Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian AD: THE LINK

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

Timestamps:

0:00 Opening remarks, Prologue, Preamble, Keynote address

6:20 Zoomd: Re-evaluation. What went wrong? BTD?

35:57 Comparison with Illumin’s situation(paywall starts)

42:55 Western Gold Resources: Last gold stock standing

57:35 Case for Western Gold becoming Beacon Minerals

1:11:00 Explaining why I’m not interested in Cerrado Gold anymore, or Cerrado-likes

1:25:30 Heartbeam: Bought the dip. Best set-up for Heartbeam so far.

Video Materials(notes, links, visuals used in the video):

Zoomd

The main risks I outlined for the thesis in April materialised, which were:

Q4 shows that the impact of the 2 large clients was larger than in Q3

Return to previous spending levels is slow, or previous levels are not returned to

Q3 showed only a fraction of the impact. And it was obvious and knowable.

It now seems the return to previous revenue levels from these customers is much more uncertain and slower than Amit led investors to believe in the February interview and the Q3 call.

Q3 communication:

“2 of our largest customers are making adaptation to the acquisition models and goals. We are working closely with them on adapting their KPIs and measurement models to align with their new objects. Such transitions are a part of our business and based on our experience, activity typically scales up within a few months. While these changes may temporarily impact near-term activity, they also established a foundation for stronger and long-term collaboration.”

This was vague “adaptations” etc. Hence, I wasn’t convinced to buy before the February interview with a different story.

In that interview, Amit said it was really about a technical change, and let investors understand that it’s all about changing the MMP, which is done, and they are already back to business, and the revenue will gradually come back.

“you know have they completed this technical change? did they technical change went through Q4? Yeah. They changed an MMP.”

“It will have an effect in Q4[understatement of the year], but then it gradually comes back as those clients are kicking running.”

“growth will be will will come and it will be gradual. Yeah. So it’s already fixed and we are back to business.”

“Q3 that in Q4 we got a bump in the wing from two clients of ours and I can say here proudly that this is part of the business the company didn’t lose those clients in fact they remain the biggest clients that we have some of the biggest client that we have and it gradually will come back. So the short-term expectation is that the company is riding like crazy still generating cash and showing good numbers and and I feel that it’s stable.”

But in Q4 results. The reality seems to be more like they communicated in Q3, but worse, as activity hasn’t scaled within a few months, as they said in Q3.

“Revenues in Q4.25 were $7.5M, a 50% decrease from $15.1M in Q4.24, reflecting the

continued impact of operating model changes implemented by two major customers, as discussed in the Company’s Q3.25 report, including ongoing adjustments to customer acquisition strategies and KPIs. Activity levels continue to be affected by these changes, with visibility remaining limited for one customer, while the other is showing initial signs of realignment following meaningful progress.”With one of these customers, visibility remains limited regarding the timing and extent of a potential recovery. With the other, we are beginning to see signs of improvement.

The February interview was all about the MMP(mobile management platform) change. And the recent earnings call and PR don’t even mention MMP.

Q1:

85% of our revenues come from five largest customers.

Q2 call:

As we reported, 83% of our revenues come from our top five customers. Revenues from these top five customers grew both compared to the same quarter last year and to the previous quarter.

Q3

“over 70% of our revenues come from the top 5 customers” call

“as five of the Company’s customers comprise 77% of its revenues for the nine months period ended September 30, 2025” MD&A

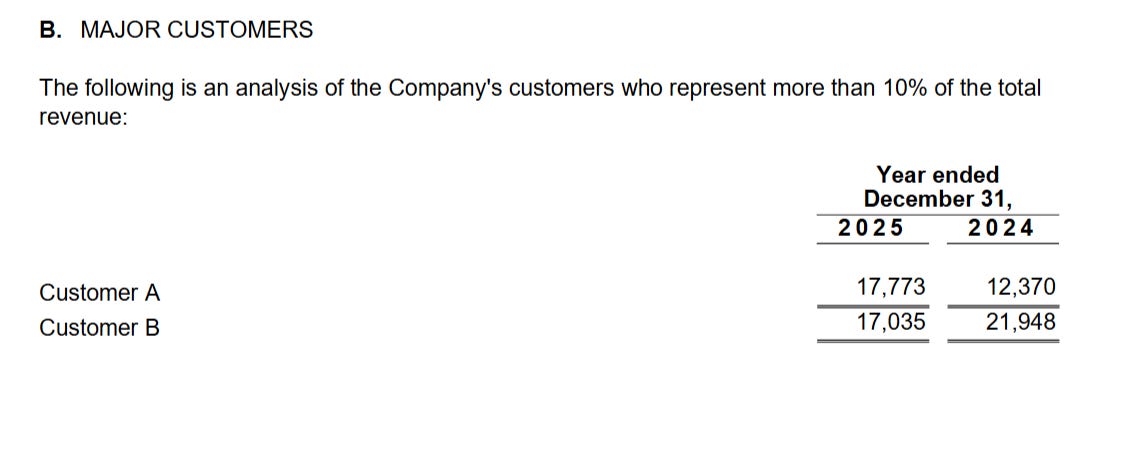

Comparing Q2 2025 with the full impact of the 2 clients to Q4 2025, when the clients were at 0. Revenue dropped 61.73% from 2 clients

Clearly, these 2 clients are way bigger than the rest of the top 5, so talking about revenue from the top 5 is a way of misrepresenting the client concentration risk to investors.

