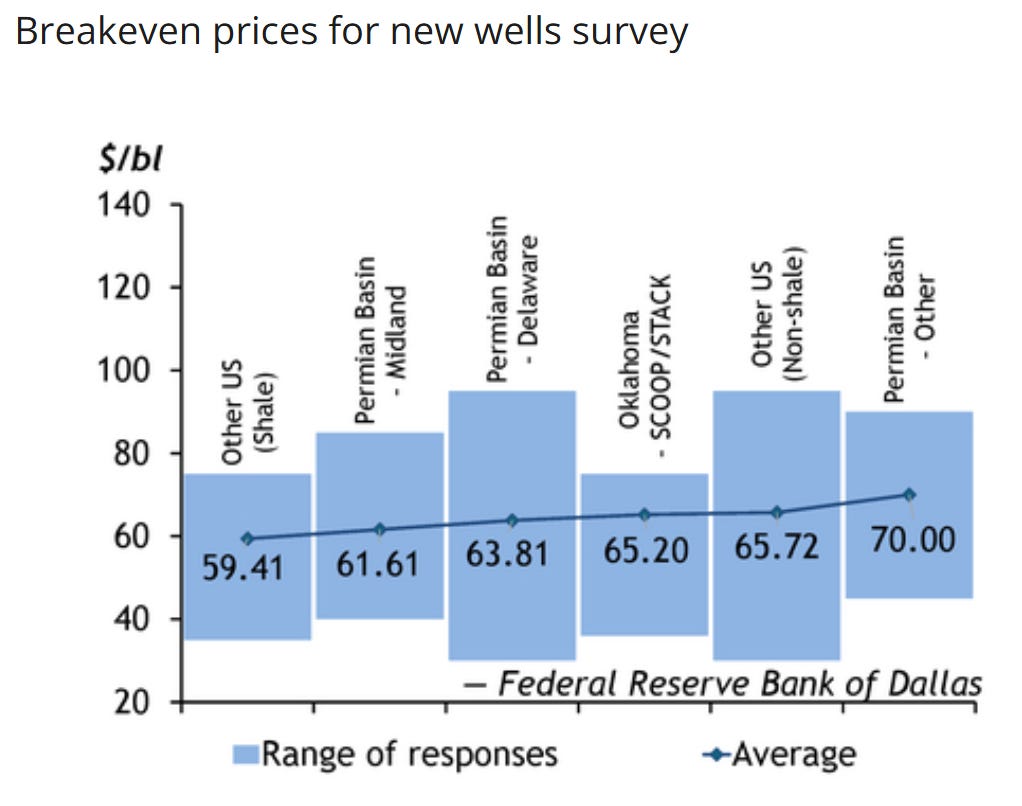

We know Trump who will be in office January 2025 has promised “drill baby drill” which would obviously be very good for Ensign as Ensign would be the company drill baby drilling, but I’m not sure this can happen at the current oil prices.

Source: https://www.argusmedia.com/en/news-and-insights/latest-market-news/2617831-permian-producers-face-new-headwinds

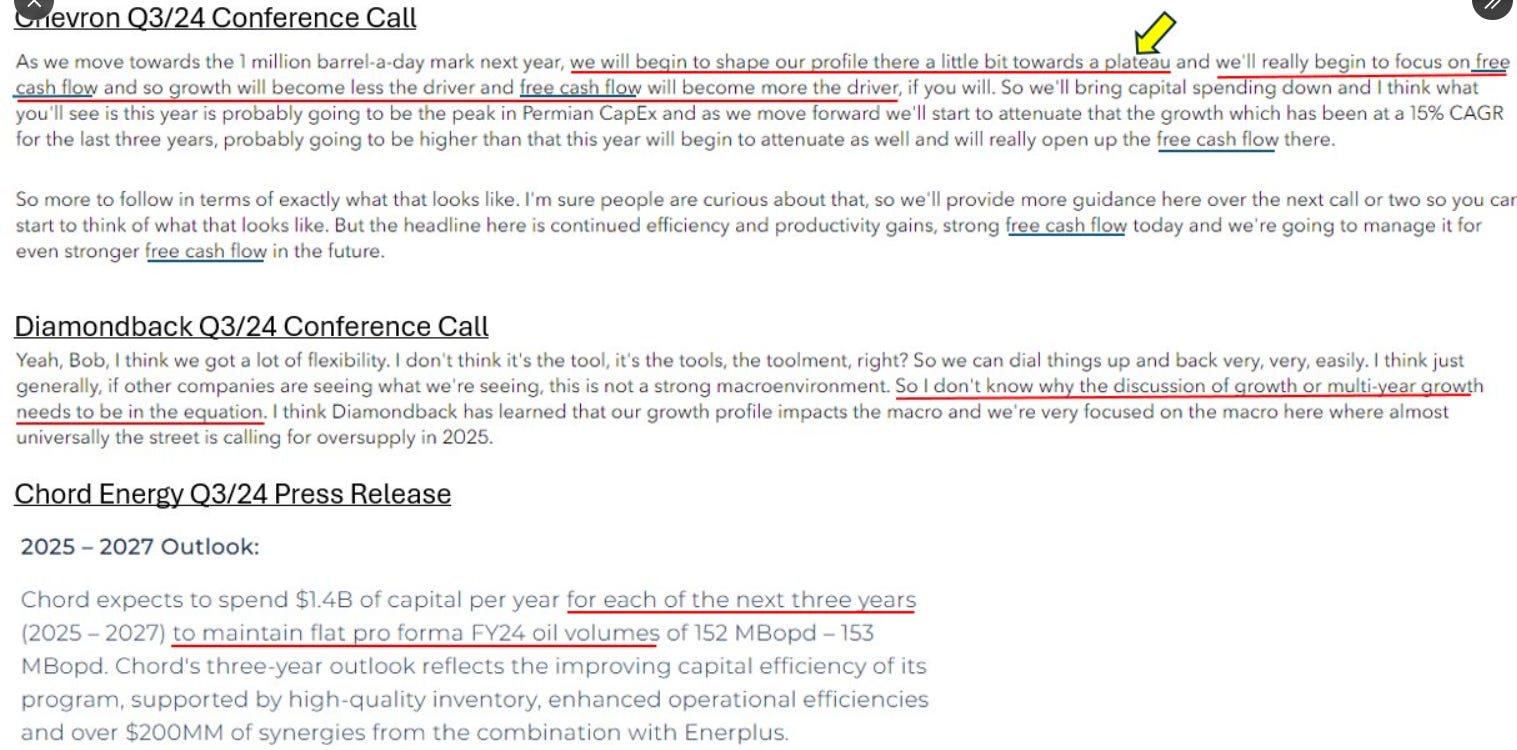

We are at 70,43$ WTI right now. This is not an attractive price to “drill, baby, drill” based on the breakevens for new wells. This is also a time when investors are increasingly demanding less production growth and more buybacks and dividends and telling us they are going to have flat production.

