Disclaimer: I’m not an investment advisor. Nothing I have written in this article should be taken as investment advice. Everything I have written here could be inaccurate. Trust nothing you just read. I’m part of the Seeking Alpha Affiliate program, which means I have a financial relationship with Seeking Alpha. This article is for entertainment purposes.

Mongolian AD: THE LINK

Get a 7-day free trial and 30$ discount on your first year of Seeking Alpha Premium with my Affiliate link: AFFILIATE LINK

Video Materials:

Market cap = US$60.9 million

EV = US$42.61 million (based on Q3 cash)

TTM net income = US$17.7 million

P/E= 3.44

EV/E= 2.41

https://zoomd.com/wp-content/uploads/2026/01/Zoomd-Investors-Deck-Q3.2025.pdf

Why did I sell in November?

Bad Q3 compared to shareholder expectations, material revenue decline QOQ, and small decline YOY, still high net income, and decent valuation

2 clients are going through a transition

Halted momentum on the stock. Presented an opportunity cost

Why did I buy it back?

We now have more clarity on the reasons behind the Q3 decline and the path back to growth.

Valuation got cheaper

Time passed

High probability path back to momentum in 2026 and for the stock to 2-3x before YE, with limited downside in case it doesn’t work out

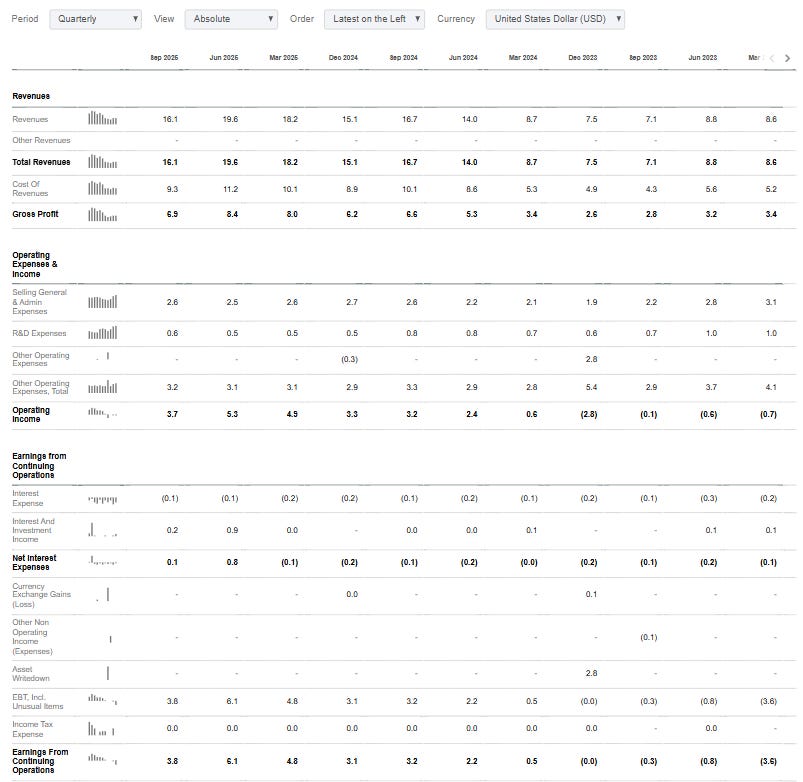

Source: https://seekingalpha.com/symbol/ZOMD:CA/income-statement

“In Q3 2025, the company reported a 3% decrease in revenues compared to Q3 2024, primarily due to the fact that most revenue from the Euro Cup tournament was recognized in Q3 of 2024.”

Next question comes from Paulo. It says, “Last earnings, we felt that large clients may be pulling back for next quarter. Is this true or are we reading it wrong?” I think you touched on that a little bit maybe. So it says last earnings we felt that large clients might be pulling back for the next quarter. Is this true or are we reading it wrong? We announced in Q3 earnings that two clients of ours ask us to halt marketing for them due to technological problem within their system. Nothing to do with Zoomed. They still are our clients, loyal clients. They love us. They even sent our testimonial and references to us. But they had an issue. We needed to halt marketing. I can expand on that if if if you want. It’s a bit technical, but I can explain what happened. Every app has a piece of software in it that is called an MMP. Mobile management platform. Any app that respects itself. So if you have a Google app, a Facebook app, it will have an MMP. that tool inside the app. The the manufacturer of the app puts it inside it in order to do different measurement. Two clients announced that they are taking out their MMP. Nothing to do with us. It’s like changing the cloud. So they change their cloud infrastructure. They change their MMP infrastructure. The moment they do that, there is no way for us to calculate how much customers are driven to them via zoomed because we use the MMP as a tool as a calculator to empirically understand how much they need to pay us in the end of the month. That’s why they are said we listen we are doing an infrastructure change we are changing an MMP. This thing never happened by the way. It happened to me in an entire career of zoomed only twice. It’s very rare but two clients did that by the way. one of the viewers of of your forum wrote me directly and said how strange that it happened to two clients in the same times it is but 10 other clients that are using the same MMP didn’t do that and I must say that two of those clients do not know each other and they are there from two sides of the world so [clears throat] it’s nothing to do about their knowing us it’s nothing to do about that one knowing the other piece of software that they decided to change the moment they change it we we hing for them. It will have an effect in Q4, but then it gradually comes back as those clients are kicking running.