Q4 call:

In 2025, revenues from customers outside of top two grew over 30% year-over-year.

Now it’s the top 2 when they can’t hide it. No mention of top 5 or top 10 anymore in the Q4 call.

Excluding the two largest customers, the rest of the customers base grew by around 30% in the quarter. In addition, roughly one-third of our annual growth came from newer customers that were onboarded in recent periods.[That would be $2,25 million]

Amit Bohensky, Founder and Chairman, Zoomd: The fourth quarter, we were impacted by reduced activity from our two largest customers. It’s important to clarify that these customers have not left. We continue to work with them, and the relationships remain strong. With one of them, as mentioned earlier, we are already seeing early signs of stabilization and gradual improvement in activity levels, which is encouraging. Our experience shows that because of the bandwidth of our offering and our ability to adjust to different models, customers continue working with us and even their strategies change, and we are well positioned to support them as actively evolves. It happens in any company that occasional singular events can have a meaningful impact on revenue in a given period. These are by nature infrequent.

We take each instance seriously, learn from it, and continue to improve by the business. When you look at underlying performance excluding these events, the broader momentum of the company remains intact. We believe our investors recognize this dynamic and maintain a long-term perspective.

“long-term perspective” red flag

https://zoomd.com/wp-content/uploads/2026/04/Zoomd-Investors-Deck-Q4.2025-1.pdf

How could I have avoided this outcome with better DD?

I didn’t even look at this, which would have given me a better idea of Q4 impact:

Source: https://ceo.ca/content/sedar/ZOMD-2025-03-25-audited-annual-financial-statements-english-c300.pdf

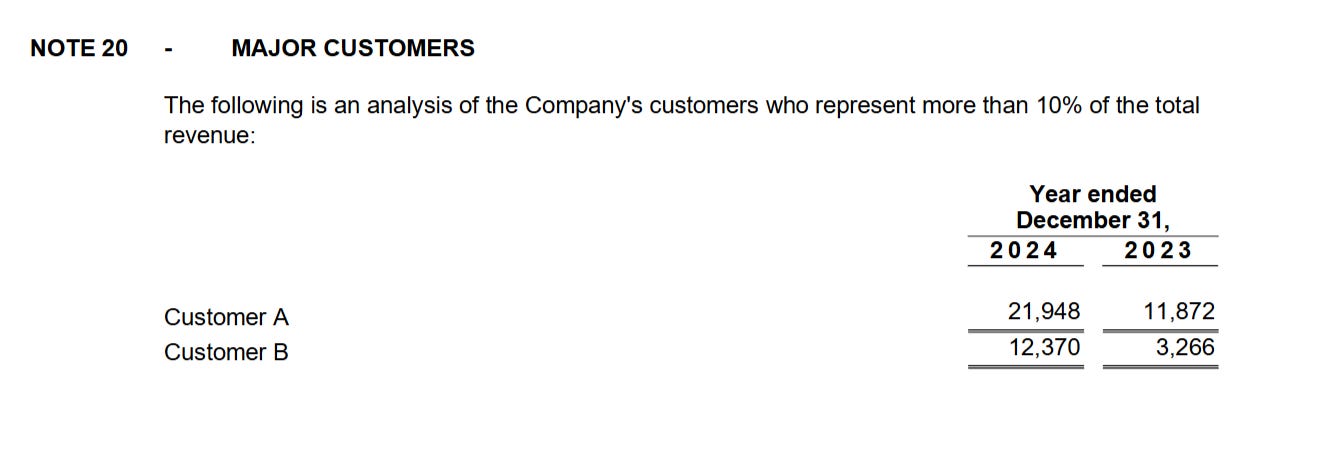

These 2 clients were 62,9% of the revenue in 2024.

A big reason for the mistake: “If that’s the case, I would have seen it talked about, heard about it, etc”

Source: https://ceo.ca/content/sedar/ZOMD-2026-04-28-audited-annual-financial-statements-english-187e.pdf

I could have researched the history of Amit’s communication, especially during the period from 2022 to 2023, when the stock collapsed 90% from peak to trough.

After looking at some of the transcripts. It didn’t seem that bad.

New base case

Market cap now at 55 cents: US$41.5 million

EV=US$ 19.5 million

$7.5 million base revenue per quarter

$12.1 million quarterly revenue lost from 2 clients.

If we assume a 50/50 split, that’s $6.05 million per one.

If they get one back to Q2 2025 levels, the company gets back to $13.55 million per Q.

$2.5-3.5 million net income using a range of GM and operating costs.

That should get the stock back to the $0.80-1.10 range.

If this trend holds up, “Excluding the two largest customers, the rest of the customer base grew by around 30% in the quarter.”

Base revenue 1.3*7.5=$9,75 million base revenue in Q4 2026

20 new clients ramping up in 2026, if let’s say $100k per quarter per new client=$2 million per Q = $11.75

If we add everything up, 9,75+2+6,05=$17.8 million rev Q4 2026

This should get the stock back to $2

In 2026, M&A is a key part of our strategy and is taken into account in our capital allocation planning. Regarding to the NCIB, we are considering commencing a normal course issuer bid NCIB program with a target timeline following the release of our first quarter of 2026 financial results. For obvious reasons, I’m not in a position to comment on the specific amount that may be allocated to the NCIB at this stage, and we will provide an update to the market once details are finalized.

Below are the materials for the paywalled part of the video.