Source: Eric Nuttall, X

Eric Nuttall who is an energy fund manager tweeted this recently. Biased or not these are real quotes and point to a trend I’ve seen from elsewhere. I tend to agree with him that “drill, baby, drill” is not something Trump can just make happen.

I do think Trump winning will be a net positive for Ensign. One reason is the sentiment if the president of the US is constantly talking about increasing drilling it helps the general sentiment and improves expectations which improves valuation even if he does not deliver.

Also, Trump's policies should in a vacuum increase drilling. If everything else stays the same, but another admin is giving more leases, cutting regulation, putting more pro-oil and gas people in regulatory agencies, making permitting faster, fully supporting the LNG export expansion(which Biden was opposing), supporting new pipeline development this should all else being equal increase drilling.

Counter point is simply that if it’s not economic or the investors don’t want it it’s hard to force it on private companies even though there will be a net-positive effect because of all the things I mentioned.

Also, Trump’s tougher stance on Iran could increase oil prices which could in combination with his policies make “drill, baby, drill” possible. From what I have seen the stance towards Iran seems way more hawkish than even during the last Trump administration from Trump himself “If I were the president, I would inform the threatening country, in this case Iran, that if you do anything to harm this person, we are going to blow your largest cities and the country itself to smithereens," and people around him like the vice president-elect JD Vance who said “A lot of people recognize that we need to do something with Iran but not these weak little bombing runs” and “If you’re going to punch the Iranians, you punch them hard, and that’s what [Trump] did when he took out Soleimani”

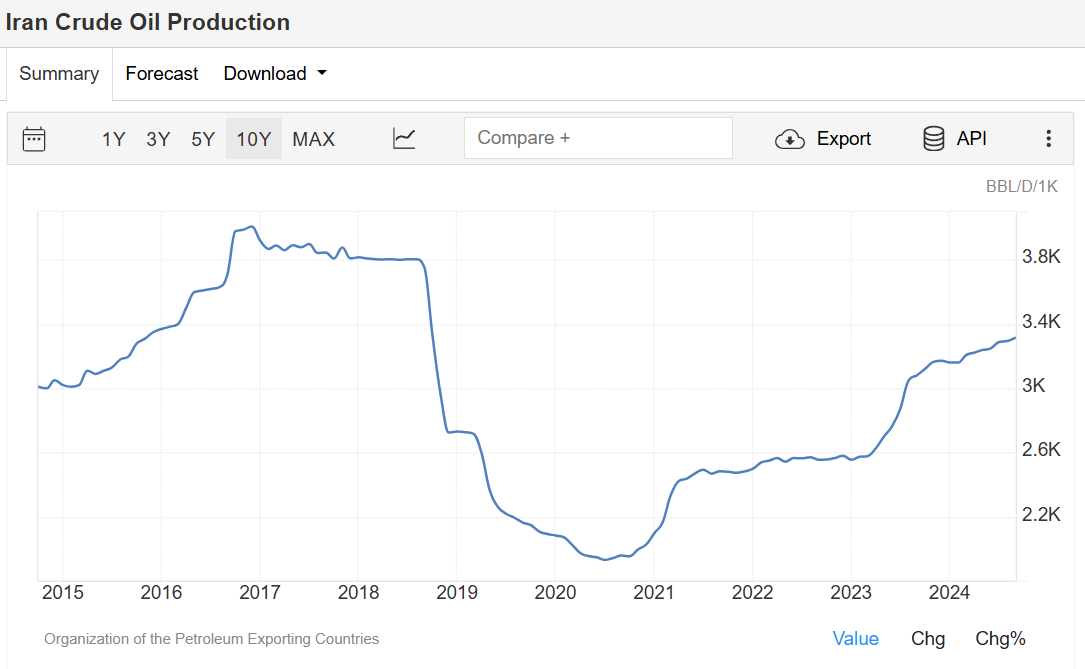

As we know Trump was able to crush Iran’s oil industry with Sanctions. Iran’s oil production has since recovered with a softer stance from Biden.

Source: https://tradingeconomics.com/iran/crude-oil-production

If Trump could take out 1-2% of the world’s oil production this should have a positive impact on prices as oil is priced at the margin, but maybe an increase from Opec+ and Trump’s own energy policies could do a lot to offset that.

Also, Trump wants to stop the Russia-Ukraine war, but this should not affect global oil supply as the sanctions were not able to curtail Russia’s oil production in the first place. Russia simply changed its customers and rerouted its oil exports to places like China and India.

Trump has also been saying he will refill the strategic petroleum reserve which was heavily drawn down by the Biden admin. This could help prices somewhat if he does it.

I don’t there is much else to comment about that.

Summary: Trump’s win is net-positive for Ensign, but I doubt there will be a big boom in drilling just based on Trump’s policies if the oil price does not cooperate.

For Ensign it’s important to note that the cash flow now is already strong when the US market is weak and the Canadian market only looks to be getting stronger and the supply of rigs is constrained this means US market strengthening is not vital for Ensign to be a successful investment, but more like a bonus.

Let’s talk about price action a bit.

Source: Google

Since 2022 we have seen the trend that the stock tends to pull back when it gets to the 4$ area and bottoms at the 2$ area. So sell 4$ buy 2$ right? Maybe. I will be thinking about this when it gets there. Although what is interesting about the strong performance this year kind of a slow climb is that the oil price is down -1,7% ytd. 2 of the 3 runs we see on the chart are when oil price was going up and this recent strength is happening despite the weak oil price.