So a question on so your your two largest clients that have you know sort of halted work based on this technical change. any any any chance you’re going to give an update on how that’s going? you know have they completed this technical change? did they technical change went through Q4? Yeah. They changed an MMP. It’s like taking a piece of software out. they put a new piece of software and then you do pilots because you do customer acquisition and you want to make sure that this MMP thing calculates in the right way your cut what you get and that is why the growth will be will will come and it will be gradual. Yeah. So it’s already fixed and we are back to business. Gotcha. And do you have a sense when you know that it’s full speed again? Like is it is it months is it weeks is it when we can’t disclose that we can’t can’t disclose that and this is very important to tell to the shareholders. When I say we can’t disclose, it’s not that we don’t want we are under a very severe NDA with those client.

Q3 that in Q4 we got a bump in the wing from two clients of ours and I can say here proudly that this is part of the business the company didn’t lose those clients in fact they remain the biggest clients that we have some of the biggest client that we have and it gradually will come back. So the short-term expectation is that the company is riding like crazy still generating cash and showing good numbers and and I feel that it’s stable.

source: SmallCap Discoveries Interview 17.2

2 clients halted marketing for a period because they changed their mobile management platforms. They remain clients

Already fixed in q4 and back to business with those clients. Can’t disclose when they get back to “full speed”

This is rare. Never happened to them before. Coincidence that 2 clients did it at the same time. Other clients that were using the same MMP didn’t change

This caused a hit in Q3 and Q4. Based on what he says, we don’t know whether Q3 or Q4 took a bigger hit from this. Although better seasonality in Q4 should soften the impact

“Stable” word choice matters. Interview before Q3, similar language(not the same), but hesitant to talk about revenue growth. I wouldn’t expect significant revenue growth in the short term

I want to update that in line with the recent changes in the marketing space, 2 of our largest customers are making adaptation to the acquisition models and goals. We are working closely with them on adapting their KPIs and measurement models to align with their new objects. Such transitions are a part of our business and based on our experience, activity typically scales up within a few months. While these changes may temporarily impact near-term activity, they also established a foundation for stronger and long-term collaboration.

As we reported, over 70% of our revenues come from top 5 customers.

Our performance continues to deliver operational ROI for our customers, supporting strong client retention and driving new customer wins. Revenues from clients outside of the company’s top 10 customers doubled in Q3 ‘25 compared with Q3 ‘24, a showcase of the significant efforts undertaken to aviate our customer concentration. Over the past year, we added more than 10 new clients and based on the typical revenue ramp-up time. We expect to see the impact of these wins in 2026. With 2026 in also being a World Cup year, we started to strategize with some of our customers to secure budgets for the World Cup, which is the most viewed sporting event in the world.

E2 is now offering Zoomd’s user acquisition services, which provide us exposure to dozens of sportsbook operators and broader sports and betting clients worldwide. Initial integrations are underway and broader campaigns will roll out in the coming months. We expect meaningful contribution already in 2026, which is also a World Cup year, a factor that should further boost demand in this segment.

Source: Q3 earnings call

Better positioned in sports now due to the E2 partnership(announced last October). Q1 2026 had the Winter Olympics and the Super Bowl. Q2-Q3 2026 has the FIFA World Cup(11.6-19.7), predicted to drive $10.5 billion in ad spending. source Most revenue to be recognised in Q3

10 new clients added last year, expected to see the impact in 2026

Bear Case:

Q4 shows that the impact of the 2 large clients was larger than in Q3

Return to previous spending levels is slow, or previous levels are not returned to

General client concentration risk from “over 70% of our revenues come from the top 5 customers”

Iran war risks:

Their revenue from the region is insignificant. Not the risk.

Hormuz stays closed, which causes a global recession, which causes marketing spending to go down, etc. Biggest risk, but in this scenario, most other stocks would fall as well, and Zoomd has a better margin of safety than most stocks.

Zoomd is headquartered in Tel-Aviv. What if they get hit by a missile? Very low probability - if it happens - cloud-based, 6 offices across the globe, remote work

In a bear case, some combination of these risks materialises and may result in revenue drops to, for example:

Revs US$12 million per quarter

43% GM =US$5,16 mil GP

operating expenses US$3.1 million

operating income US$2,06 million

An unknown amount of Tax loss carry forwards, no tax in recent quarters

Adding 300k interest income pa

Annualised net income US$8,54 million

Still P/E of 7.1 and EV/E of = 5 (based on Q3 cash)

But the stock would likely go down 40-60% percent from the current price

Bull case

back to Q2 25 growth trajectory in Q3 26 and onwards, Annualised net income US$25-30 million, market cap to US$250-300 million, stock price 4-5x

2025 peak US$190 million market cap