I think this is because of the obvious strength in the Canadian market, slow recognition of the undervaluation, and strong buying from an institutional investor Fairfax Capital

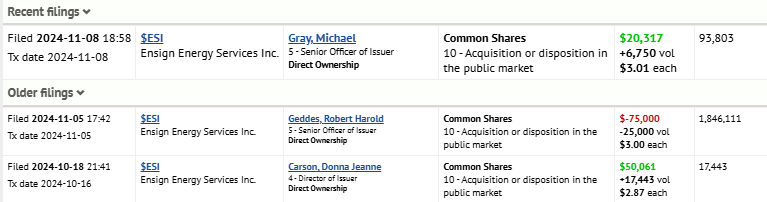

Source: https://ceo.ca/esi, SEDI insider filings

They have been loading up and have acquired almost 10% of the shares outstanding.

Source: https://ceo.ca/esi, SEDI insider filings

These are what the other insiders have been doing. Mostly buys, but not large sums.

To sell at 4$ area? Maybe depending if I really want to raise money for something else. One dynamic here is that even if this chop keeps happening the company fundamentally keeps increasing in value per share as they keep paying off the debt.

I’m also wondering if we could get a Trump-driven speculative rally to the 5-6$ area. Republicans won the Senate and the white house. the house is still unclear, but it seems like they will win the house as well so Trump should be able to execute their agenda. So if he gets inaugurated and immediately does a million executive orders on energy, starts going after Iran, and starts refilling the SPR. Maybe we get a big rally on Ensign stock because of these things. That could be a good time to take profits.

Illumin

What I’m writing in this update is based on the assumption that you have read my original write-up. Link here: Link

Illumin got a CEO by the name of Simon Cairns who described himself like this in the first quarter earnings call:

“Firstly, though, a little bit on my background. Through my 24-year career, I've been focused on driving growth and performance in technology, services, and SaaS platform companies. My expertise includes strategic leadership, finance, marketing, operations, and business and corporate development. Before joining illumin, I served as the Chief Executive Officer of SPUD, Western Canada's largest online and omnichannel retailer of fresh foods and healthy products. At SPUD, I was responsible for returning the business to growth and performance by focusing on A, continuously generating value for the customer; B, significantly increasing financial performance; C, reviewing and aligning our operations for organizational effectiveness; and D, reinventing our brand value. Before SPUD, I served as the Chief Executive Officer and General Manager of PNI Media, an enterprise class e-commerce and value-added services SaaS platform provider. In that time, I helped drive the business firstly to $400 million and then three years later to over a $1 billion a year.”

Simon was appointed in 27.3. And so far his performance is quite good. As he has been CEO for the second and third quarters and the third quarter is already showing a lot of improvement.

Source: Google

Since my article, the stock has moved up +23,03%. Now above my cost-basis which is nice. On Friday they released their Q3 earnings and the stock closed the day +10% in a reaction to strong results. It was not a proper reaction. The stock should have gone up more.

So as you and I know from reading my write-up Illumin is not priced like a profitable growth company even now nor it’s priced like a growth company or a highly profitable company because based on financials from recent years Illumin is not that kind of company.

market cap=95m

Cash=51,4m, Debt free (based on Q3 numbers, all in CAD)

EV=43,6m

Revenue TTM=127.5m - FCF around breakeven - trading at EV/S=0,34 and P/S=0,74

Obviously this is not a valuation of a growing ad tech business. A highly profitable and growing Adtech company The Trade Desk trades at P/S=26.52 and EV/S=26.12. This is not far from what Illumin traded at peak hype at the start of 2021.

Illumin is currently priced like a company with flat revenue, flat profitability, and a strong balance sheet and that is how it has been since 2021, but there was a shift in Q3.

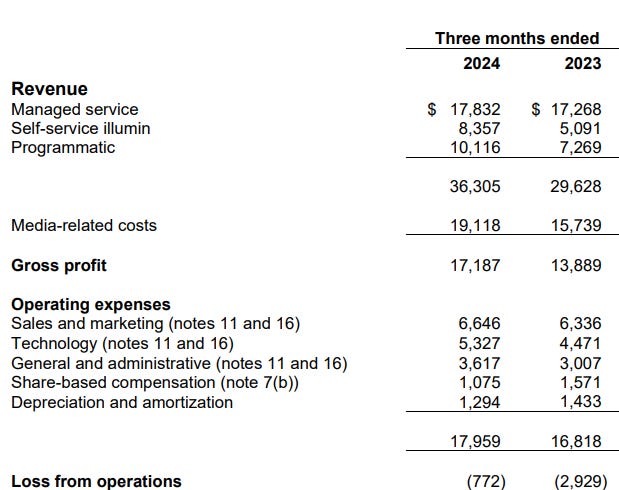

Source: https://illumin.com/news-press/illumin-reports-third-quarter-2024-financial-results/

23% y-o-y growth is quite an improvement from the slow decline we have seen in recent years.

Of course, the market won’t start valuing this as a growth company after one good quarter. Because they might it could have been a fluke. A one-off strong quarter. We need multiple quarters of growth to start getting a higher valuation. So now we have to use the information we have to analyze whether this is a structural change or a fluke.

They have said in the past that as they transition to a more self-serve long-term contract business model it’s not going to show revenue growth right away. And as some clients transition from managed to self-serve it takes them some time to return to the same spending levels. This was one of the reasons given for the lack of revenue growth.

They have also taken a hit by winding down their Argentina business.

“Revenue generated in the Europe, LATAM and Other category for the quarter was $4,983, a decrease of $4,164, or 46%. The primary factor for the decrease in this geography was specifically related to the South American region, where revenue decreased to $989 from $6,626 for the same period of the prior year. This 85% decrease was mainly attributed to revenue generated in Argentina. With changes in the political climate within Argentina and foreign exchange instability, the Company decided in late 2023 to substantively reduce itsrisk exposure in this region. As a result, revenue from Argentina was minimal for the three months ended September 30, 2024. The Company believes that this will continue for the foreseeable future and as such, will maintain its cautious approach to this region until conditions improve.”

Quote from Q3 MD&A

The revenue decline from this seems to be mostly over as the revenue from Argentina is already “minimal”. It’s also promising to see they were able to grow despite this factor decreasing revenue.

Also, the managed posted a small 3% y-o-y growth, and another reason for no revenue growth was that managed was declining while self-serve was rapidly growing. Self-serve still grew 64% y-o-y while management did not decline. If this is the new trend we should be getting consistent growth from now on.

The new CEO thinks managed service can return to growth. All of the below quotes are from the 3rd quarter conference call from the CEO or the CFO.

“These results also prove a point I made on prior calls where I discussed my view on managed services as an area where we could return to growth, moving our story from a single growth track to potentially multiple tracks of growth.”

“We will also continue to identify new opportunities for growth in our managed services business. By doing this, I am confident that we will increase revenues and ensure illumin's long term growth.”

Quotes from third-quarter earnings call 2 above from the CEO one below from the CFO

“3% rise in managed service revenue from the same period last year. This growth was mainly driven by new clients as well as higher platform utilization by existing clients.”

In the fast growth 64% y-o-y self-serve business they onboarded 29 new clients and are saying this is still at its early stages and see customers as early adopters. It was 23% of Illumin’s revenue in Q3.

There was also a 39% increase in programmatic revenue y-o-y. Which was 27,8% of their Total revenue. This is basically the non-Illumin revenue.

“All revenue earned outside of Managed service and Self-service illumin is reported as Programmatic revenue, which includes, among other things, our exchange services business, that captures our transactions generated from buying and selling of ad inventory through other bidding systems.”

Quote from Q3 financials

Source: https://ceo.ca/content/sedar/ILLM-2024-11-08-interim-financial-statementsreport-english-0fa4.pdf

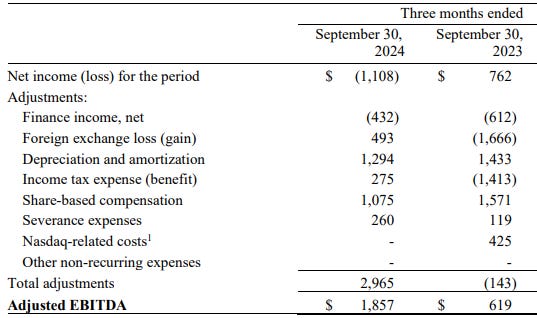

We are seeing a bit higher operating costs, but gross profit went up more than operating costs so operating loss went down significantly. If the company is growing the market can forgive losses especially if you have a strong balance sheet, because you can always make the argument that the company could be profitable, but they are investing in more growth and spending more on marketing to grow more.

And Illumin is not losing cash from operations considering non-cash expenses like Depreciation and stock-based comp.

Source: https://ceo.ca/content/sedar/ILLM-2024-11-08-interim-mda-english-ae56.pdf

ADJUST IT MORE

One thing people might be thinking about is whether the election gave them a one-time boost in earnings to make this quarter a one-off event.

"Inflexio" said on ceo.ca “IR confirmed to me that Political revenue would not have a material impact on their results for Q3 nor Q4” I suspect this is the same person as “Inflexio research” who wrote a good thread on Twitter about Illumin The thread

Also, they did not have a blowout quarter at the time of the last election (-3% revenue decline). Granted it was the Pandemic where their overall revenue dropped around 10%, but still.

What are the reasons given for this revenue growth?

They have been changing the team. New revenue officer. New SVP of marketing. They have been changing the way they are doing sales and experimenting with new strategies. Some segments like CTV(Ads for streaming on online connected TVs) have been growing a lot and also their integration with Meta(Facebook)seems to be helping. Then there are a lot of these generic terms that every company says like “customer-centric approach” and “addressing operational efficiencies”.

They are also predicting a “solid” revenue quarter for the next quarter.

“Looking ahead, we expect solid fourth-quarter revenue growth resulting in part from the recent organizational changes we have made in the leadership and sales team. For the long term, we remain focused on generating overall strong sustainable revenue growth and a prudent approach to cost management.”

So we seem to be in a pretty good position here as these are scenarios where the stock reaches a higher valuation.

Becoming a growth company=stock goes up

Becoming meaningfully profitable=stock goes up

Growing and meaningfully profitable=stock rockets up

The investment thesis is that Illumin will reach one or both of these scenarios while protecting the downside with the large cash pile and low valuation.

Now we are seeing signs of revenue growth and improving profitability.

One thing I would have liked to hear more about is the plan for capital allocation. They are sitting on a lot of cash that I would like to see deployed somehow in a value-creating way. What they said was pretty basic.

“All options, including synergistic acquisition opportunities and share repurchases, will only be undertaken under a structure of continued overall revenue growth and strong consistent cash flow from operations.”

So far this year we have had some buybacks, but I would like to see the buybacks ramped up way more when the stock is still cheap.

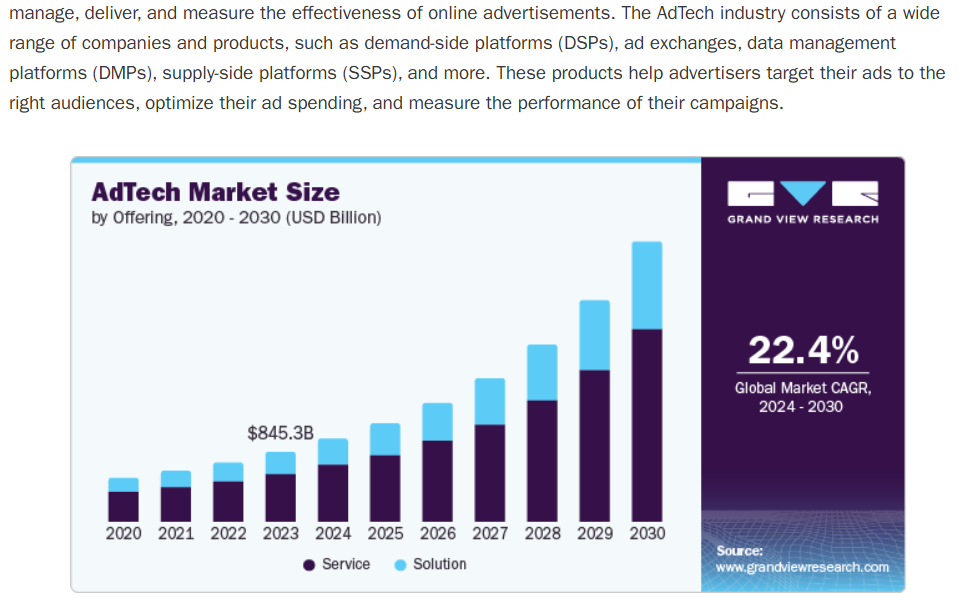

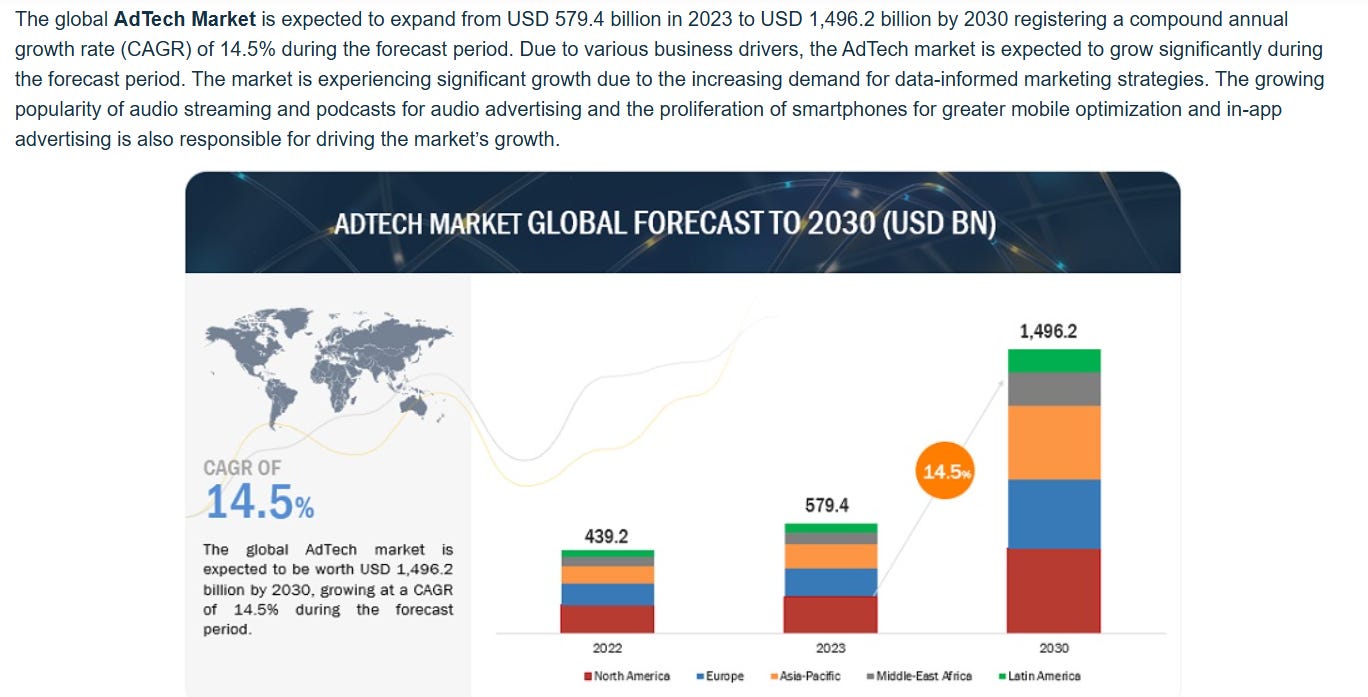

Adtech Market projections:

Source: https://www.grandviewresearch.com/industry-analysis/adtech-market-report

Source: https://www.marketsandmarkets.com/Market-Reports/adtech-market-135513139.html

Looking at the different projections about the Ad tech market over the coming years it shows that this is a fertile ground for a high-growth business with a high market valuation. not saying Illumin will become like the Trade Desk with years of growing fast and with a 26 P/S ratio, but Let’s say Illumin can grow to an annual rate of 23% consistently like in Q3. Business like that in this space. Probably get’s 2 P/S ratio.

Let’s take TTM revenue and add 23% → 127.5*1,23=156,8m this 2 times sales would be 313,65m market cap which would be a +230% gain from the current stock price.

Illustrating how little needs to happen for this stock to get some legs if the sentiment around it changes and it’s seen as a growth business.

Metro Mining

Source: Google

The stock price has gone a bit lower(-8%) since I released my write-up, but there was a very nice dip in between that this time(the stock dipped to 0,034) I used to lower my cost basis to 0,0408 so I’m up +23% on the stock. Because of this adding and the subsequent rebounding of the stock price Metro has become one of my biggest positions third biggest in The AlmostMongolian Portfolio.

From a fundamental standpoint, let’s see what has happened since my write-up in July.

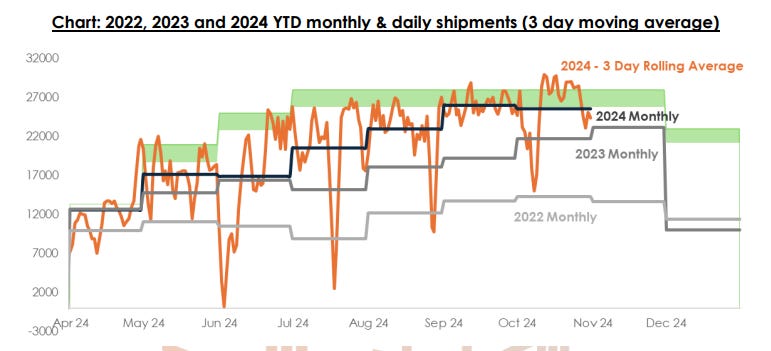

Metro has successfully ramped up production

Source: https://wcsecure.weblink.com.au/pdf/MMI/02876643.pdf

As you can see from the picture they were a bit late on the ramp-up. I think this caused some worry and caused the dip we saw in the stock. But now they are on track with their production ramp and based on their statements it looks quite good.

Source: https://wcsecure.weblink.com.au/pdf/MMI/02876643.pdf

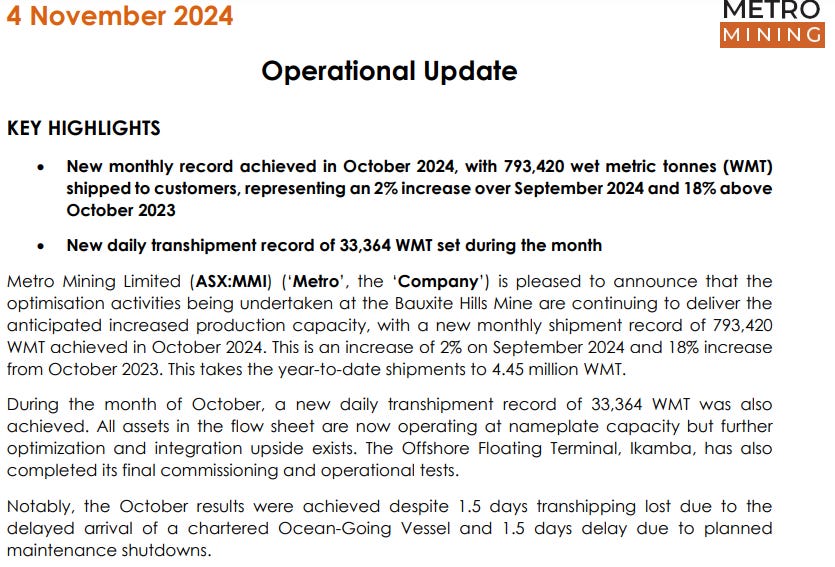

A new monthly record and a new daily record were achieved during October even with some delays and according to this “further optimization and integration upside exists”.

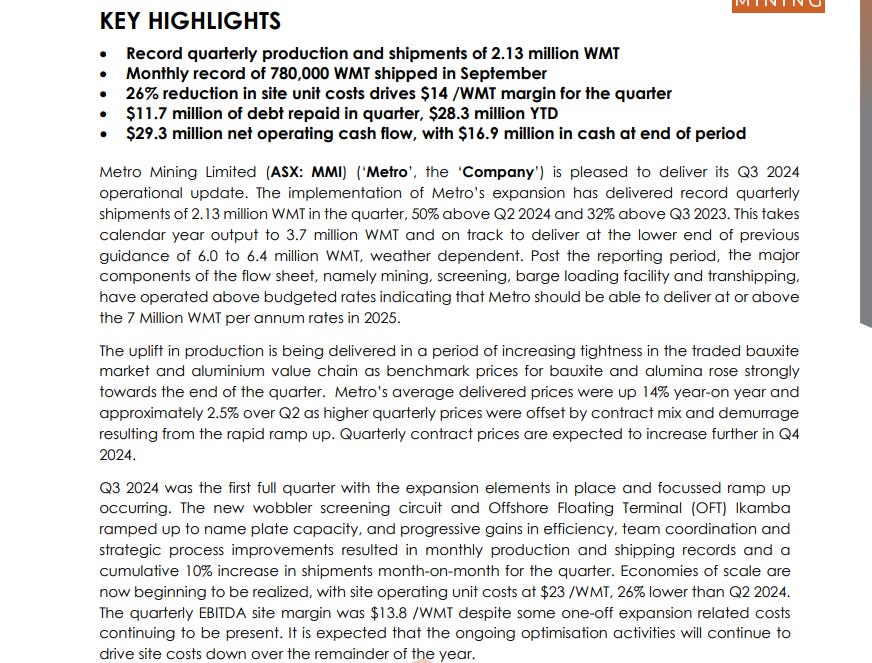

We also got the third quarter results. 3rd Q results do not reflect these new production numbers as Metro had not reached these production levels yet in July-August.

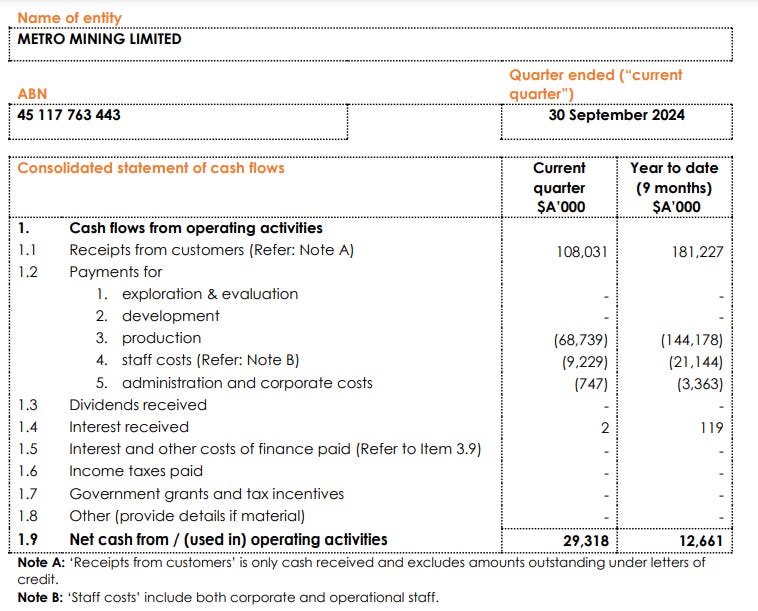

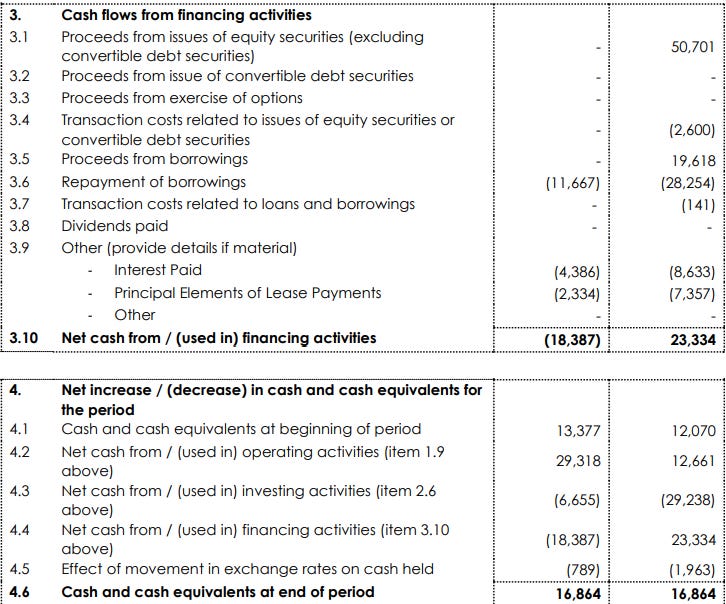

But even with the production lower than it is now Metro posted strong cash flow.

Source: https://wcsecure.weblink.com.au/pdf/MMI/02873852.pdf

We are starting to see the economies of scale benefits from the production ramp. Paying back debt from cash flow. The new production level de-risked.

Source: https://wcsecure.weblink.com.au/pdf/MMI/02873852.pdf

Huge improvement in cash generation without the full production ramp included in the numbers or the bauxite price increases.

Source: https://wcsecure.weblink.com.au/pdf/MMI/02873852.pdf

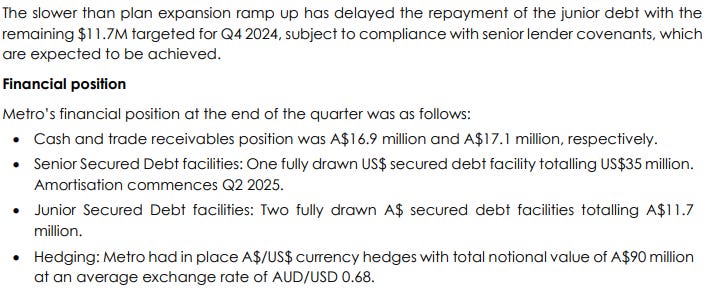

More repayments for Q4 and I expect Metro to be debt-free next year easily and hopefully start doing some form of shareholder returns.

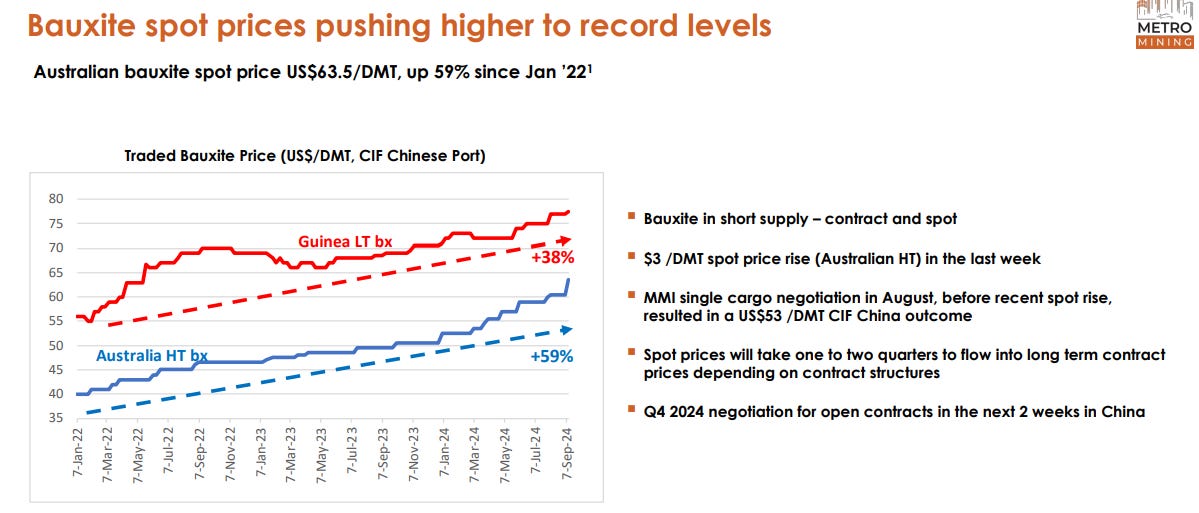

This was also in the PR “Quarterly contract prices are expected to increase further in Q4” This is big as bauxite prices have continued to increase.

Source: https://wcsecure.weblink.com.au/pdf/MMI/02851861.pdf

Source: https://www.metal.com/Aluminum/201303070020

This is the most recent price. 70 USD. And if it takes one to two quarters for a spot to flow into long-term contracts we should be seeing the amazing first half of next year.

One of the reasons for this price rise is that Guinea imposed a partial export ban on Bauxite. Here is an interview with Metros’ CEO talking about it.

Then there are longer-term factors playing into the supply/demand thesis

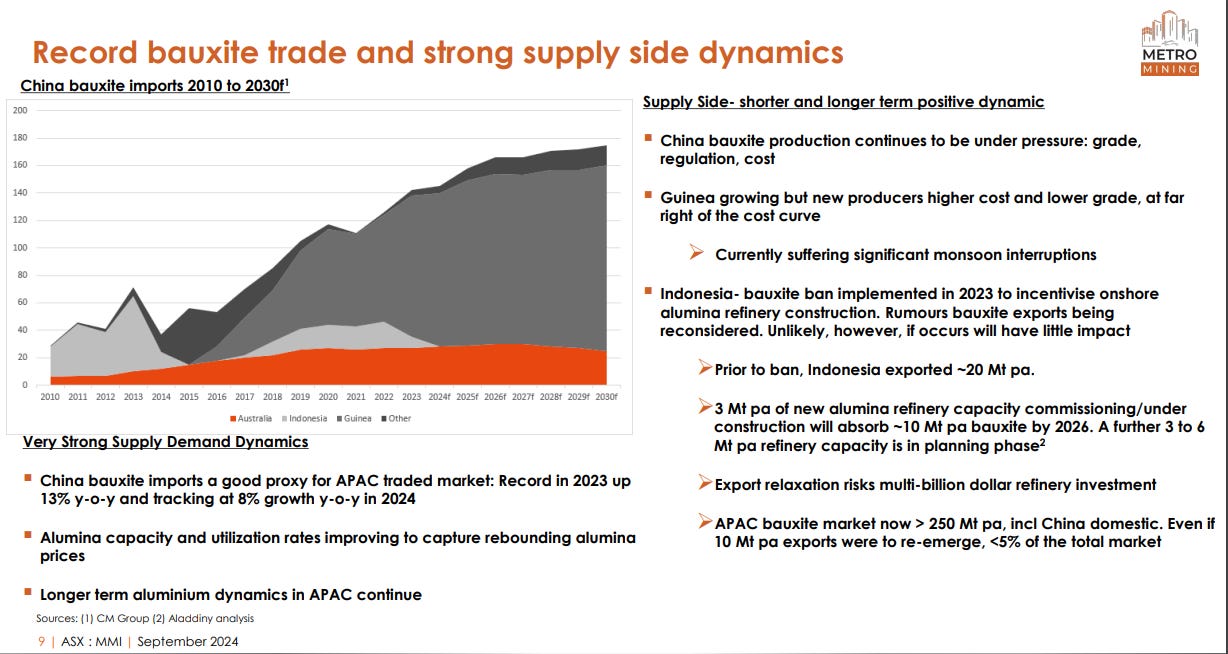

Source: https://wcsecure.weblink.com.au/pdf/MMI/02851861.pdf

The Chinese bauxite production struggling with strong demand is the long-term bull case unless Guinea just fills that gap as we are seeing they are already making export bans possibly trying to copy Indonesia’s strategy if developing their own refining. Currently, the situation in Guinea is uncertain for outsiders and the ban is not for all of their exports.

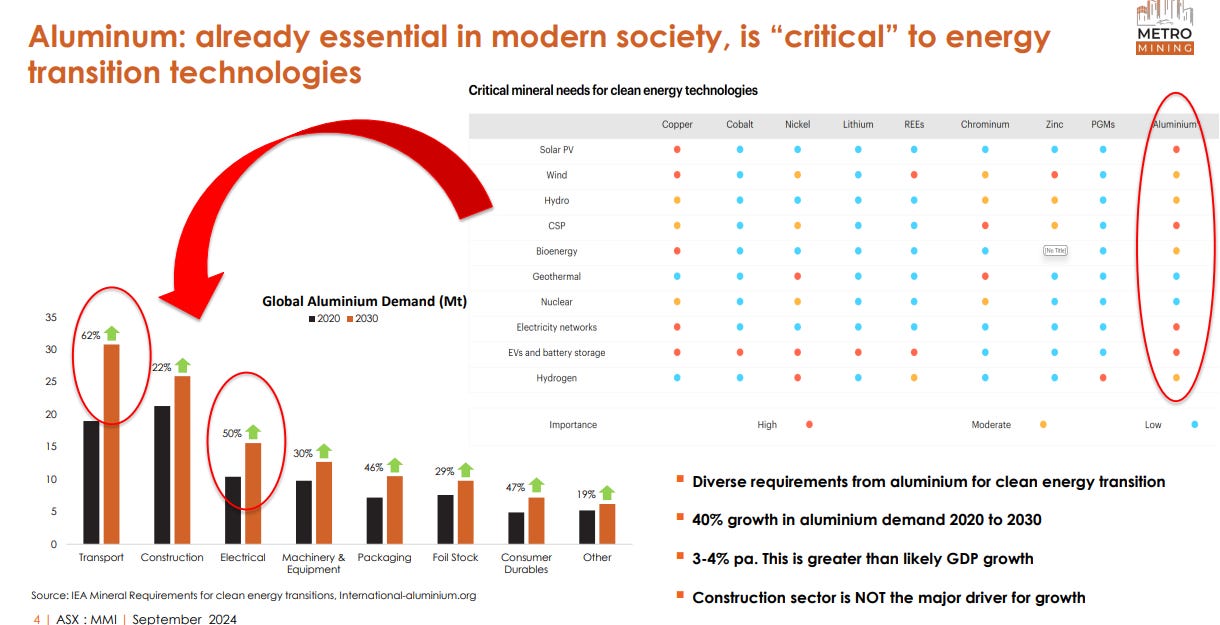

I suggest taking a look at this presentation Metro put out a link I’ll throw another slide about demand from that presentation in here.

Source: https://wcsecure.weblink.com.au/pdf/MMI/02851861.pdf

Aluminum demand is looking strong for the next decades.

Metro also announced new Offtake contracts Here

In summary, everything is going as expected the production is rising, the numbers are improving and the bauxite price is rising. The numbers will get better as the new production levels and bauxite prices start being reflected in the results in Q4, Q1, and Q2.

Now it’s just about waiting for those things. Waiting for the market to realize that the stock is cheap. Waiting for the company to start returning capital.

Just look at the valuation it’s priced like a mine in Africa even though it’s in Australia 297m AUD market cap

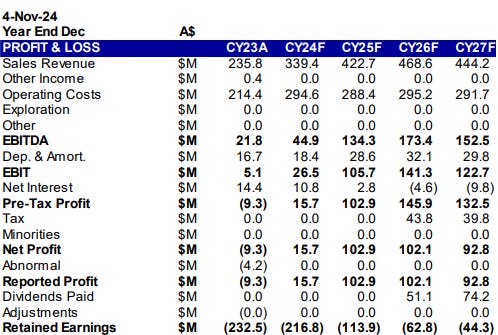

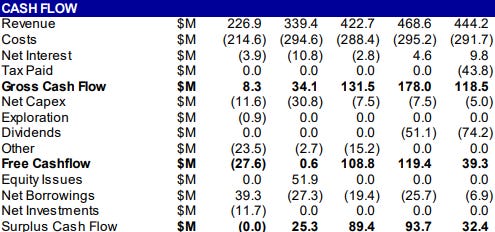

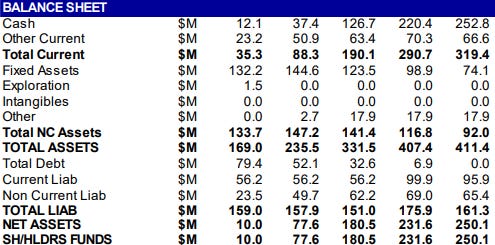

This is from the Petra Capital Research Report. They use 55 USD/DMT for this estimate for 2025(Current spot 70$). The reason for no taxes is the carry-forward tax losses they have.

Source: https://metromining.com.au/wp-content/uploads/2024/11/Metro_Mining_Limited_MMI_Another_monthly_shipping_record.pdf

The Capex is going down a lot next year. It’s just cash flow. These guys are estimating Metro would start paying dividends in 2026, but I think or I hope they will do it sooner because they could be paying a high dividend yield next year or buybacks. I repeat this estimate is using 55 USD/DMT bauxite price. You can check the report and run the numbers for whatever price you think is reasonable. The numbers get pretty wild at the higher prices.

Even with 55/DMT, we are making 108m of free cash flow next year based on these estimates. And should probably trade at a 500m market cap. But We are likely above 150m FCF for next year so what is the reasonable valuation for a single asset producer that will be debt-free in a first-world jurisdiction? 600m? 900m? Against the current market cap of 297m.

That’s it for the update as you can see all of these stocks are doing quite well from a fundamental standpoint. The risk/reward remains very favorable.

For Metro, In case you are trying to calculate sale price of the bauxite. From what I understand they have high temp bauxite which trades at a discount to the West Australia prices. So you can expect the price to be a bit below what is quoted. I dont think they come out and say what that discount is....just that there is one. I think its about 5-10$ cheaper tho.